- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 01.31.2026

Location Strategy Chartbook 01.31.2026

Real Estate Market Insights

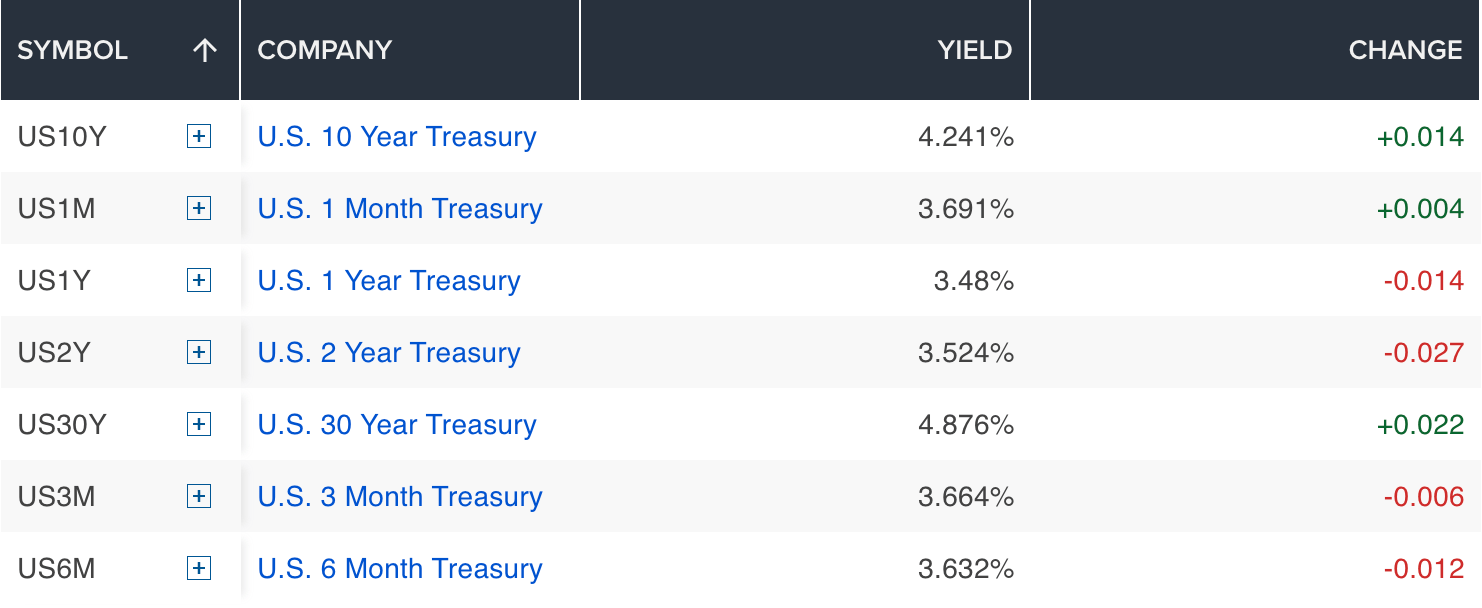

U.S. Treasury yields head steady on Friday after the latest producer price index came in more than double Wall Street estimates and after President Trump named Kevin Warsh as his pick as the next Federal Reserve chair.

The 10-year Treasury yield rose around 2 basis points to 4.251%, while the 2-year Treasury note yield slipped about 2 basis points to 3.531%. The 30-year Treasury yield added around 3 basis points to 4.887%.

CNBC

Warsh, 55, earned a law degree from Harvard University in 1995 before becoming a banker at Morgan Stanley, where he later served as vice president and executive director before joining the Bush administration in 2002 as executive secretary at the National Economic Council.

Bush nominated Warsh to serve on the Federal Reserve’s Board of Governors in 2006, with Warsh becoming the youngest person ever to join the central bank at 35.

During the 2008 financial crisis, Warsh aided in the government’s bailout of insurer AIG and assisted in JPMorgan’s acquisition of Bear Stearns, an 85-year-old brokerage that collapsed as the investment banking industry failed.

Warsh criticized the Fed’s decision to quickly lower interest rates during the financial crisis, arguing the cuts would only spur inflation, and was the only Fed official to argue against the central bank’s plan in 2011 to buy $600 billion in Treasury securities.

He joined the right-leaning Hoover Institution think tank after resigning from the Fed in 2011, and Warsh was among the finalists before Trump nominated Jerome Powell to succeed Janet Yellen as Fed chair in 2017.

Warsh is a critic of Powell, telling CNBC last year he supported a “regime change” at the Fed, claiming its policy has been “broken for quite a long time” and arguing Trump was “right to be frustrated” with Powell’s refusal to lower interest rates more quickly.

Consumers maintained robust spending in late 2025, according to new Bureau of Economic Analysis data released last week that had been delayed by the federal government shutdown.

However, shoppers increasingly dipped into savings accounts to get through the holiday season, reducing the personal savings rate to a three-year low. And with year-over-year real spending growth outpacing disposable income growth for the 17th consecutive month, this spending growth appears to be on an unsustainable path.

Still, economists expect consumer spending growth to continue in 2026. Those projections for positive, albeit slower, spending growth hinge on new tax policies delivering higher-than-average annual tax refunds in the first quarter. Combined with provisions of the One Big Beautiful Bill Act, these changes are expected to bring incomes and costs into better balance.

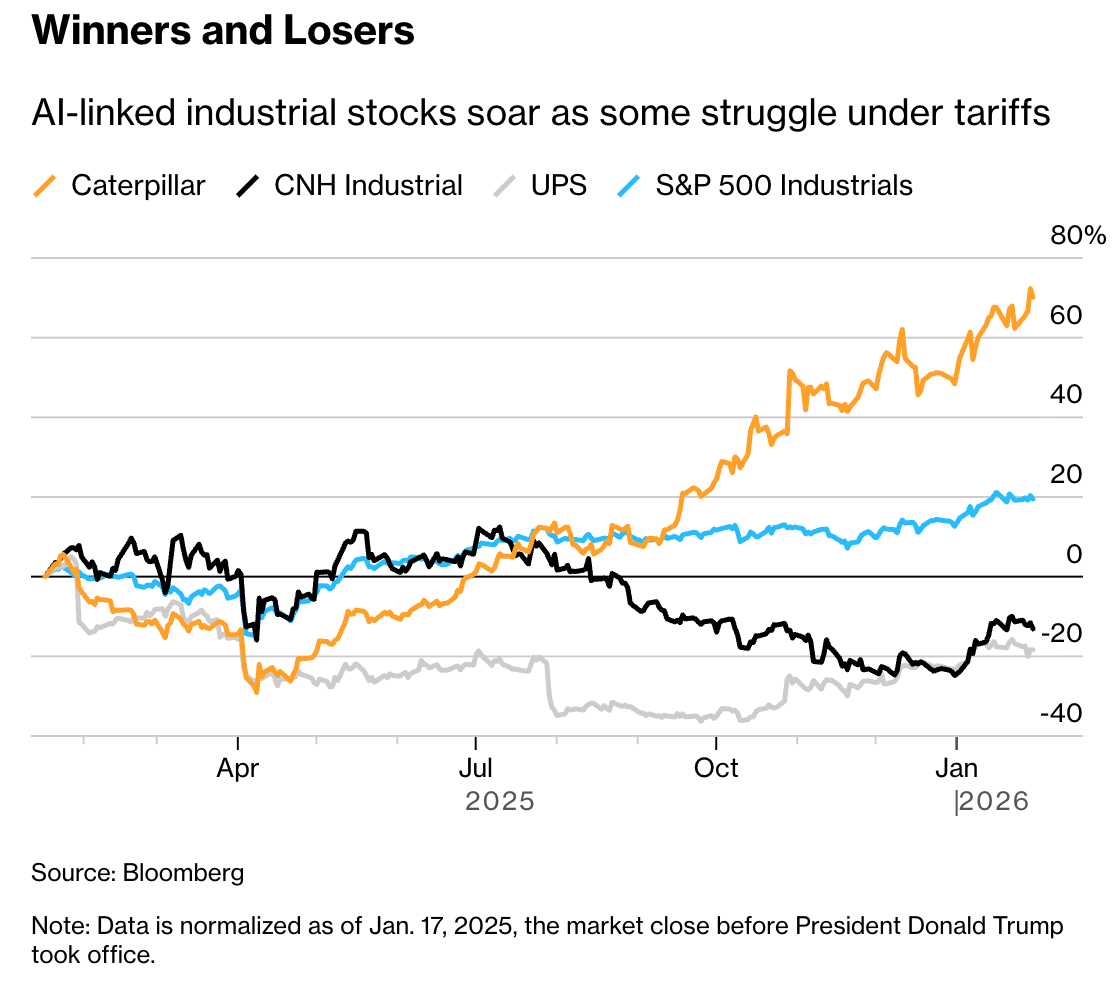

Earnings reports from some of the largest US manufacturers and transportation companies this week drove home how policies on trade and energy are putting a squeeze on the sector’s profits.

Caterpillar, which imports raw materials and parts for construction equipment, said it expects the levies to cost about $2.6 billion this year. Railroad Norfolk Southern said trade policy is eroding demand for some of its business lines, and shipping giant United Parcel Service said trade flows are shifting in a way that’s pressuring margins.

Meanwhile, on the energy front, power-equipment company GE Vernova Inc. took a hit last month after the Trump administration required work to stop on a wind farm off the coast of Massachusetts. Its wind business recorded a wider-than-forecast $225 million loss last quarter.

AI euphoria. Caterpillar and GE Vernova are seeing strong demand for their power-generation equipment, which drove up their stocks after this week’s reports. GE Vernova said it’s in frequent talks with the White House about ramping up production of its natural-gas turbines. Still, the unit’s “substantial headwinds” weighed on guidance for the year, Colin Rusch, an analyst at Oppenheimer, wrote in a note to clients. At the same time, he said demand in its power and electrification businesses is beating expectations.

High‑end consumers, still willing to pay for premium experiences, boosted demand at luxury hotels. Revenue per available room, or RevPAR, for the luxury hotel segment rose 3%. In contrast, consumers with less disposable income pulled back on both travel frequency and spending, leading to a 4.4% decline in RevPAR among economy class hotels.

Many economists describe the current U.S. economy as being 'K-shaped,' referring to the spending gap that appears to exist between the two ends of the consumer spectrum. Often, higher-income households have greater exposure to the stock market and own residential real estate, providing additional disposable income that they can spend on high-end experiences.

Lower-income households, however, need to allocate more of their income to necessities as inflation drives up prices. This, in turn, erodes travel budgets for lower-income consumers, putting pressure on more-affordable limited-service properties.

By contrast, luxury hotels have maintained pricing power. Room rates increased by an average of 3% in 2025, even as occupancy held steady at 2024 levels. This underscores the ongoing ability of luxury hotel owners and operators to command higher rates by delivering upscale experiences.

Office sales volume for 2025 was more than $56 billion, an increase of $10 billion from 2024, according to CoStar’s preliminary year-end figures. The year-over-year sales increase of more than 20% far exceeded that of the other major property sectors.

While values are still approximately 45% below the cyclical peak, the stabilization suggests that buyer interest in investment-grade multitenanted office assets is returning. While the risks have not disappeared, the prospect of capitalizing on lower property values has brought even some institutional buyers back off the sidelines.

Institutional buyers accounted for about 40% of transacted office value in the late 2010s, but their share began to fall sharply in early 2022. By 2024, they were involved in less than 20% of purchased office value. Occupiers and private buyers helped fill some of the gap, though many office building trades simply did not occur — as evidenced by depressed sales volumes in 2023 and 2024.

Last year, however, the institutional share of buying activity picked up again, ending the year above 25%. The return of these buyers was a major driver of the outsized increase in office sales activity, which accounted for its largest share of overall commercial property transaction volume since 2021.

At the end of 2025, a handful of Los Angeles commercial properties carrying playful names including Quick Quack and Crystal Cave sold at prices seriously above average. The real estate in question? A California mainstay: the car wash.

Across the nation, sales of car wash properties soared in the past year as operators cashed out of their owned real estate in sale-leaseback deals to fund their next wave of growth. Legislation adopted as part of the federal One Big Beautiful Bill last year boosts tax incentives for buyers of properties with qualifying equipment, such as car washes. That's expected to help send the sector to record transaction volume this year, property professionals say.

The bill "certainly won’t drive down pricing, but it significantly increases the buyer pool for the product type,” said Calvin Short, executive vice president and managing principal at SRS Real Estate.

Short said U.S. car wash deal activity surged to an estimated $350 million in the second half of 2025, with prices outpacing other property types on a per-square-foot basis, as investors rushed to lock in the tax benefit.

Falling oil prices could lead to reductions in rent as the Midland-Odessa area pushes through the slower winter months for apartment demand in early 2026.

As of late January, multifamily rents in Midland-Odessa were down a modest 0.1% year over year, while West Texas Intermediate was down roughly 14%. At roughly $58 per barrel, oil prices continue to decline from their peak of almost $273 per barrel in 2021.

The seasonal effects of the spring and summer months were particularly strong last year, helping Odessa resist falling into negative territory over the past 12 months. Nonetheless, slower rent growth is apparent in both markets as 2026 opens on shaky ground.

After strong leasing in the spring and summer, most apartment markets tend to see a slowdown in demand during the fall and winter months. In this way, Midland and Odessa are similar to their peers across the nation.

Inventory Boomerang hits housing market as last year’s 10-year high in delistings turns into a relistings jump. In the second half of 2025, there was a notable jump in delistings, as some home sellers—particularly in the Sun Belt—who couldn’t get their desired price decided to pull their homes off the market. Indeed, U.S. delistings as a share of inventory ticked up to 5.5% in fall 2025—a decade-high reading for that time of year.

In December 2025, ResiClub noted to readers that: “Looking ahead, in markets seeing the biggest jumps in delistings right now, many of those listings will likely return to the resale market in spring 2026—or test out the rental market.”

Fast-forward to January 2026, and we are indeed seeing an upswing in relistings*, according to Compass chief economist Mike Simonsen’s analysis of Altos Research data.