- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 02.28.2026

Location Strategy Chartbook 02.28.2026

Real Estate Market Insights

The S&P 500 is poised for a monthly loss after a whirlwind February defined by twin fears: that the AI trade has become a bubble, and that the technology itself could prove deeply disruptive. Treasuries, meanwhile, are wrapping up their best monthly performance in a year, a reminder that—for now at least—the $30 trillion market still reigns as a safety valve, regardless of all the doubts about US fiscal health. And if you thought bullion was the refuge of risk-averse retirees, think again. Gold above $5,000 an ounce is starting to look like the new normal.

U.S. Treasury yields fell Friday as investors reacted to a stronger-than-expected January wholesale inflation report, and a tumbling stock market amid rising fears of artificial intelligence hurting the economy.

The benchmark 10-year Treasury yield fell more than 5 basis points to 3.962%, while the 30-year Treasury bond yield dropped more than 3 basis points to 4.631%. The 2-year Treasury note yield was lower by more than 5 basis points at 3.389%.

WSJ: The K-shaped economy is creating new challenges for food companies.

The traditional strategy—once built around a broad, stable middle class—has effectively collapsed. Companies that previously sold to the masses now need to deploy two distinct playbooks: one for cash-strapped shoppers and another for higher-income consumers buoyed by rising stock markets.

In the wake of the pandemic, food giants hiked prices well beyond inflation. When consumers revolted against excessive costs and volumes dipped, companies like PepsiCo and General Mills pivoted to aggressive promotions to regain market share.

But there is a hidden barrier to entry for these savings. The better off often score deals through bulk sizes and loyalty perks. Meanwhile, many lower-income consumers—unable to afford the upfront cost of a deal—end up paying higher unit prices for smaller, budget packs.

Granted, price disparities have always existed. But the combination of stubborn food inflation and record income inequality is exacerbating the divide, forcing global food majors to rethink how they market to different economic strata.

Meanwhile, over the past three years, General Mills, Kraft Heinz and Conagra have seen their stock prices collapse. While a recent rotation out of Big Tech provided a modest lift to consumer-staples companies, valuations remain depressed. Kraft Heinz, for example, is trading just under 12 times forward earnings versus a 15-year average of nearly 16.

General Mills shows the risks. Last week it warned of “significant consumer stress, especially for the middle and lower income groups,” due to inflation and reductions to government benefits like food stamps. The company lowered its full-year outlook for sales and profits, sending shares down 7% that day.

For the cash-strapped, companies have to offer a low-enough out-of-pocket expense. This way the item stays in the weekly shopping basket, even if the price-per-unit is higher than what a higher-income shopper might get.

Bob Nolan, senior vice president at Conagra Brands (the maker of Slim Jims), explained at a recent consumer conference that lower-income consumers are “shopping basket to basket or even meal to meal” until their next paycheck.

Higher earners, conversely, have the “ability to invest” when promotions hit. They can buy 10 of an item on sale because they have both the liquid capital and the physical space—large pantries or even second freezers—to store it.

Andre Maciel, finance chief at Kraft Heinz, said at the same conference, it is about offering discounts that work both for struggling consumers as well as for those flush with cash.

The economy ended in a downshift in the last quarter of 2025, after two quarters of stronger-than-expected economic growth.

Gross domestic product (GDP) recorded a 1.4% annualized growth rate in the fourth quarter, far below expectations. For the year, the U.S. economy grew by 2.2%, slower than the relatively robust 2.8% in the previous year and 2.9% in 2023.

Consumer spending — generally the largest contributor to GDP growth — rose 2.4% in the fourth quarter, a slowdown from the 3.5% growth in the third quarter but still solid. Purchases of goods fell, likely due to the decline in vehicle sales following the expiration of the tax credit for electric vehicle purchases. Meanwhile, purchases of services rose a healthy 3.4%.

Overall, consumers contributed 1.6 percentage points to overall growth, more than offsetting the negative contribution of government spending, which fell due to the lengthy federal government shutdown in the quarter.

A 22-property hotel portfolio serving as collateral for $265 million in commercial mortgage-backed securities debt moved to special servicing in January.

The case stands out because it exposes the limits of the post-pandemic hotel recovery narrative. The portfolio, comprising full-service, select-service, extended-stay and limited-service hotels, has yet to return to pre-crisis performance — despite carrying three of the industry's most recognized brands.

The Starwood Capital Group-owned portfolio includes 2,943 keys across 17 cities and operates under the Marriott, Hilton and IHG flags. It transferred to a special servicer effective Jan. 28 after the loan was flagged for imminent default, according to commentary reviewed by Morningstar Credit. The borrower had paid the loan through Jan. 11.

Net operating income in 2024 sat 57% below 2019 levels and 31% below the income level Fitch Ratings used at loan issuance, according to the bond rating firm's rating action in July. The portfolio's debt service coverage ratio — a key measure of a property's ability to service its debt — stood at just 64 cents per $1 owed for the trailing 12 months ended June 30, according to Morningstar DBRS. Weighted average occupancy fell from 72.5% when the debt was issued to 63.1%, while revenue per available room dropped from $84.80 to $78.90.

The portfolio's last formal appraisal, conducted at issuance, valued the collateral at $401 million. Both Morningstar DBRS and Fitch flagged that figure as likely overstated given the cash flow erosion, but neither agency published an updated valuation.

The loan does not mature until September 2028, giving the special servicer and borrower a window to negotiate. But with interest rates remaining elevated and hotel cash flows under pressure, analysts see limited options for a clean exit.

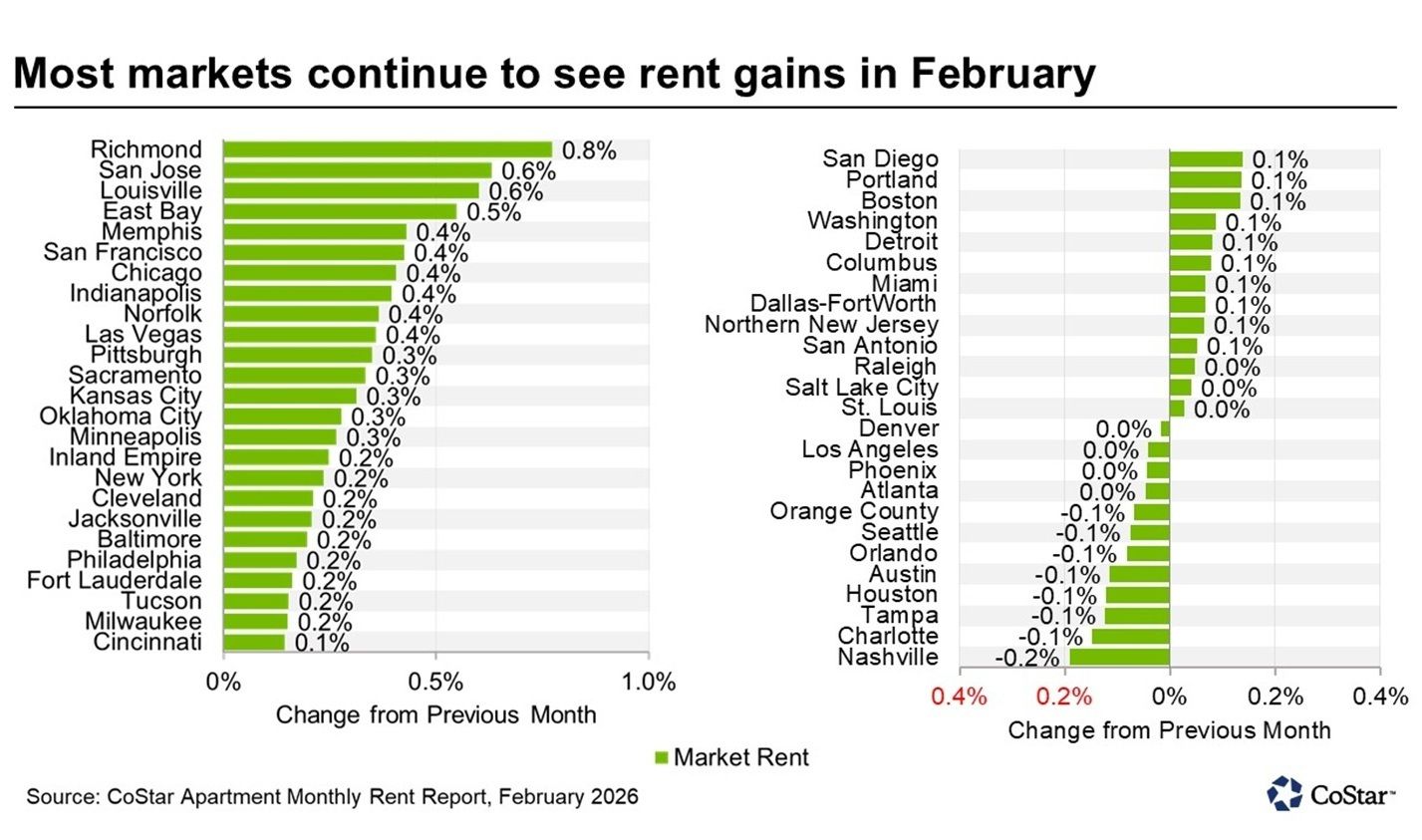

U.S. apartment rents increased in February, with the national average increasing to $1,716, a 0.1% increase from January’s upwardly revised figure of $1,714, according to Apartments.com's latest report on multifamily rent trends.

The monthly rent increase continues the trend of rising monthly rent changes that began in December 2025, but at a moderated pace. Prior to December, rents were flat or falling for five consecutive months. Annual rent growth eased marginally to 0.4% in February 2026 from 0.6% in the prior month and down from a 1.5% increase in February 2025.

While the rent change in February 2026 was positive, the increase was modest relative to typical February seasonality observed from 2010 to 2025, when rents increased by an average of 0.3%.

Supply pressures remain elevated and continue to temper rent momentum, resulting in uneven early-year gains that remain below typical February seasonal averages.

Across the U.S., 38 of the top 50 metropolitan areas posted rent increases, down from 42 in January. Areas posting the highest month-over-month rent increases were Richmond, Virginia, at 0.8%, San Jose, California, at 0.6% and Louisville, Kentucky, at 0.6%.

The steepest average monthly declines occurred in Nashville, Tennessee, down 0.2%, followed by Charlotte, North Carolina, Tampa, Florida, Houston, Austin, Texas, Orlando, Florida, Seattle and Orange County, California, where apartment rents decreased by an average of 0.1%. Many of these Sun Belt markets face elevated vacancy after newly constructed apartments opened, putting downward pressure on rents.

San Francisco posted the strongest annual rent increase at 5.7%, followed by Norfolk, Virginia, at 4.1%, San Jose, California, at 3.5% and Chicago at 3.0%. In contrast, apartment rents in Austin, Texas, recorded a 5.1% decline, while rents in Denver fell 3.4% and rents in Phoenix, Arizona, declined 3.3%, each reflecting oversupply outpacing demand.

During the rise of the internet in the 1990s, data center operators wanted to be near highly populated financial trading, commerce and government hubs like New York, downtown Los Angeles and Washington, D.C. Those geographic strategies look different today.

Northern Virginia, near the data-heavy federal government in Washington, D.C., is still considered the largest market for data centers, with what real estate services firm CBRE estimates is the capacity to use nearly enough electricity to power more than 3.5 million homes.

But the industry is heading further afield, with technology giants including Microsoft, Google, Meta and Amazon expanding into areas including southern Idaho, Texas' Big Country, Ohio, Indiana and the Midwest farmlands in search of lower-cost land and power.

The projects are part of an explosion in data and energy campus development across the United States — fueled by super-charged demand for computer processing power for artificial intelligence and cloud storage application — that is reshaping parts of rural America.

"Anyone who has land in core or secondary markets — and now farming areas — is trying to sell their site for multiples of what it's worth as data center land," said Andy Cvengros, JLL executive managing director and co-lead of the firm's U.S. Data Center Markets team, during a recent webcast.

At least 16 gigawatts of colocation and hyperscale data center space is under construction at new and expanding projects across North America, the highest amount on record, Andrew Batson, JLL's head of data center research in the Americas, told CoStar News.

Stocks exposed to the US housing market plummeted Wednesday amid depressing outlooks from companies like home improvement retailer Lowe’s. Investors also reacted to the lack of a housing policy update during President Donald Trump’s State of the Union speech. The S&P composite homebuilder index shed as much as 5.2%, the most since last April’s “liberation day” market meltdown.

Earlier this week, Home Depot’s Chief Financial Officer Richard McPhail said that “the homeowner is one of the healthiest customer cohorts out there, but they tell us that uncertainty is growing, that there’s concern around housing affordability, around job losses.”

Meanwhile, Lowe’s Chief Executive Officer Marvin Ellison on Wednesday said that “consumer confidence remains subdued given inflationary pressures and overall economic uncertainty.” He also flagged high mortgage rates, leading to a “persistent lock-in effect,” and slow new home building.