- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 021024

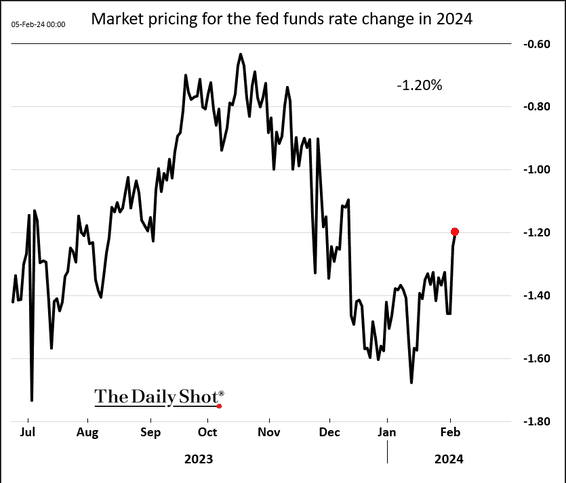

Well it was an exciting week with Federal Reserve Chair Jerome Powell confirming last Sunday that the Fed won’t wait for inflation to 2% before it starts cutting rates. Long term readers will know Location Strategy has been telling you this for almost a year. The pressures in the banking system, particularly community banks, as well as political pressures related to financing the Federal Debt will be too great.

Again Powell said they were not battling the housing market, but if ±40% of the CPI is the cost of housing, if you are fighting inflation you are fighitng the housing market. To his credit, Powell acknowledged that he controlled virtually none of the levers, save interest rates, to affect housing affordability. We can only hope that his interview is a coda to a series of sorry and tragic policy mistake sthat began with Tony Fauci’s announcement in 2012 of his plan to develop a “supercoronavirus” against which vaccines could be made.

Location Strategy Chartbook

The total expected rate reduction in 2024:

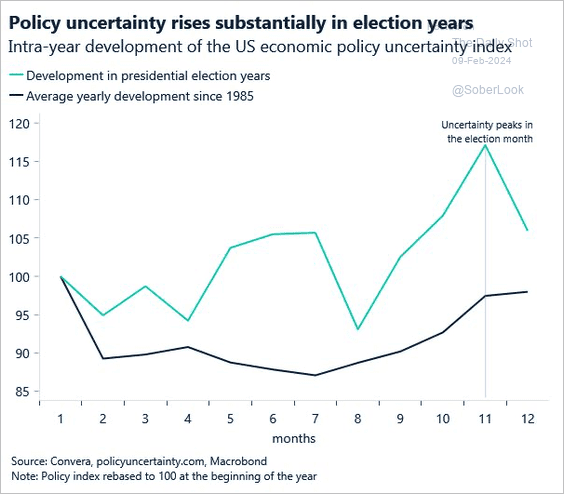

Policy uncertainty rises substantially in the months leading up to a US presidential election.

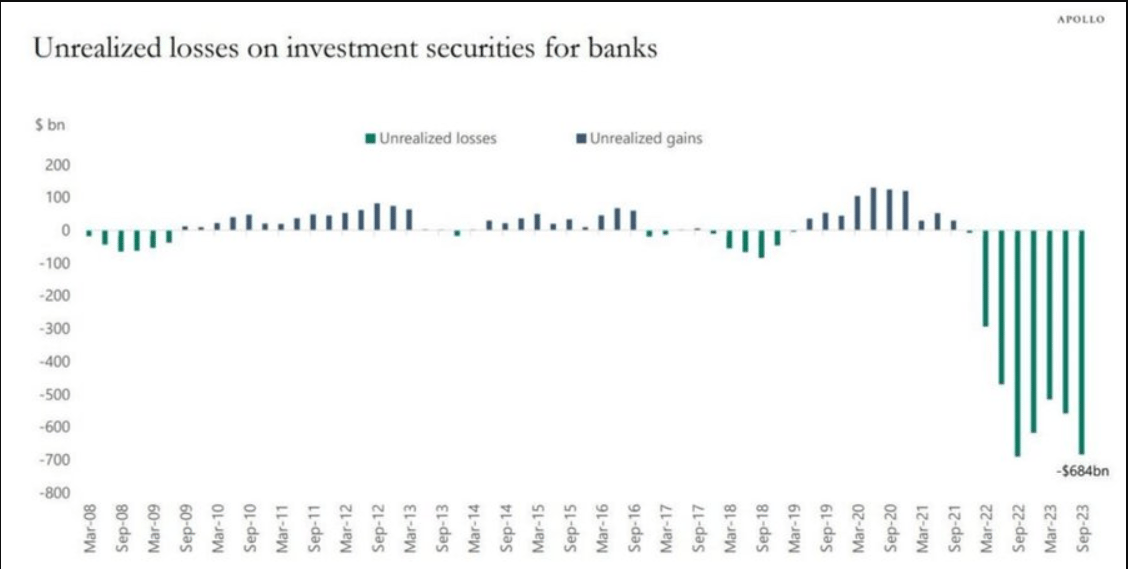

Banks Still Have Huge Unrealized Losses

As the Federal Reserve began printing money in 2020-2021, banks had to put it somewhere an there were rules that defined the kinds of securities they could invest in. When rates began rising, they rapidly eclipsed the returns on these securities. In way, this is similar to what caused the Savings and Loan Crisis in the 1980s.

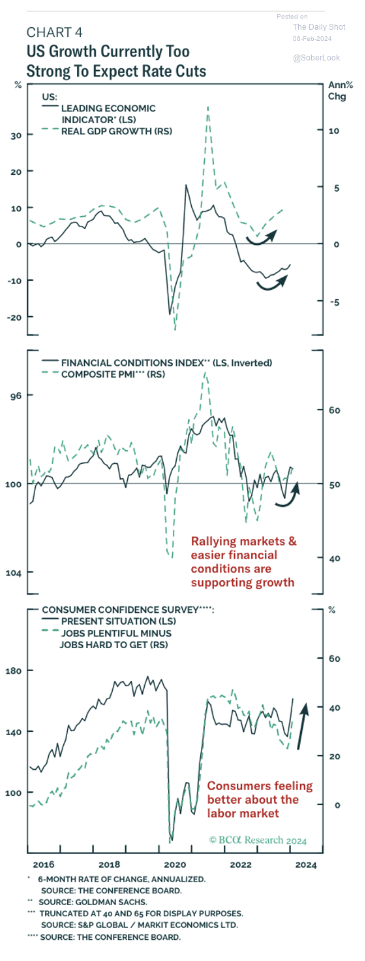

The resilient economy could delay Fed rate cuts.

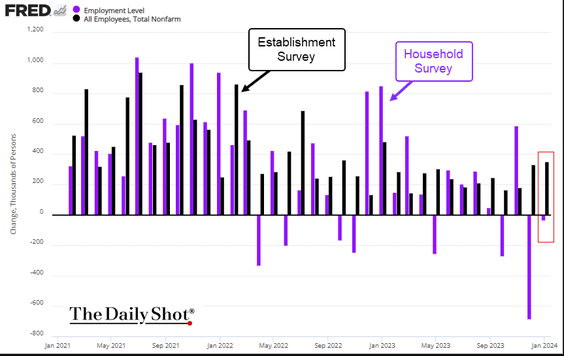

However, the Household Survey once again showed a decline in jobs, further diverging from Establishment Survey (above).

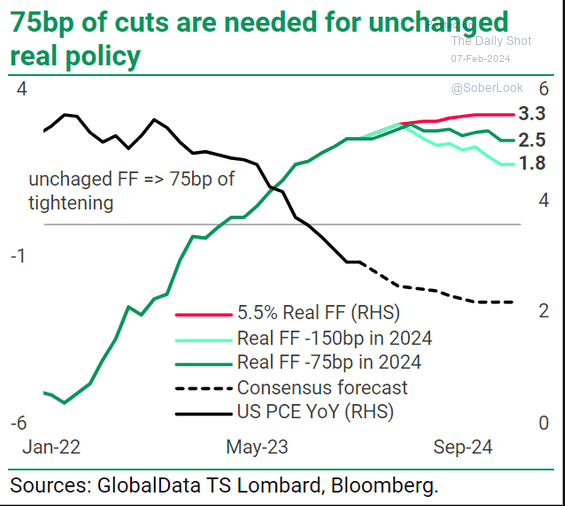

With current expectations of reduced inflation ahead, the Fed would have to lower rates by 75% basis points merely to maintain the current tightness of monetary policy.

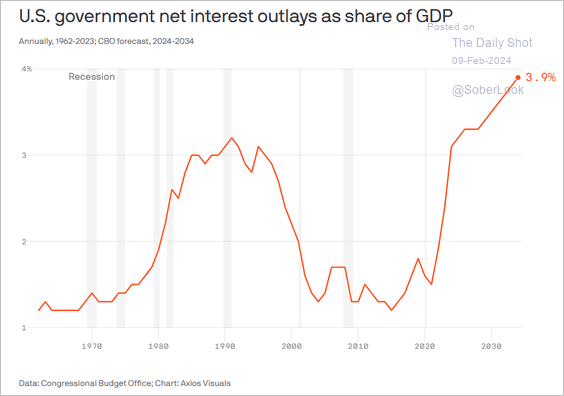

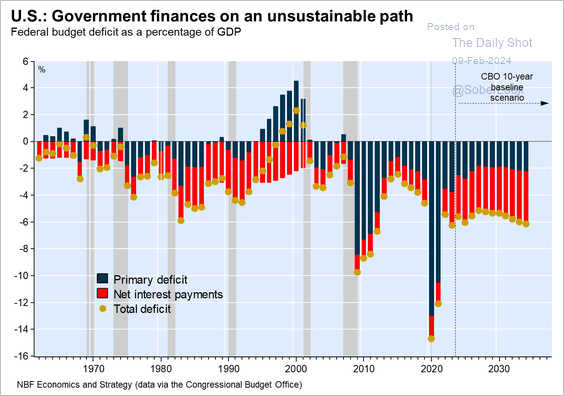

However, the government’s key challenge will be soaring interest expenses,

… blowing out the total budget deficit.

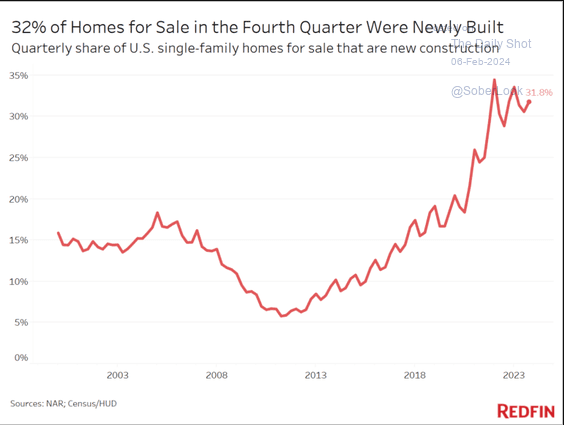

New Homes continue to represent over 30% of the total housing market listings.

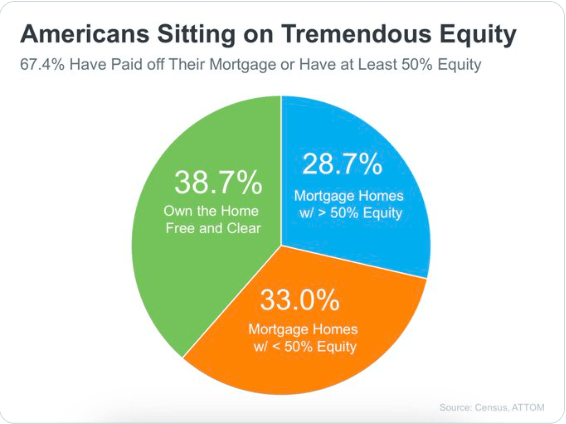

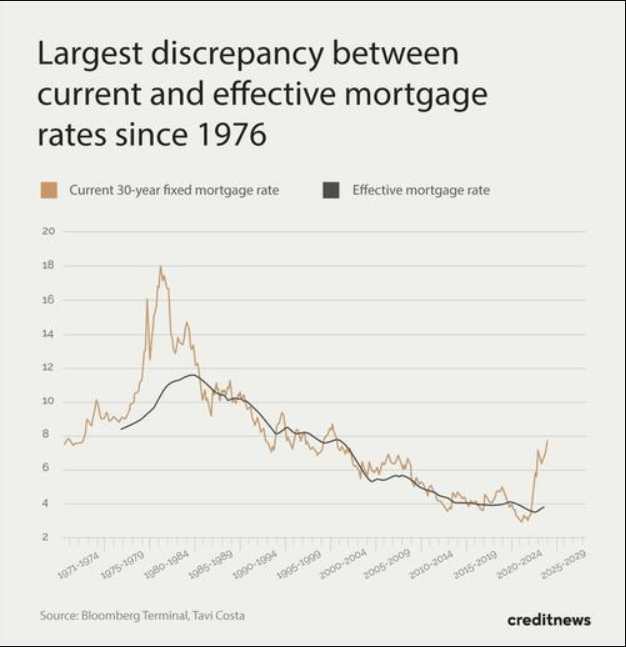

39% of Americans Don’t Have a Mortgage

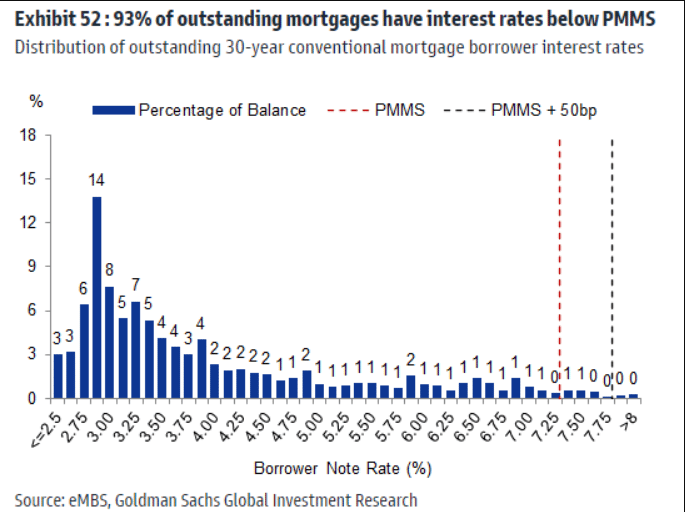

93% of outstanding mortgages have interest rates below the going market rate.

More than 40% of all U.S. mortgages were obtained in 2020-2021 when interest rates were at rock bottom. And nearly two-thirds of current mortgage holders locked in rates below 4%—almost 3 percentage points lower than the current 30-year mortgage rate.

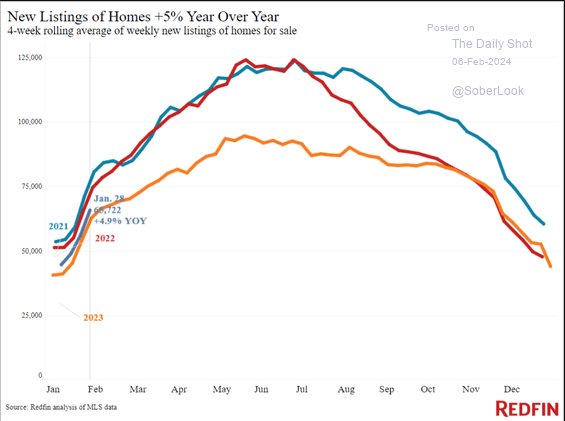

New Listings have been running slightly above 2023 levels.

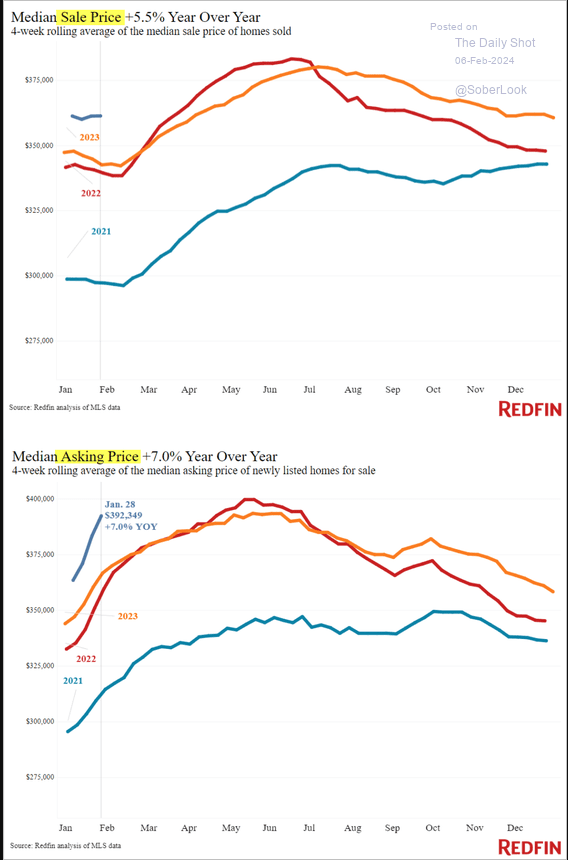

Asking and sale price are at record highs for this time of the year.

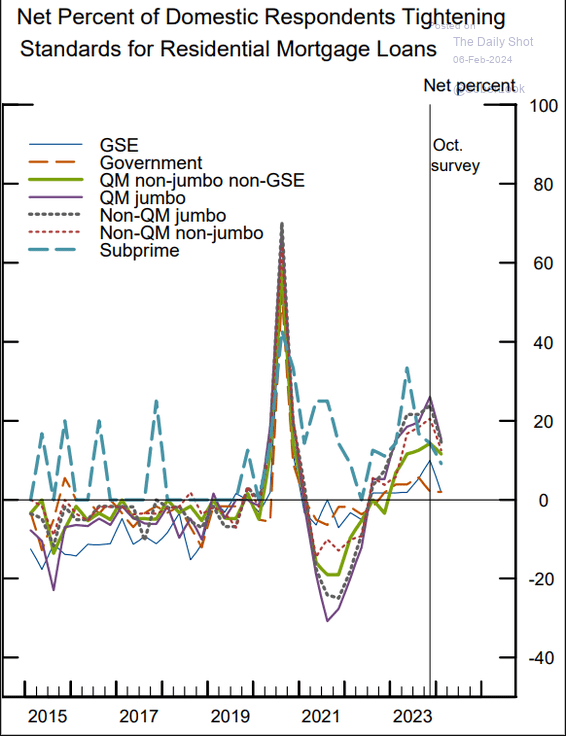

Fewer banks are tightening lending standards on mortgages.

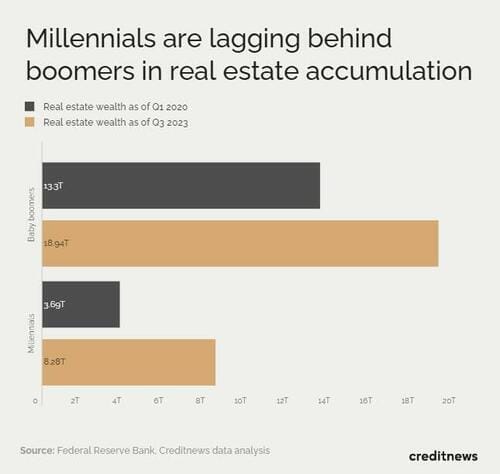

Baby boomers have the upper hand in the homebuying market," said Dr. Jessica Lautz, NAR deputy chief economist, adding: "The majority of [boomers] are repeat buyers who have housing equity to propel them into their dream home—be it a place to enjoy retirement or a home near friends and family. They are living healthier and longer and making housing trades later in life.

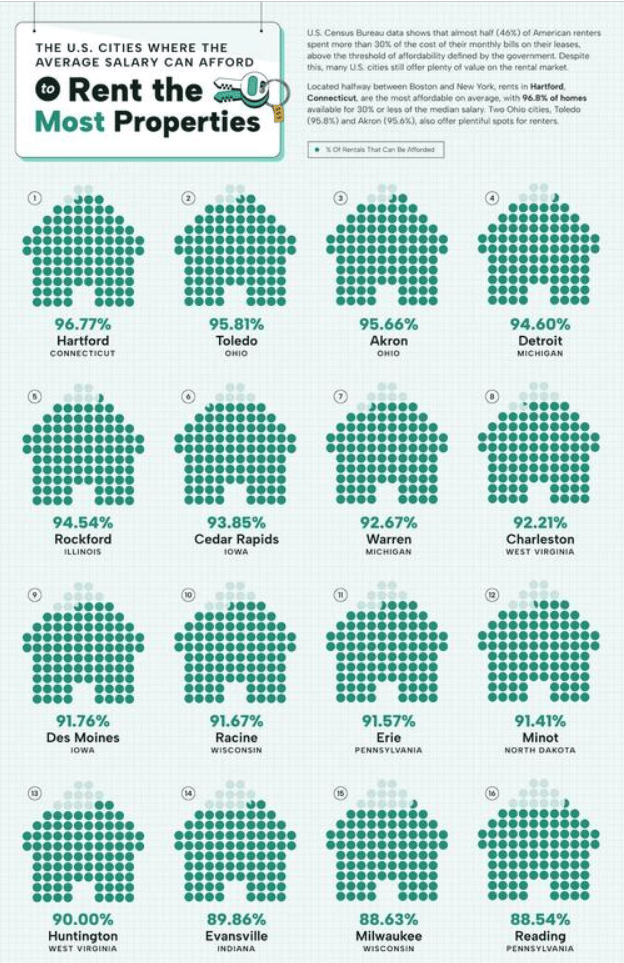

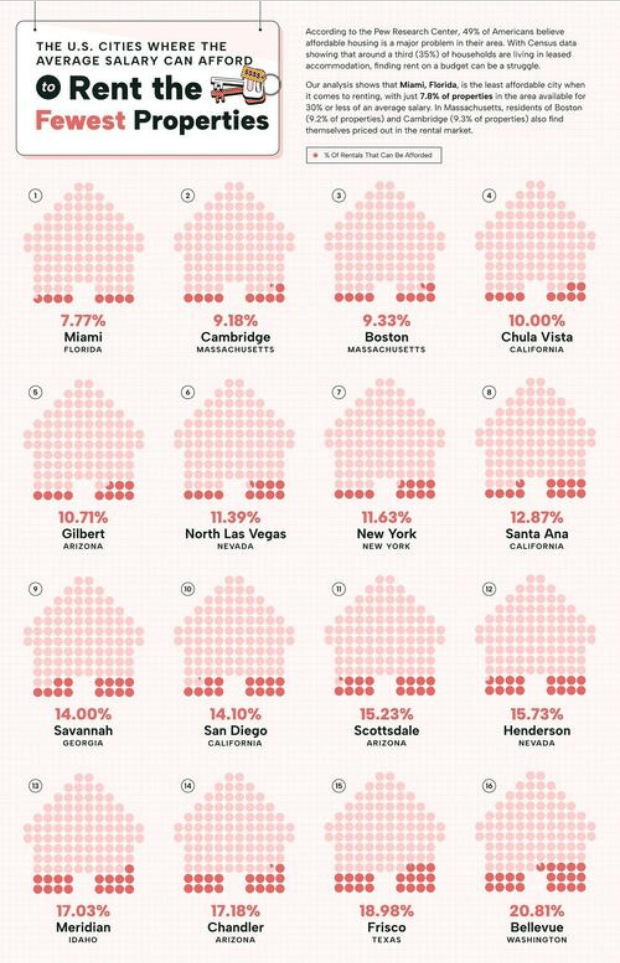

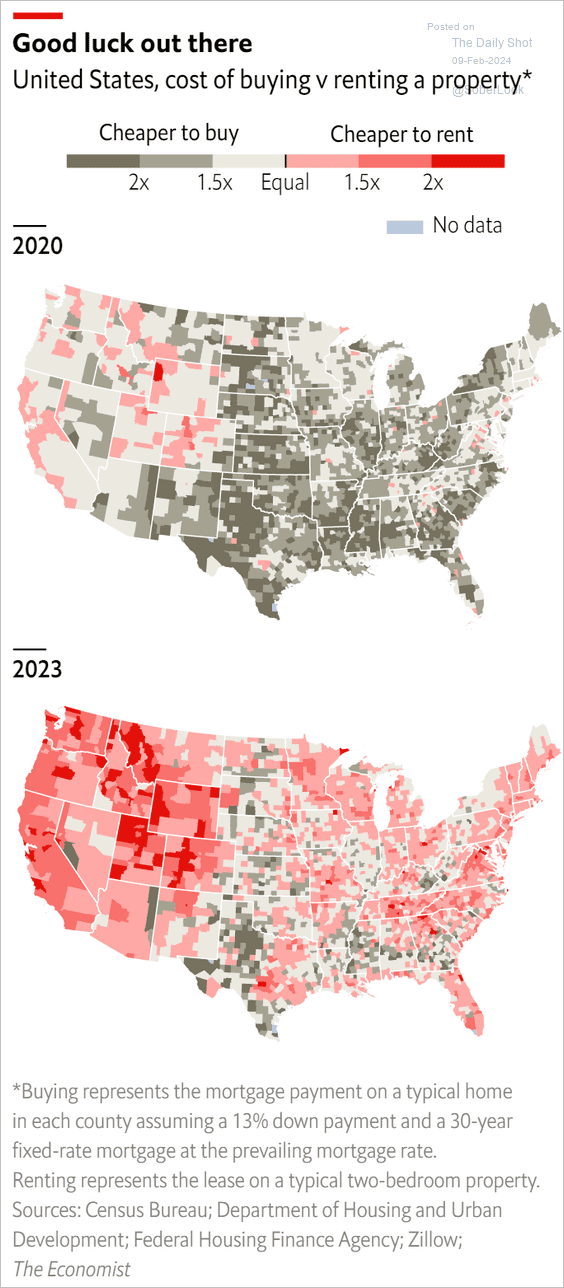

Cheaper to rent or buy?

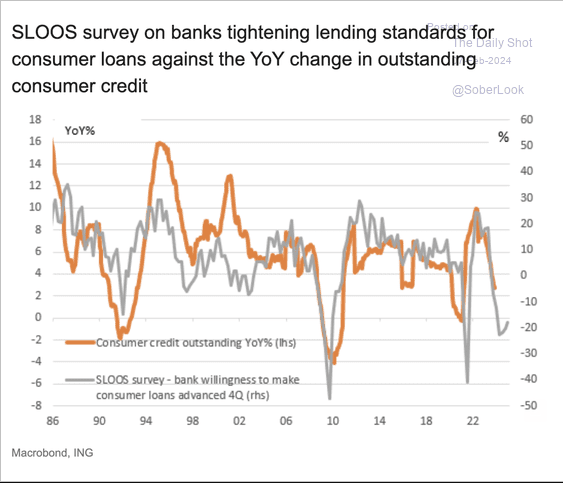

Tight lending standards still signal a slowdown in consumer credit ahead.

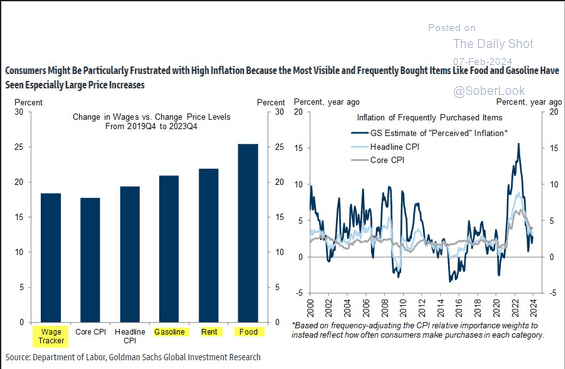

Despite recent slowdowns in price increases. Americans still perceive inflation as high, attributed to the elevated costs of highly visible and frequently purchased items.

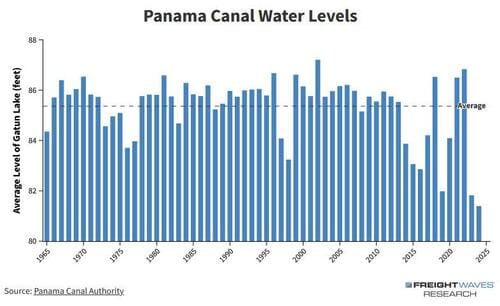

Low Panama Canal water levels causing 6 day delays in shipping to eastern ports