- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 03.14.2026

Location Strategy Chartbook 03.14.2026

Real Estate Market Insights

Prices at the pump now at 22-month high

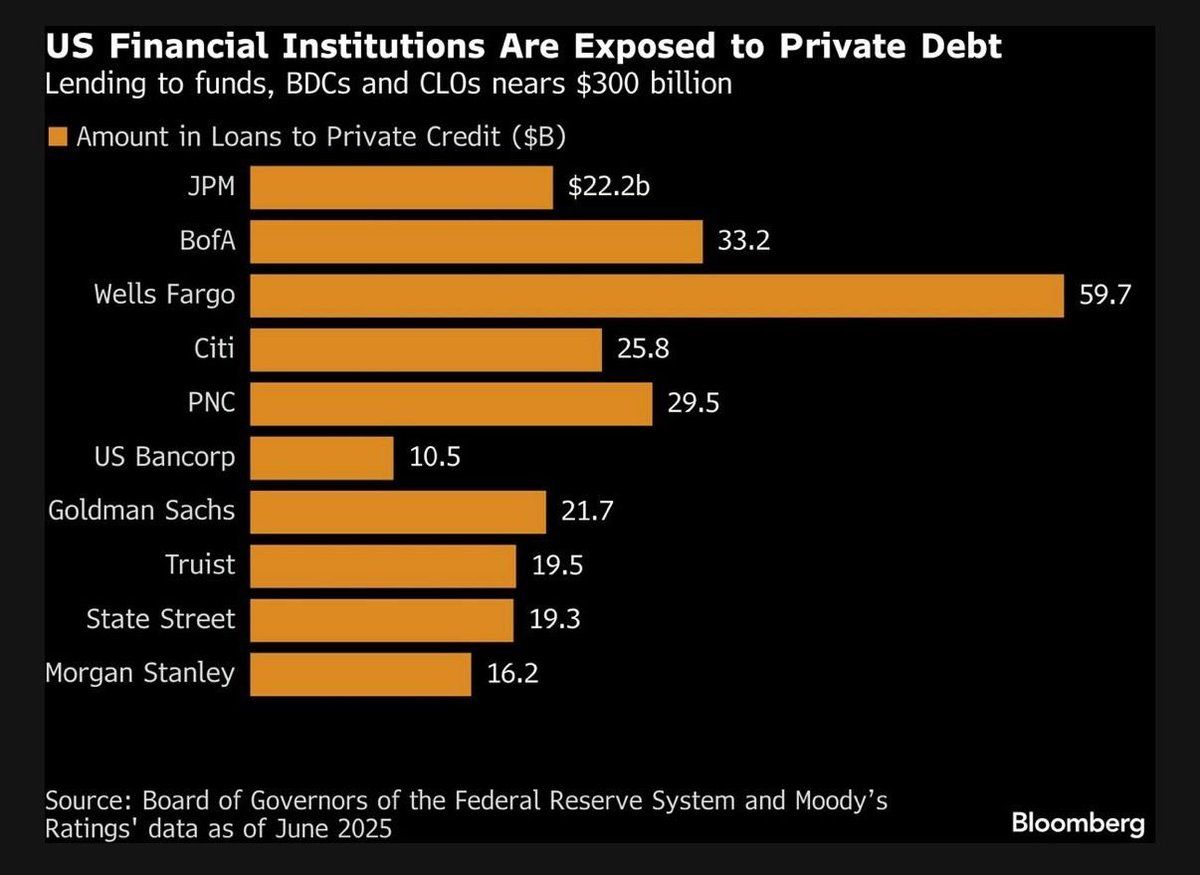

The Office of Financial Research, an independent agency housed at the US Treasury Department, said in a report Thursday that private credit fund borrowing could be as high as $345 billion — though it urges interpreting the figure “with caution.”

“Our analysis of fund-level data indicates that reported borrowings by some private credit funds may underestimate leverage,” said the paper, authored by Ted Berg and Jung Hoon Lee.

Banks are already under pressure. The concern is likely to intensify in coming months, especially as investors ask how much banks stand to lose if a lot of private loans drop in value.

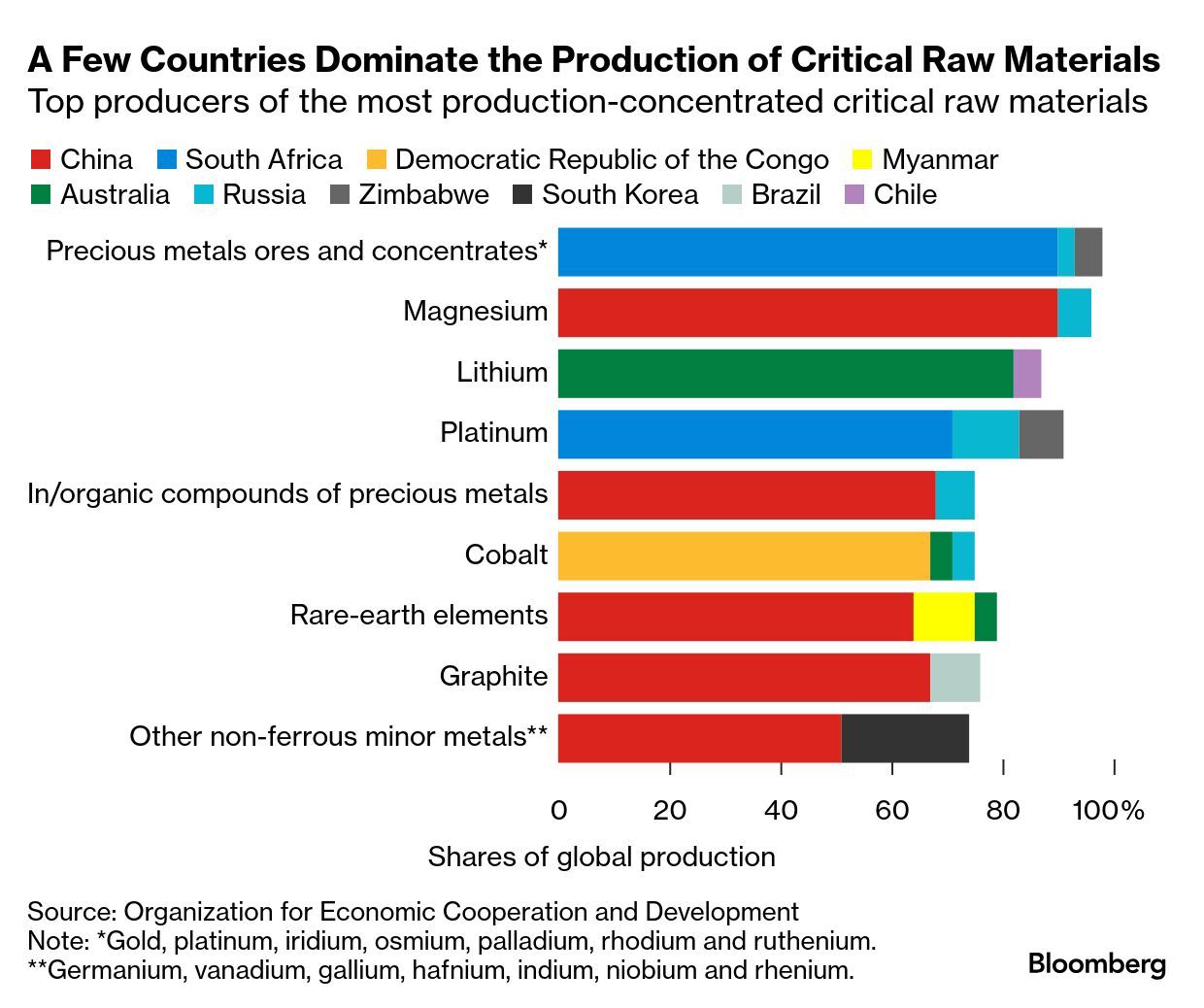

The US, Japan and the European Union are said to plan an announcement in the coming weeks about laying the foundation for a trade agreement in critical minerals. The Office of the US Trade Representative, which has led negotiations with Brussels and Tokyo on the framework, will also head talks for a trade deal that is set to include a price floor and tariffs for the materials to counter any market distortions by China.

Global efforts to diversify critical minerals supply chains intensified after Beijing last year imposed sweeping export controls, including on rare earths and critical minerals, in response to Trump’s global trade war. Beijing has threatened it would retaliate against the formation of a bloc that would target its exports.

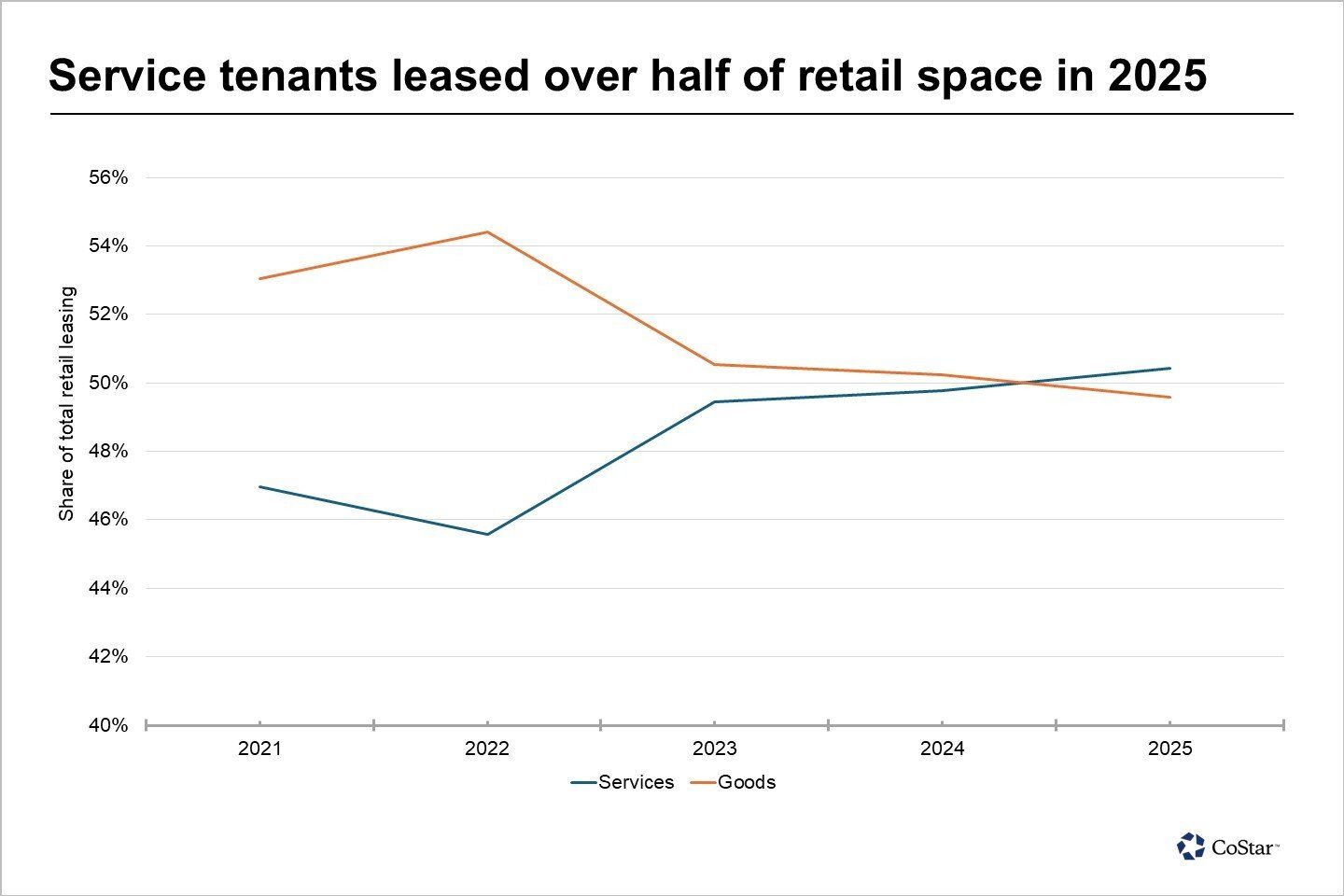

For the first year on record, service-based retailers leased more space than traditional goods-based tenants.

And while the margin was narrow, 50.4% services to 49.6% goods, the crossover is meaningful as it reflects the long-running reallocation of consumer spending and the continued evolution of physical retail space toward uses that are less vulnerable to e-commerce.

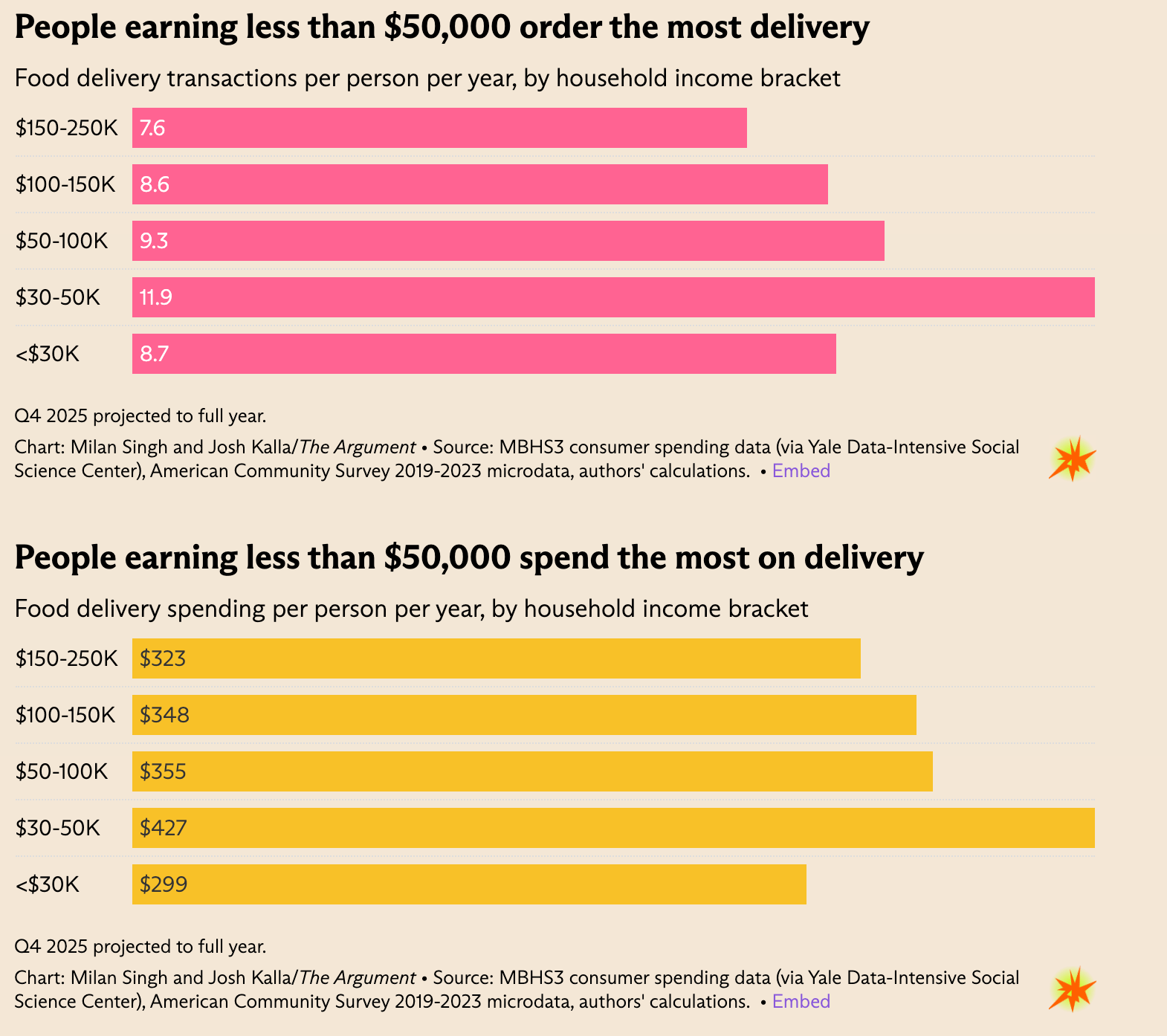

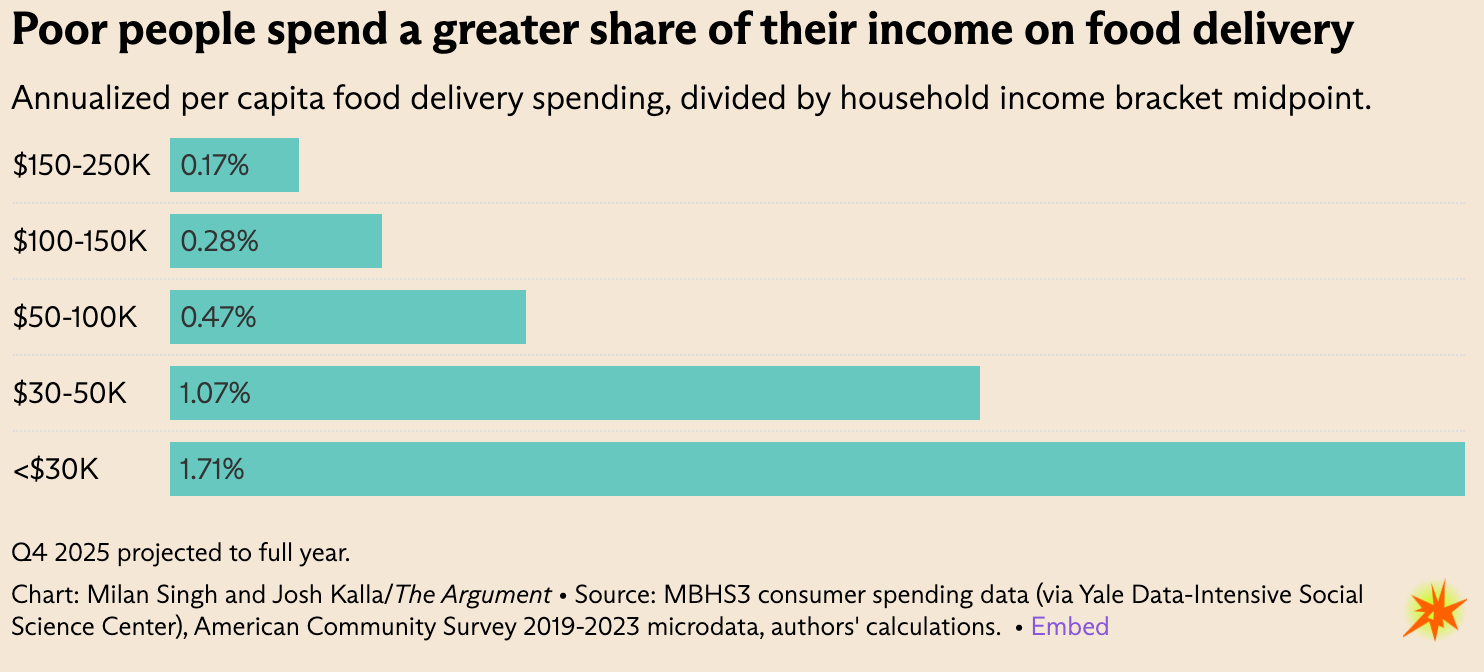

The Argument: Nearly 75% of all restaurant meals are consumed off-premises. Takeout and drive-thru play a large part, but in recent years, the explosion of meal delivery through platforms like DoorDash has fundamentally reshaped consumption patterns.

What about delivery spending as a share of household income? After all, spending $100 on delivery is much more of a splurge for a college student than for a professional in their 30s.

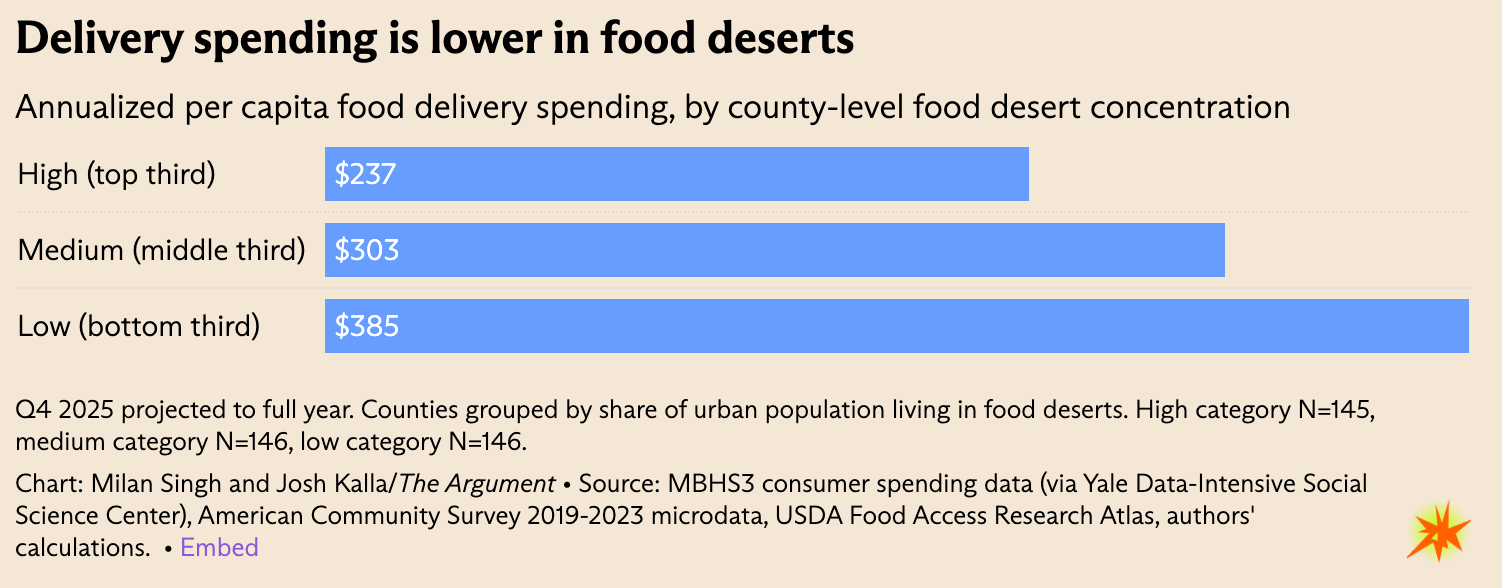

The availability of grocery stores was not a driving factor in whether someone used food delivery services; in fact, there was an inverse relationship between the two.

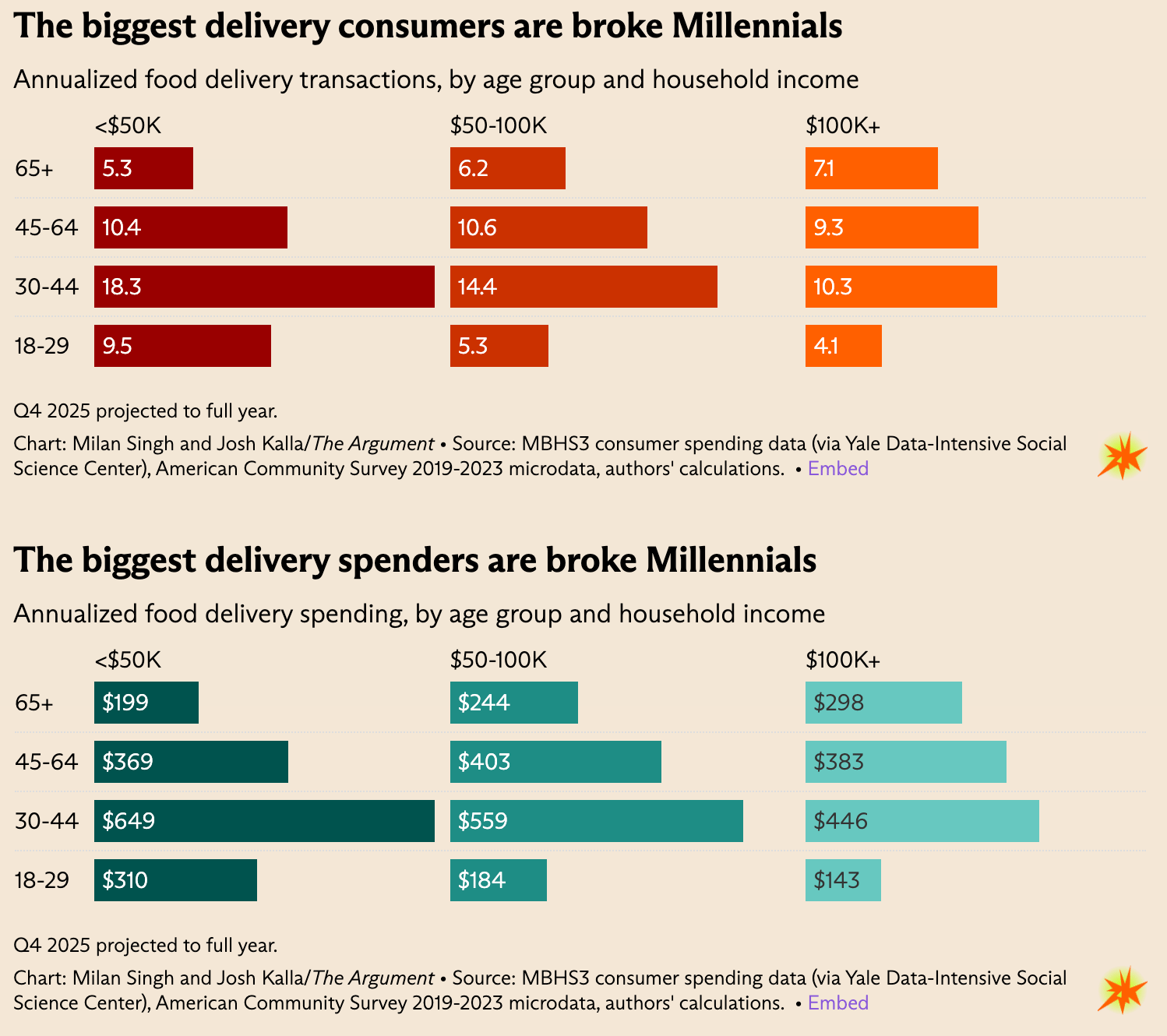

The people who order the most DoorDash aren’t the very young; they’re people in their early 30s to early 40s.4 More specifically, they’re people in their 30s and 40s who don’t make very much money.

Look at annualized delivery transactions, broken out by income bracket and generation. The biggest DoorDash customers are people in their early 30s who make $50,000 or less.

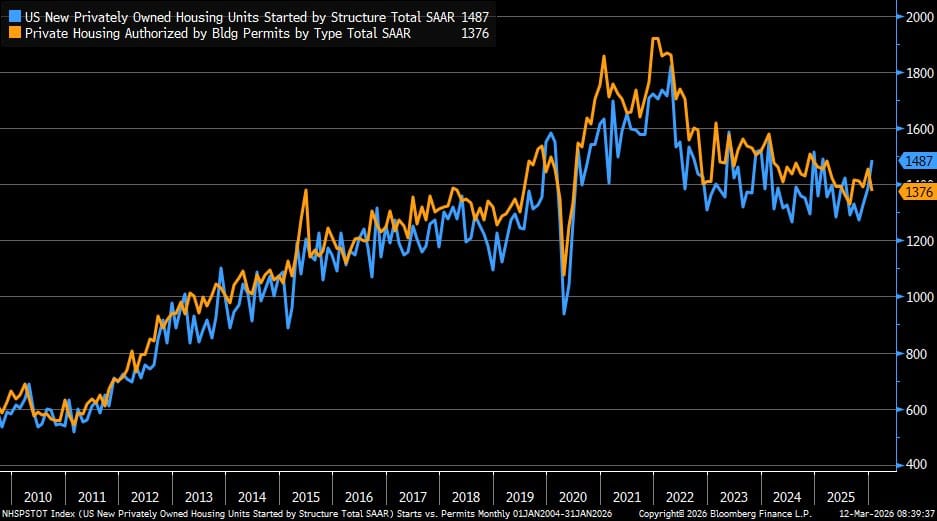

Liz Ann Sonders, Schwab: Divergence of late between stronger housing starts (blue) and weaker building permits (orange) … latter remains in a downtrend over past couple years

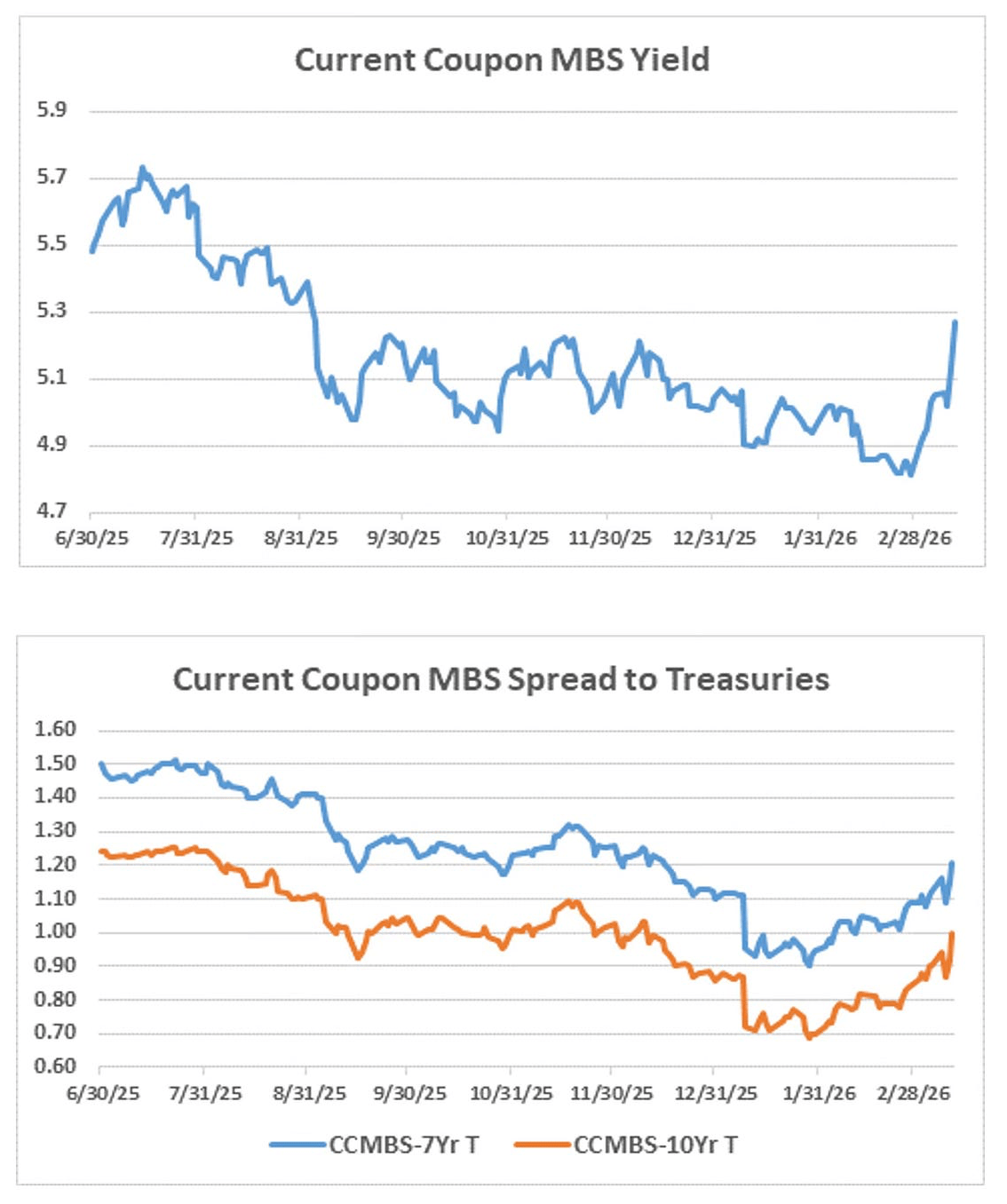

Bill McBride, Calculated Risk: Yesterday current-coupon MBS (CCMBS) yields jumped to their highest level since early September of last year, and CCMBS/Treasury spreads increased to their widest levels since the middle of last December. Surging oil prices and uncertainty about the duration and the ramifications of the Iran war – inflation, growth, fiscal, etc. – not only put upward pressure on overall interest rates, but also led to significant increases in actual and implied interest rate volatility. Higher interest rate volatility, of course, generally causes CCMBS yields to rise relative to Treasury yields because of the embedded prepayment option in the mortgages backing MBS. This heightened uncertainty also led to increased implied volatility in other markets, including the stock market.

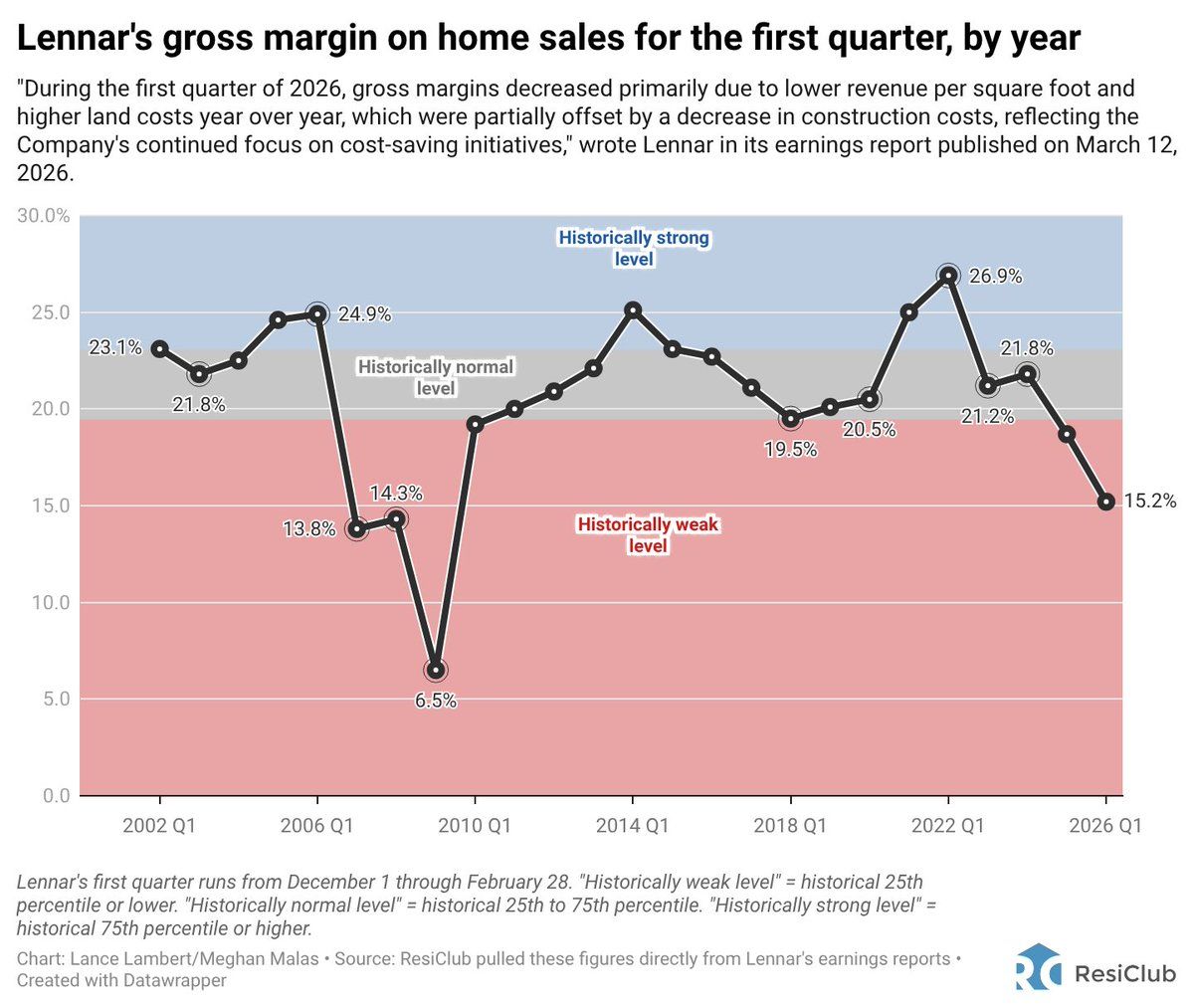

Lennar—America's second largest homebuilder—gross margins fall to the lowest levels since 2009

Among giant public homebuilders, Lennar has been the most aggressive in using affordability adjustments/incentives to maintain volumes/take market share

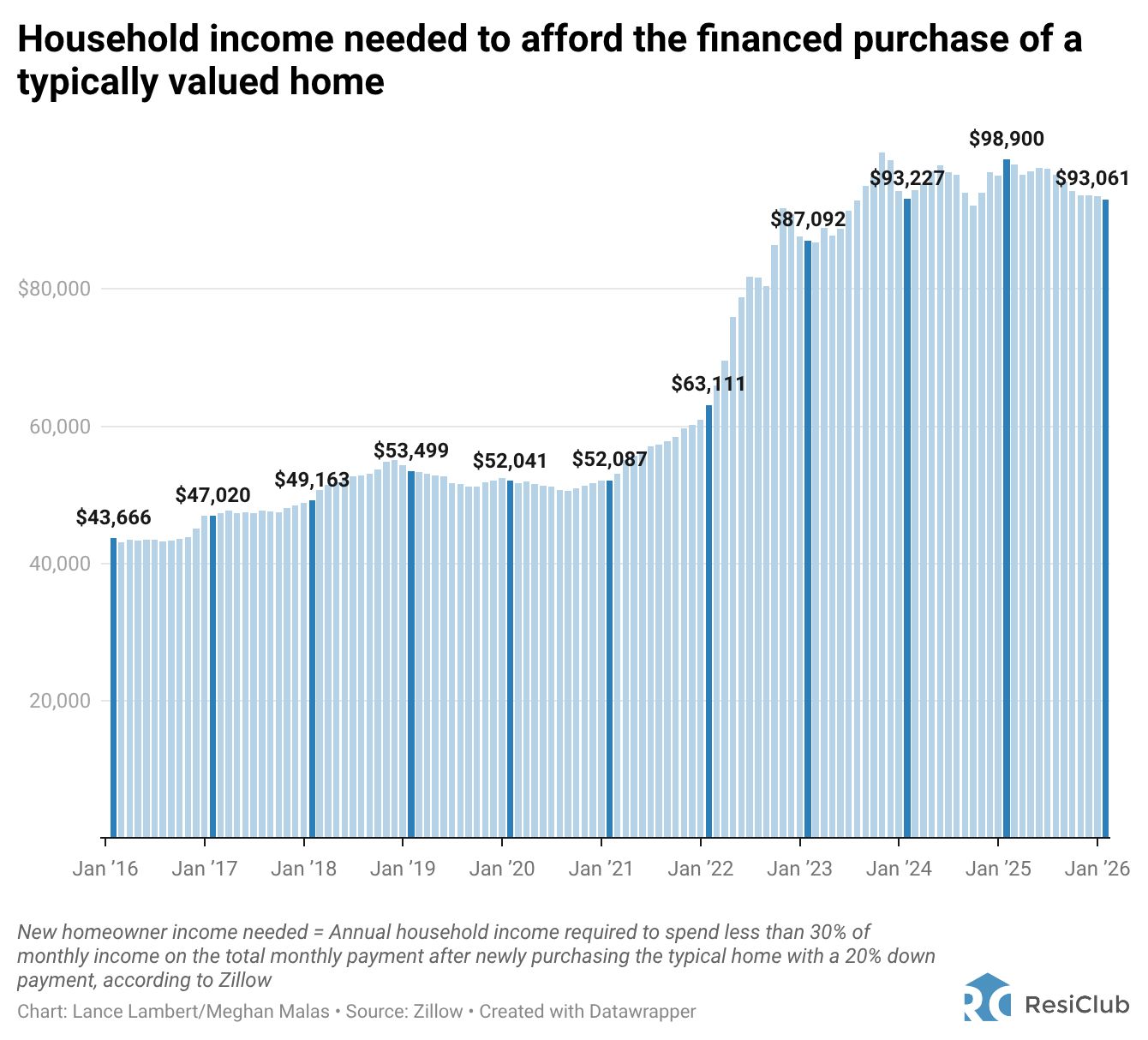

Here’s the annual U.S. household income needed to purchase the typical valued U.S. home

While the income needed to buy the median-priced U.S. home is +78.8% higher than it was in January 2020, it’s down -5.9% year-over-year. Methodology: This Zillow calculation is conservative and assumes a 20% down payment and the homebuyer spends less than 30.0% of their monthly income on the total monthly payment. This is a financed purchase, of course. For typical home value, Zillow economists used the latest Zillow Home Value Index reading.

Jan. 2020 -> $52,041

Jan. 2021 -> $52,087

Jan. 2022 -> $63,111

Jan. 2023 -> $87,092

Jan. 2024 -> $93,227

Jan. 2025 -> $98,900

Jan. 2026 -> $93,061