- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 03.28.2026

Location Strategy Chartbook 03.28.2026

Real Estate Market Insights

Inflation and bond markets have been pricing in the short-term effects of higher energy prices, but not a medium-term AI disinflation scenario. If investors begin assigning greater weight to this probability, it could provide a counterbalance to the short-term concerns and push short-term bond yields and inflation swaps lower.

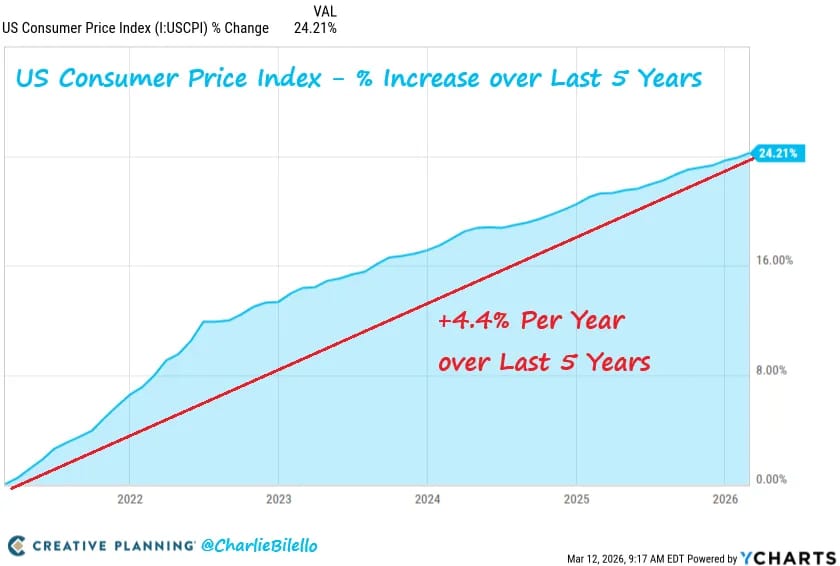

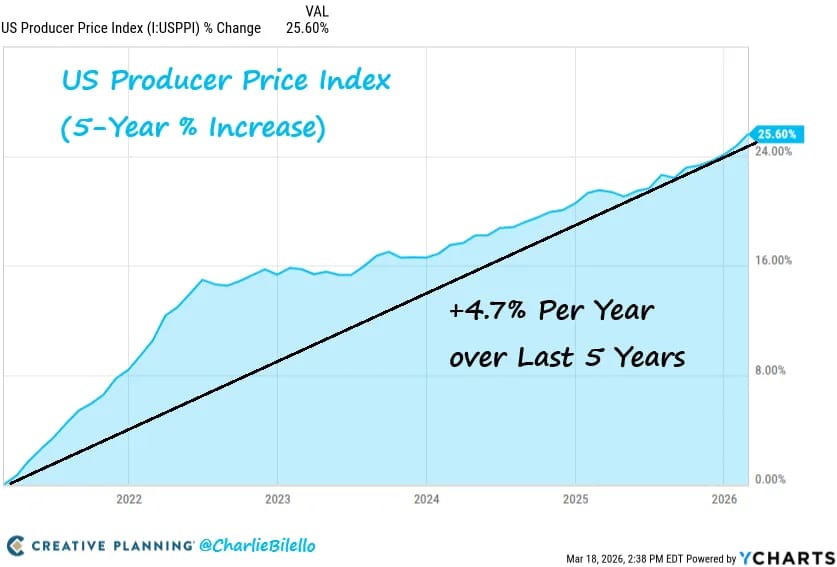

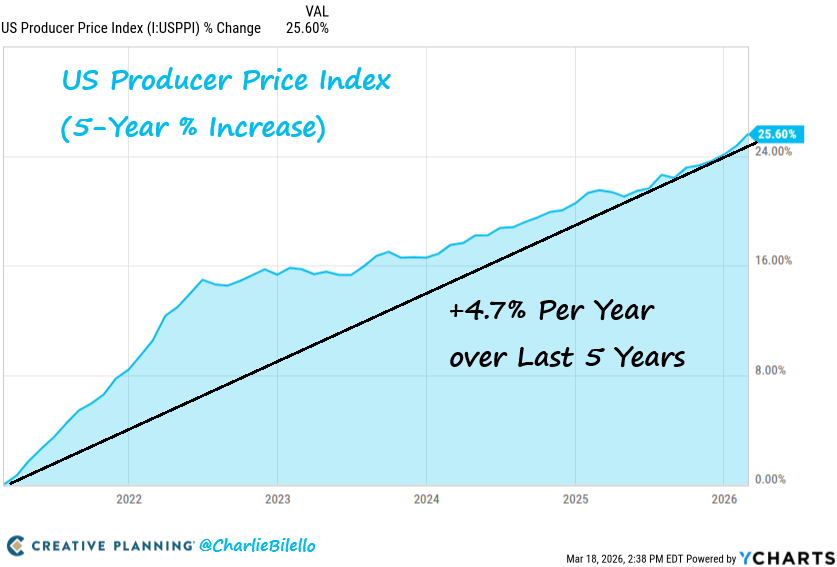

Both Consumer (CPI) and Producer (PPI) prices in the US have risen at a rate of more than double the Fed’s 2% target over the past five years.

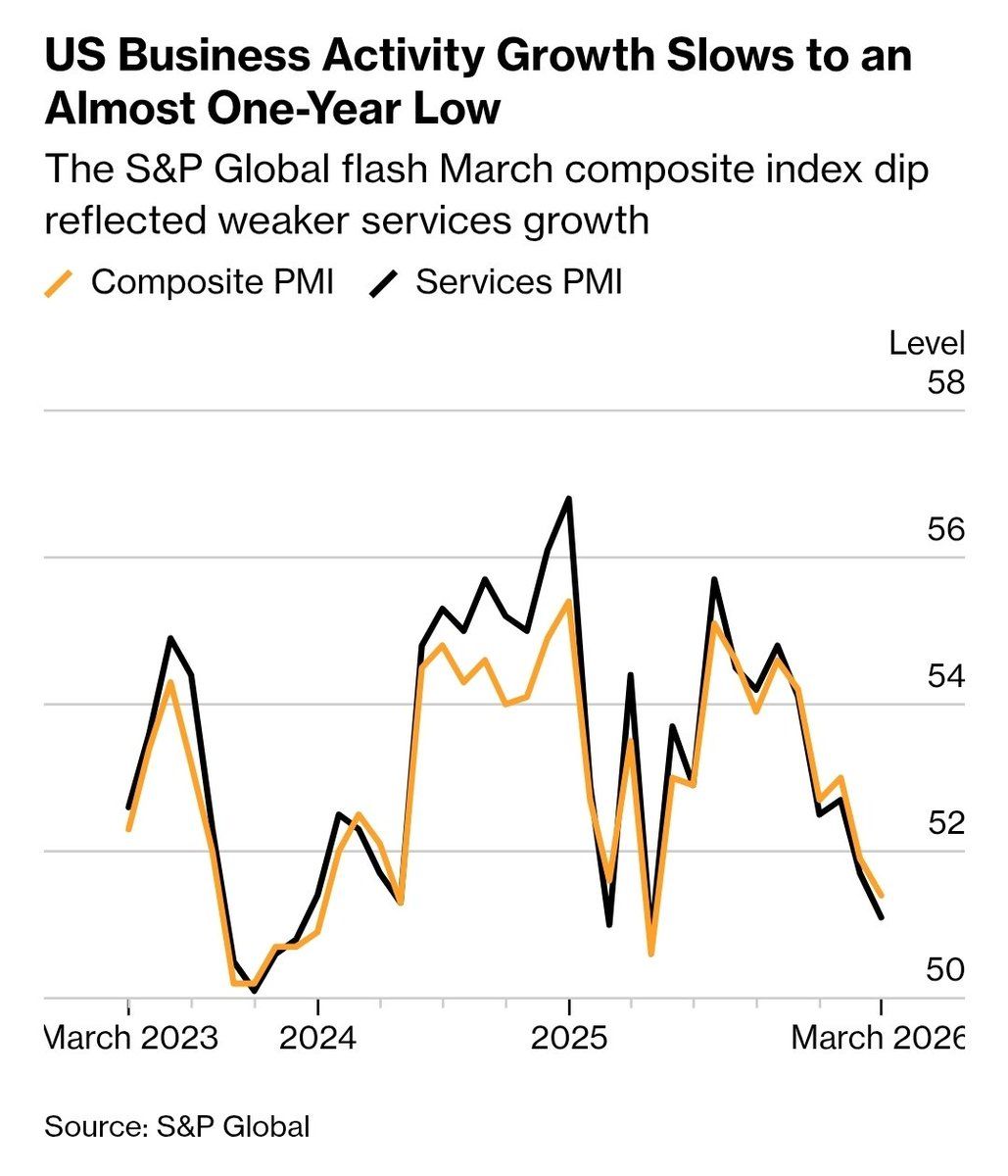

Input prices for services rose to the highest since May 2025, while those for manufacturers jumped to a seven-month high.

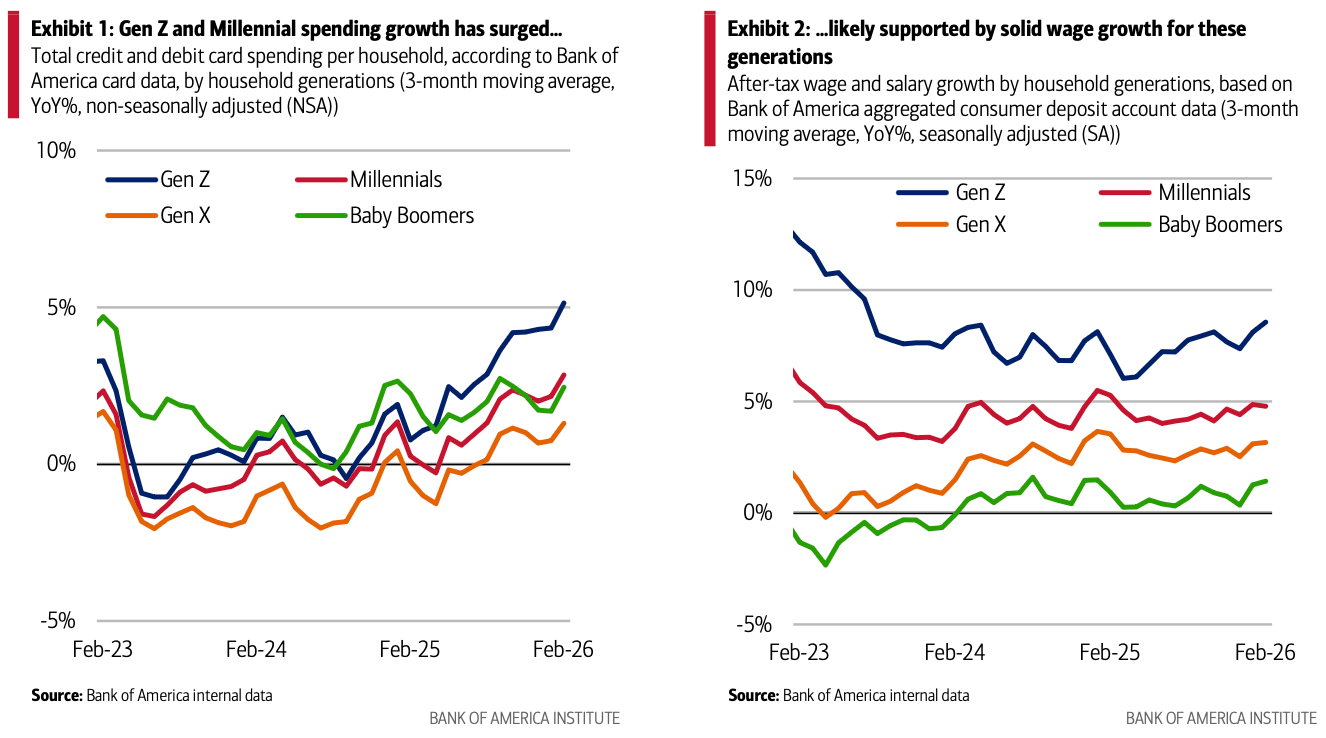

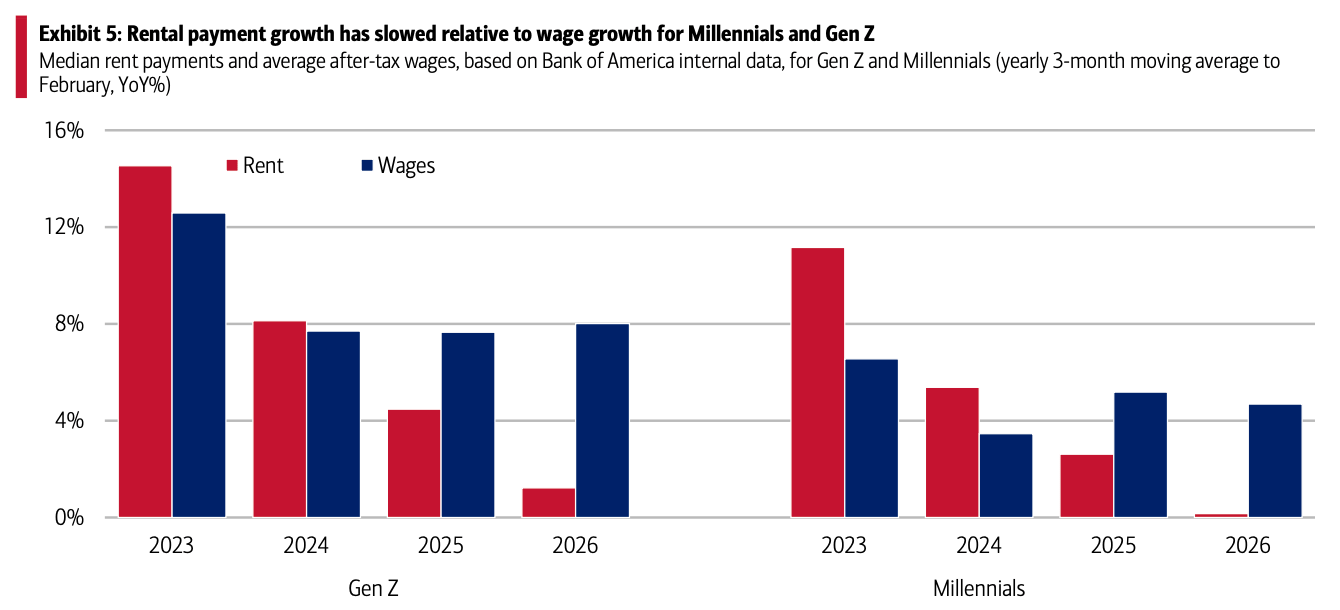

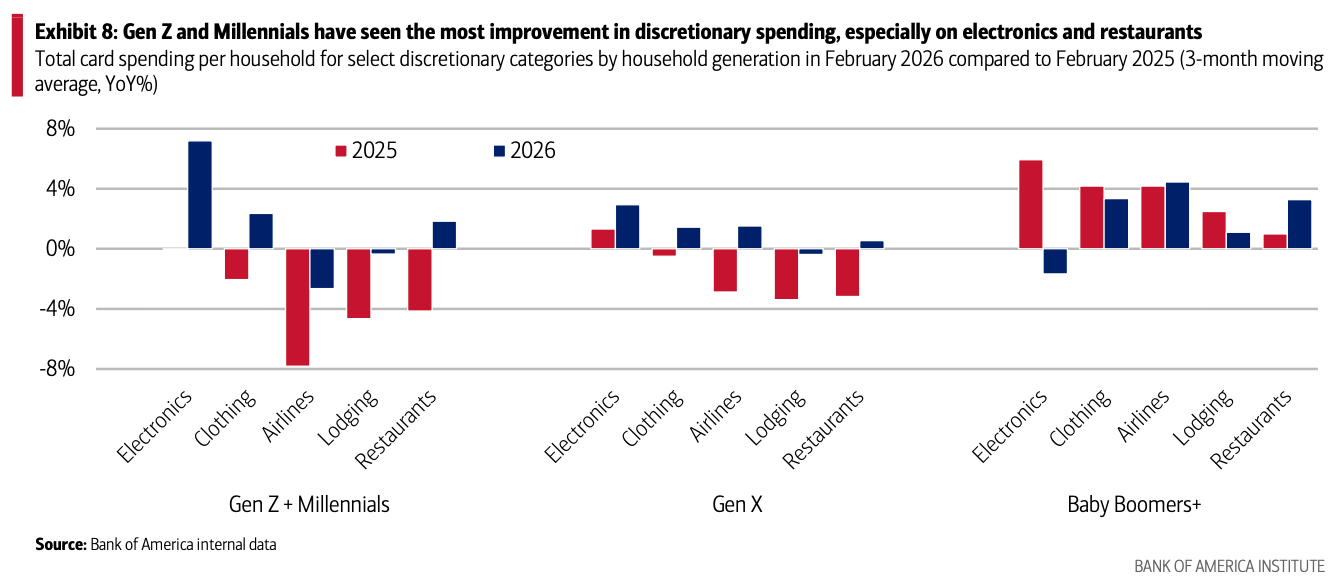

• Gen Z and Millennials have seen an improvement in their spending growth over the last year: in Bank of America credit and debit card data, younger generations' spending growth was higher than older generations as of February 2026.

• What's driving this? In our view, easing rent pressures are a key factor. Younger consumers are seeing rent payment growth below their wage growth according to our data. As a result their spending on discretionary items such as electronics, clothing

and restaurants has improved. Tax refunds are an additional tailwind.

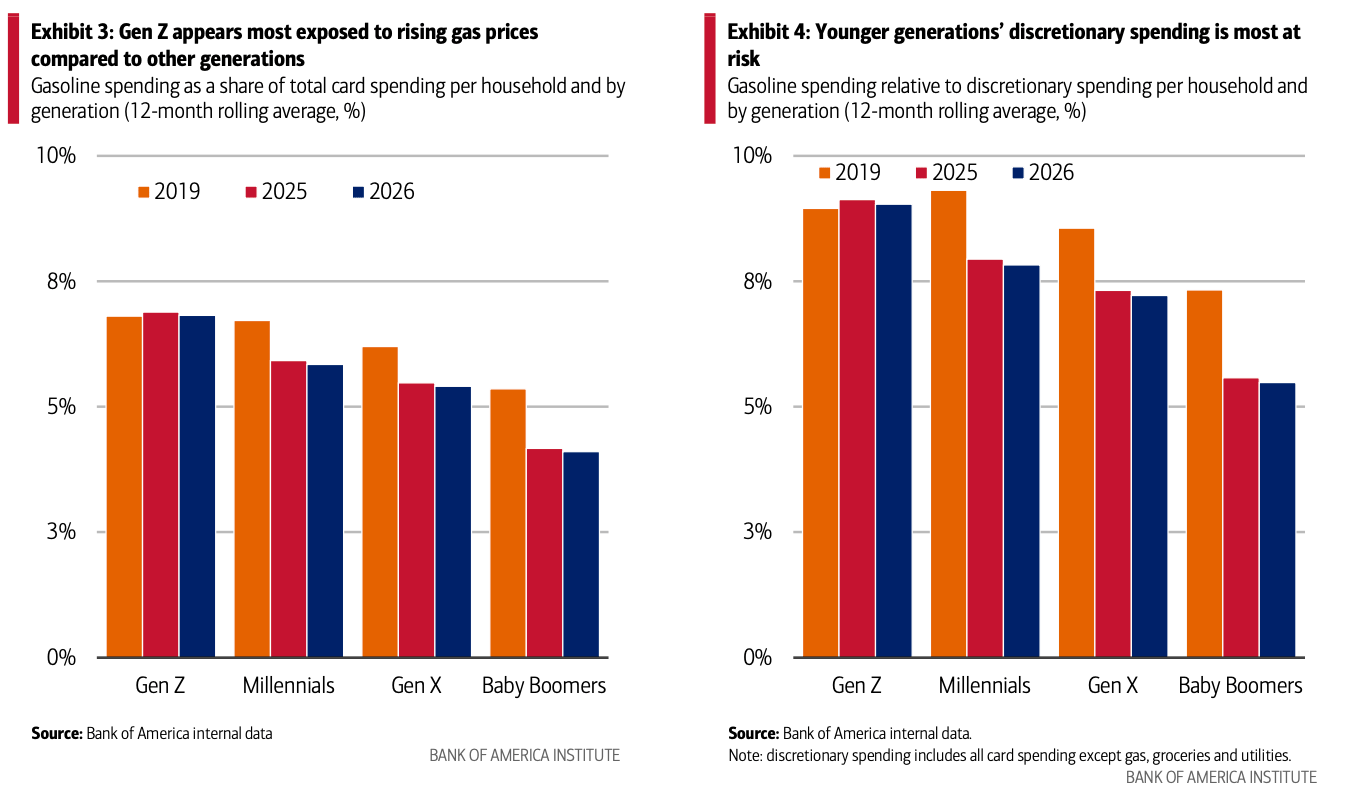

• But the current oil shock poses risks to this picture. Younger generations' gasoline spending is relatively high compared to their discretionary spending, so there is the potential they will need to pullback most aggressively in the face of higher gasoline prices. Further out, while the overall labor market may be "low-hire, low-fire", it poses particular challenges for Gen Z, with potential knock-on headwinds to their spending.

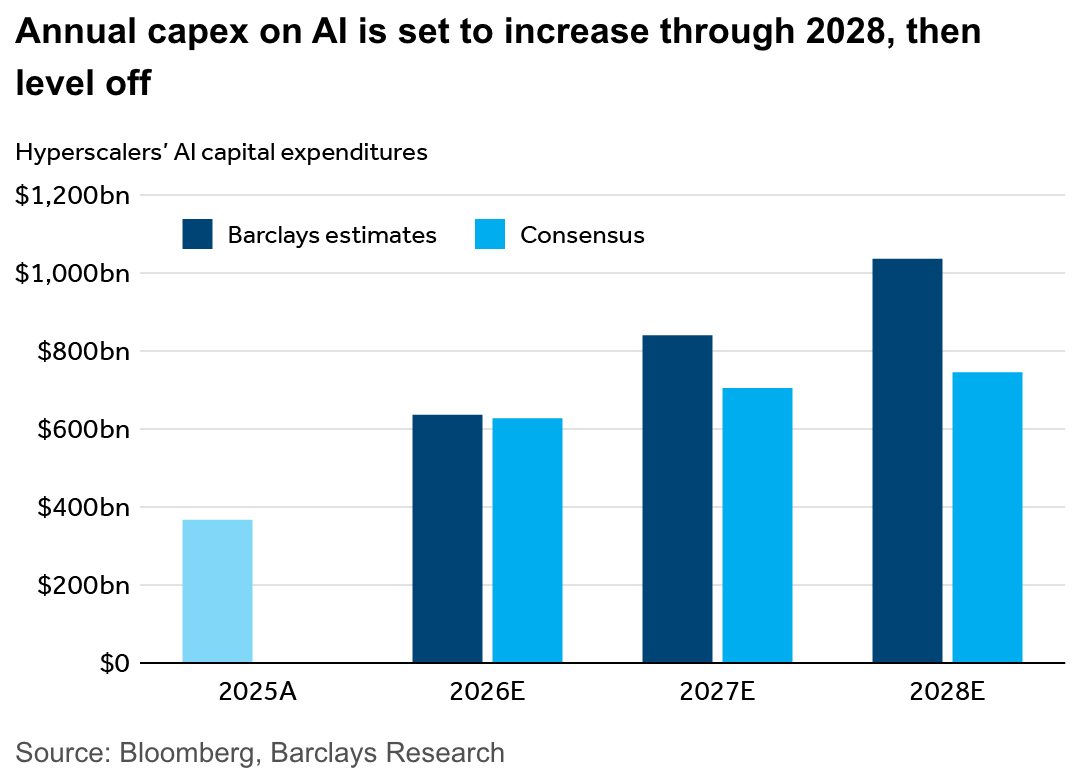

AI has been moving faster in early 2026 than many expected, with leading labs reporting big jumps in annual recurring revenues. As adoption by consumers and companies widens, demand for computing power keeps growing too. Against this backdrop, the largest technology firms will spend an estimated $2.5 trillion on AI buildout in the next three years, our analysts estimate.

As of the end of 2025, total available office space across the Nashville market stood at 15.2 million square feet, with approximately 14.6% of that inventory being marketed as sublease space.

In comparison, in the first quarter of 2023, total available space peaked at roughly 16.7 million square feet, with sublease offerings accounting for 17.3% of availability. The decline in sublease availability marks a notable shift from recent years, reflecting fewer large tenants shedding excess space.

Major corporations such as Oracle and Amazon are driving office demand in Nashville, and the arrival of Starbucks, which is reportedly seeking 250,000 square feet of available office space, will further augment demand.

With over 3 million square feet of new office space constructed just in the past two years, the downtown area remains the epicenter of office leasing, accounting for over 4.2 million square feet of available office space. Of that total, only a 6.1% share is available via sublease.

Some of the largest blocks of sublease office space are in the Cool Springs area. It currently has over 2.9 million square feet of available space, 22.1% of which is available for sublease. The area is home to several large sublease listings, including 365,000 square feet in the Carothers Building and 155,000 square feet in the Highwood Office Park.

The Nashville office availability sublease share remains above the national average of 10.9%, underscoring the need for more leasing to improve fundamentals.

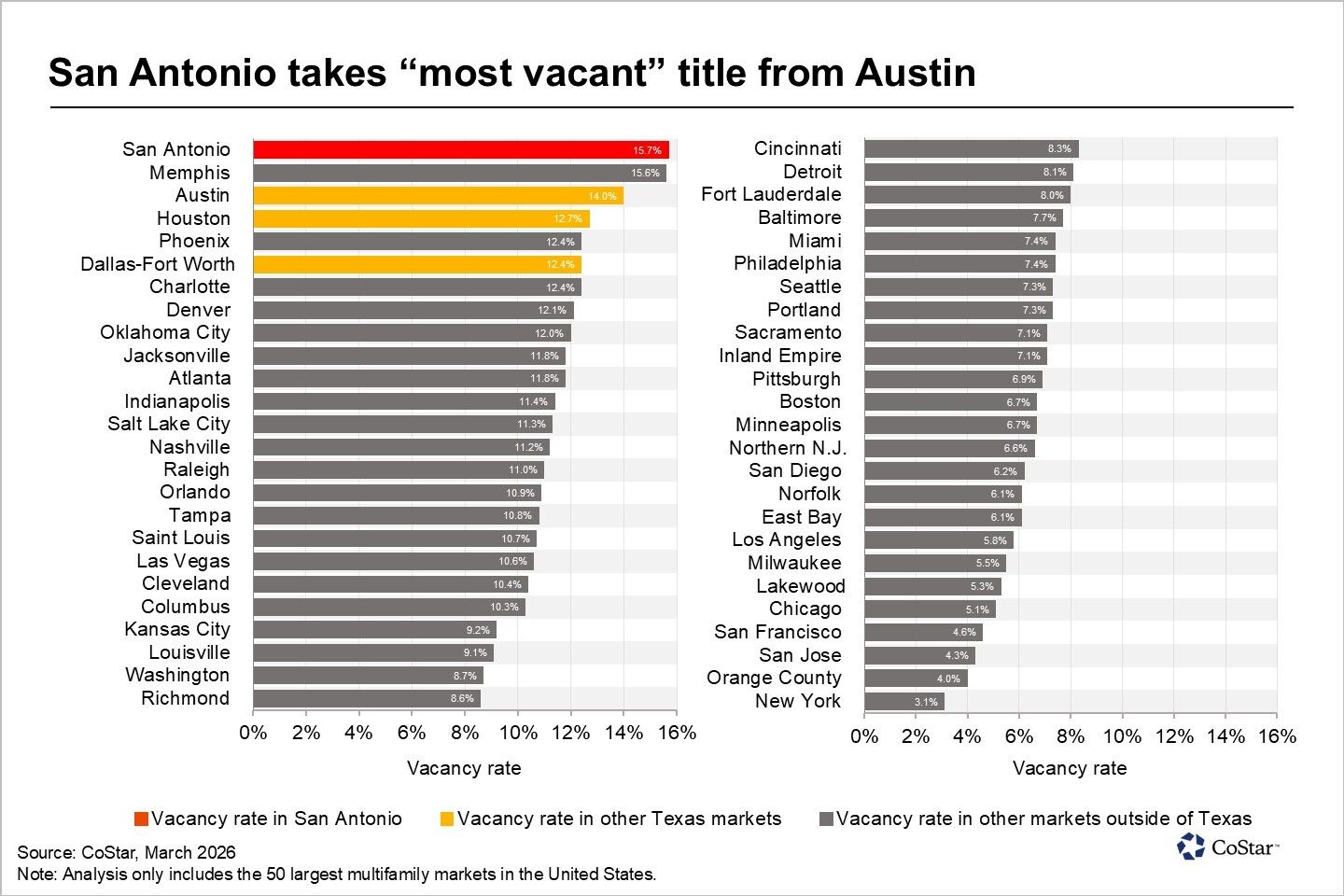

After rising for three-and-a-half years, Austin’s vacancy rate finally began to decline in early 2025, eventually falling below that of Memphis by the summer. Vacancies in San Antonio, on the other hand, kept rising, eventually surpassing Memphis and all other major multifamily markets in the United States this year.

Central Texas is not alone with its stubbornly high vacancy rate. Fellow Texas markets Houston and Dallas-Fort Worth are not far behind, currently with vacancies of 12.7% and 12.4%.

While Texas has been particularly affected, this supply-heavy dynamic has been a common feature of Sun Belt markets for quite some time now. Among the 10 most vacant major multifamily markets in the United States right now, nine are in the Sun Belt.

States such as Arizona, Florida, Oklahoma and North Carolina, as well as Texas, attracted a significant amount of multifamily construction during the immediate post-pandemic years as developers, lenders and investors sought to cater to a surge in population growth in the region.

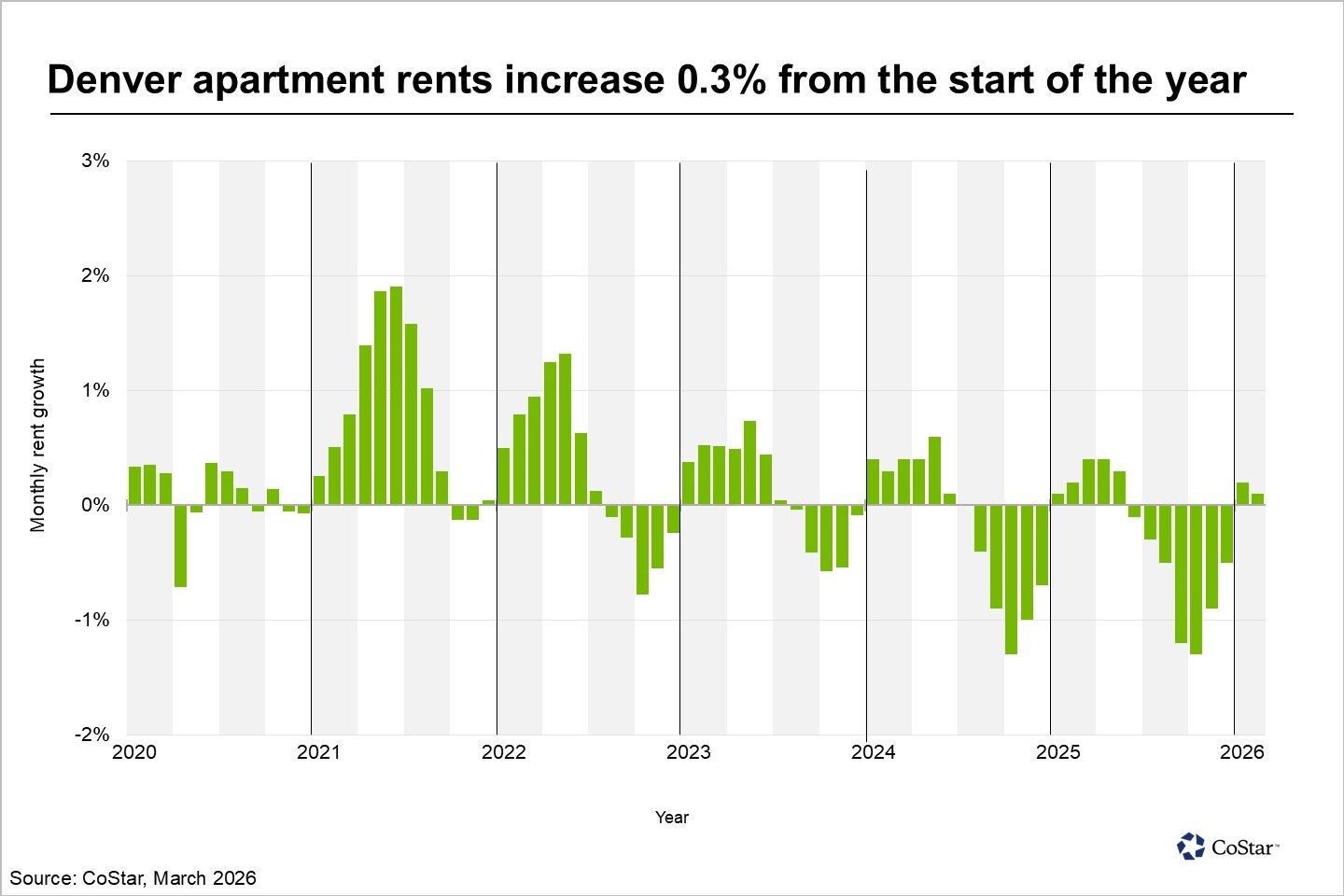

In Denver, apartment concessions are high and landlords are competing for renters. But one out-of-state developer is honing its focus on the region's long-term growth as it kicks off the latest addition to its regional multifamily portfolio.

Carmel Partners, a San Francisco-based investment firm, broke ground on an apartment complex in the city's RiNo district that is set to transform a former industrial site into 480 units of luxury housing. Plans call for a seven- to 14-story building along a full city block at Blake and 34th streets, further extending what has been one of the most active construction pipelines in the country.

The firm acquired the Blake Street site nearly half a decade ago, according to property records, a portfolio deal that stitched together four warehouse parcels totaling about 2.3 acres.

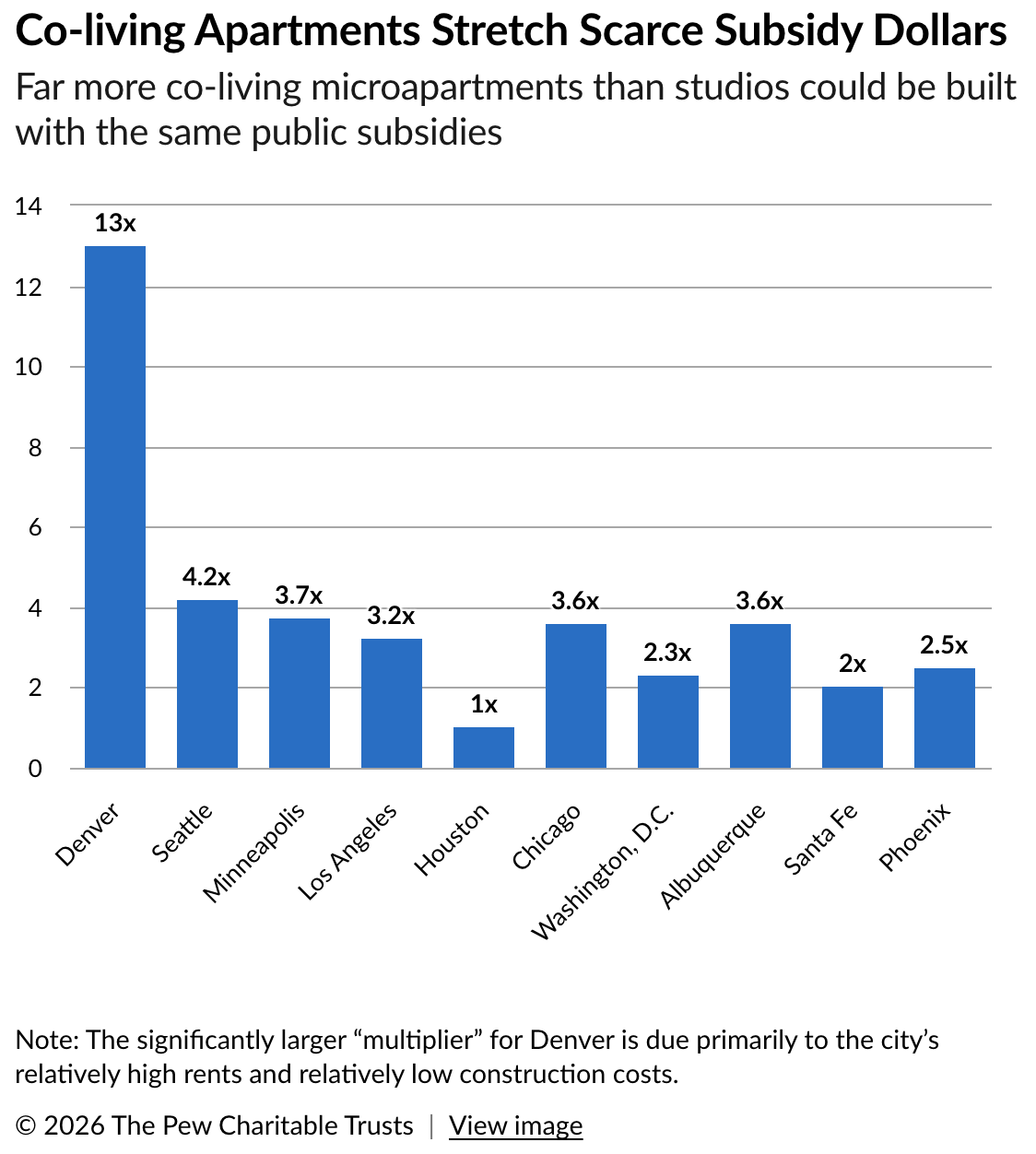

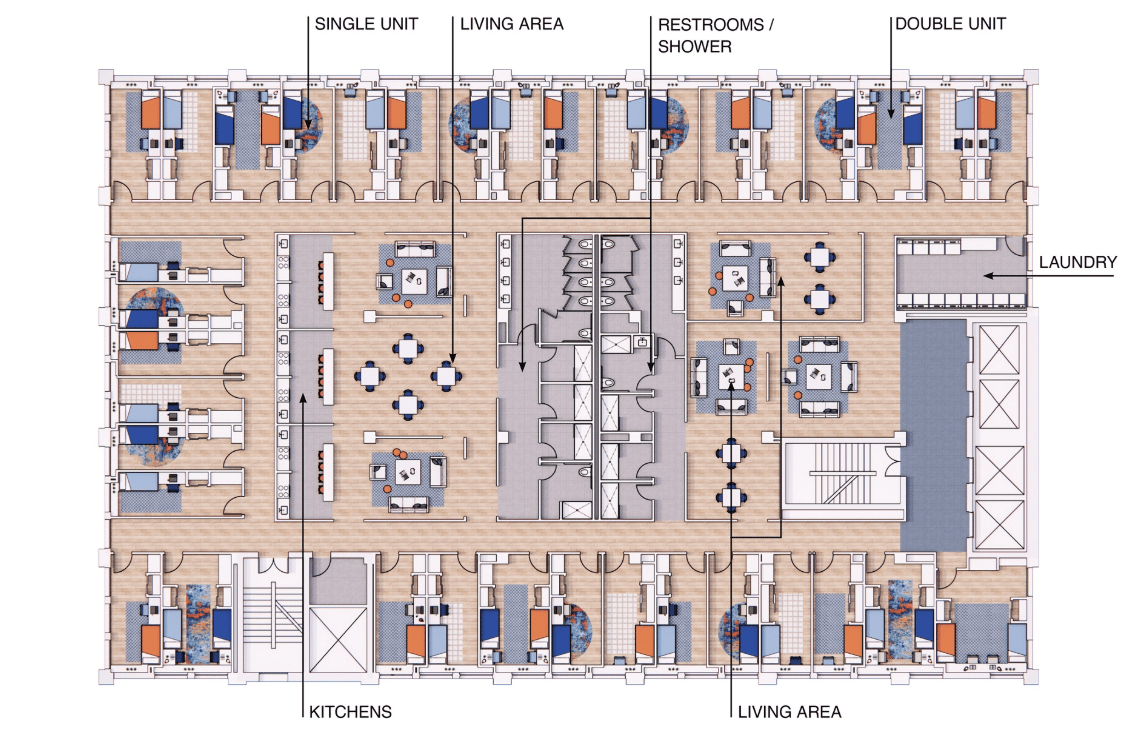

The Pew Charitable Trusts collaborated with Gensler, a global architecture, design, and planning firm, to explore the feasibility of transforming vacant office buildings into co-living microapartments in 10 U.S. cities: Denver; Minneapolis; Seattle; Los Angeles; Houston; Chicago; Washington, D.C.; Albuquerque and Santa Fe, New Mexico; and Phoenix. This emerging model takes its cues from single-room occupancy (SRO) dwellings that once provided flexible, extremely low-cost housing before they were largely zoned out of existence. Research estimates that more than 1 million SRO apartments were destroyed or converted to other uses from 1970 to 1980 alone. Their demise was a major factor in driving up homelessness.

The Gensler design is to locate fully furnished rooms on a building’s perimeter, with windows. It also envisions shared kitchens, bathrooms, and laundry near the building’s core, where an office building’s plumbing already exists.

In the 10 cities studied by the Pew/Gensler team, approximately half of all renter households are considered to be cost-burdened, spending more than 30% of their incomes on rent. In 2024, the Department of Housing and Urban Development reported a record 771,000 people experiencing homelessness in the U.S., an 18% increase from the prior year.

There’s also a mismatch between the housing that is available and what renters need: There is not enough housing near jobs and amenities that is affordable for most workers. Many renters earn less than half the area median income and struggle to find housing in job-rich downtowns where median rents often exceed $2,000 per month. In addition, 40% of renter households nationwide consist of just one person; that figure was closer to 50% in many of the cities studied and reached 56% and 58% in Washington, D.C., and Seattle.

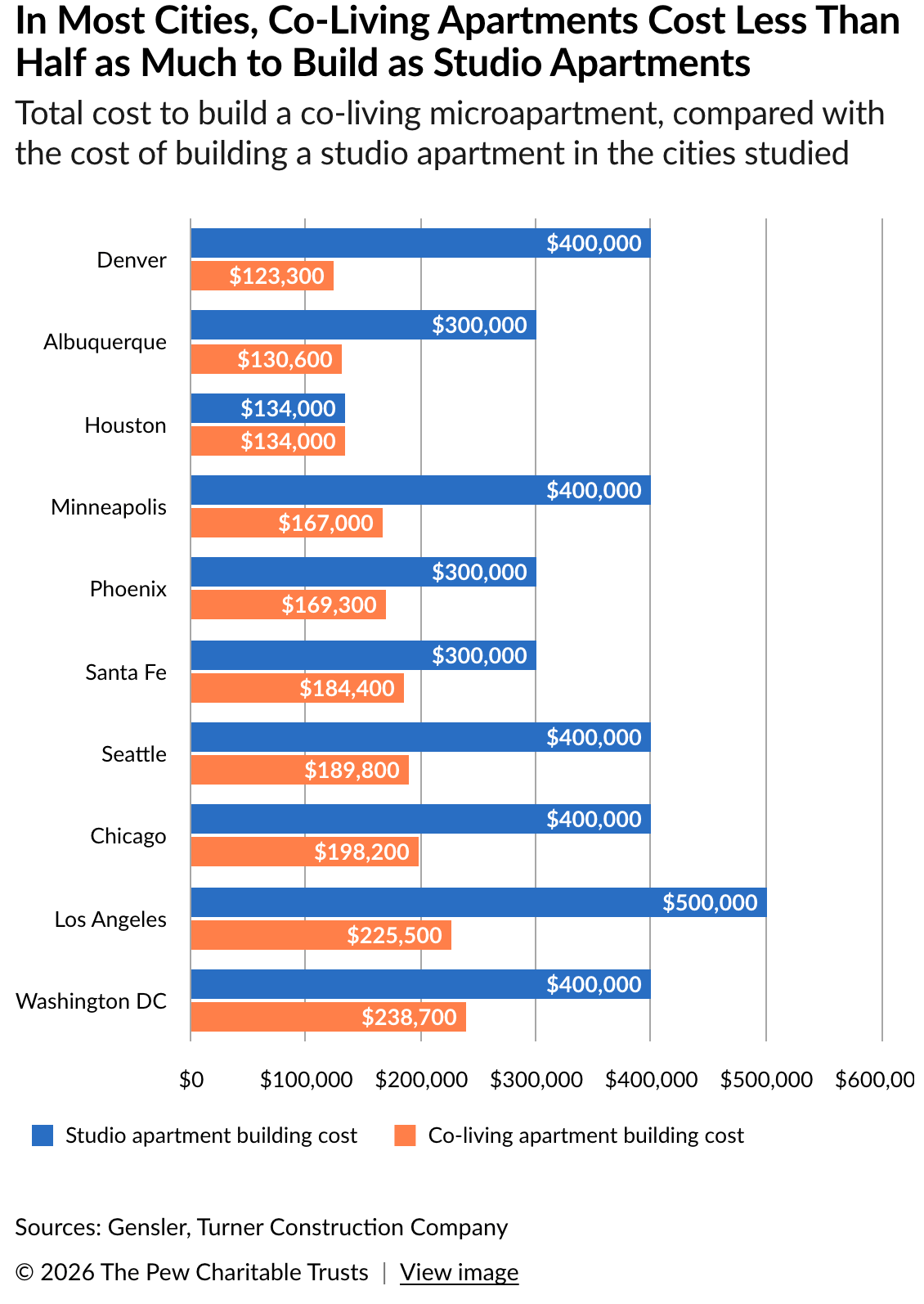

Working with Turner Construction Company, Gensler found that small co-living apartments could be developed for $123,300 to $238,700 each, including acquisition, design, construction, furnishing, and, where needed, seismic retrofitting. In all but one city—Houston—costs ranged from one-third to half the price of developing new traditional studio apartments, which often run $400,000 each in large, high-cost cities.

Financial projections suggest that upfront subsidies ranging from $25,000 to $120,000 per microapartment would be needed to attract private developers. But once the conversion is completed, no ongoing operating subsidies would be required. By contrast, each similarly affordable new studio apartment requires subsidies of $200,000 to $300,000 or more in many cities.

This relatively low subsidy means that every dollar of public investment would produce far more housing with the co-living model than a traditional apartment project. In Phoenix, for example, a $25 million subsidy would produce 294 co-living apartments, compared with only 116 studio apartments—roughly 2.5 times as many homes for the same public investment. In Seattle, the “multiplier” would be 4.2; in Chicago, 3.6.

Across the 10 cities studied, co-living conversions would deliver an average of 3.9 times more affordable homes per dollar of subsidy compared with studio apartments.