- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 031624

This week we are at The National Due Diligence Alliance, an event much more interesting than its title sounds. It’s a meeting of family offices and institutional sources of funding for alternative investments which include real estate. I’ll have summary of what we’ve learned from the money people next week.

I also had a few things to say about the NAR’s settlement of the Sitzer-Burnett case. I found this case quite puzzling from the very beginning. I don’t think the case affects us directly, but it will affect affordability in the existing market. I read the DOJ’s position on the case a few weeks ago and it struck me as written by someone who’s understanding of the residential real estate market was precisely backwards. Although there was much fanfare around cost savings following the settlement, I don’t see anything substantive to indicate that would happen. The major concession is offers for buyer agent compensation are coming out of the MLS, and buyers will need written agreements with their representation. I think the most likely result will be seller commissions are unchanged - there is no factor to motivate selling brokers to reduce their fees - and will cause buyers to pay an increased fee for their own representation, increasing the overall transaction costs 2-3% - another great win for the consumers by our government.

How might this affect the new home market? About 75-80% of sales are typically co-op sales depending on market conditions. It looks like this settlement will reduce the price gap between new and existing homes by a fairly significant amount - if the buyer comes in without representation.

Location Strategy Chartbook

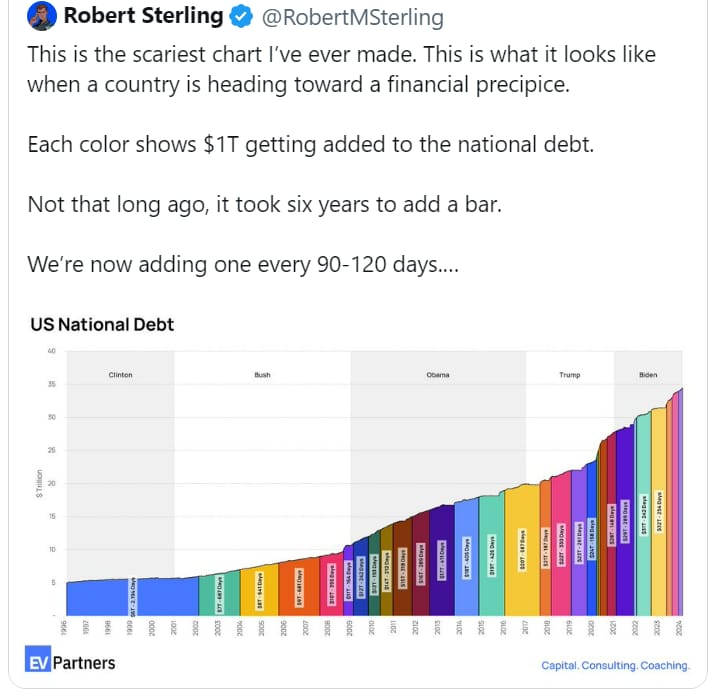

Although we generally try and stay away from political commentary, I feel comfortable in saying the president’s a fundamentally unserious document. The chart below shows the growth of US national debt. Each bar represents $1 Trillion - which now happens every 60-90 days.

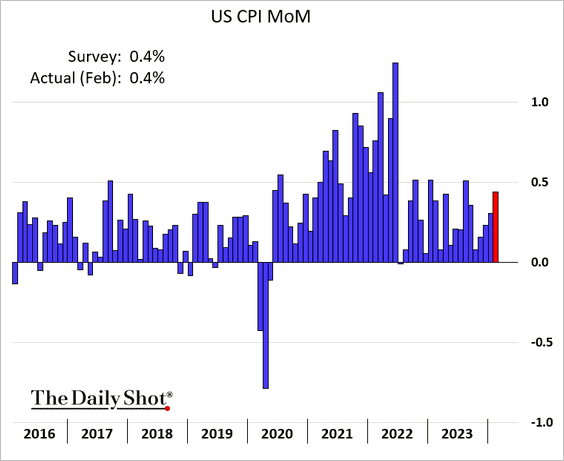

Inflation strengthened in February,…

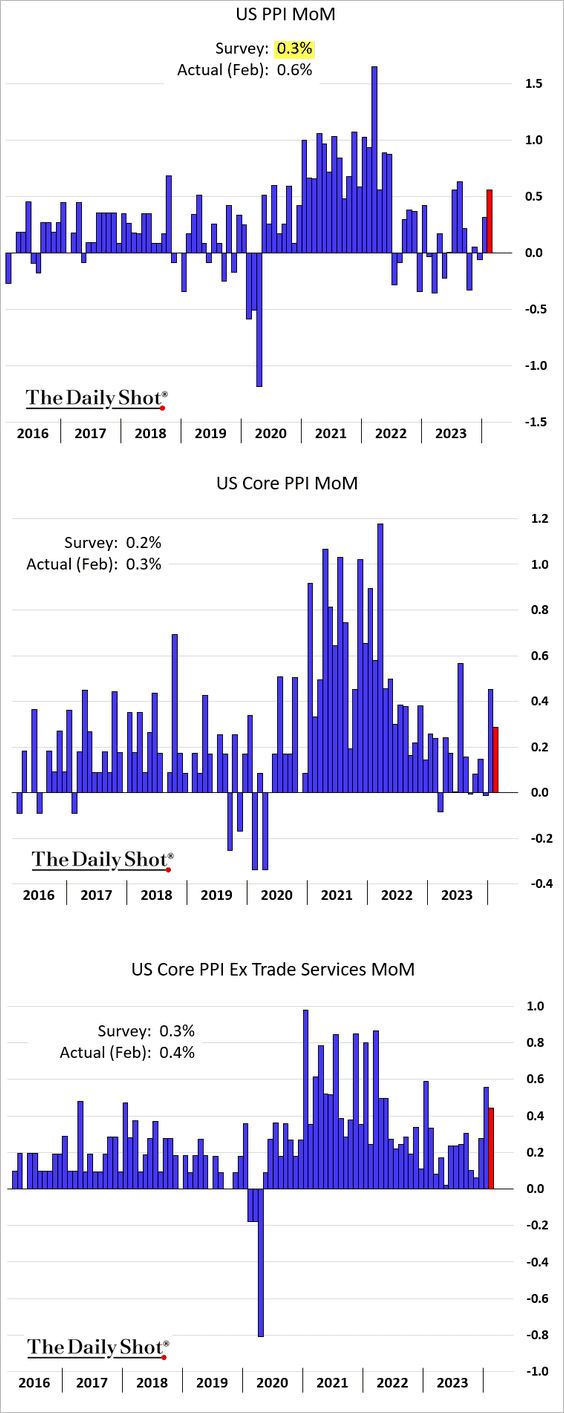

Last month’s producer prices topped expectations, reflecting persistent inflationary pressures. PPI projects CPI increases about nine months out.

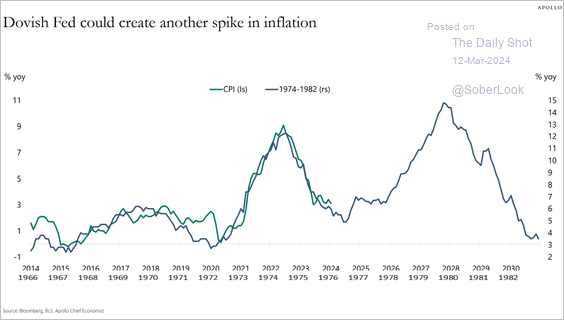

Inflation vs the 1970s: we are not quite ready to make the double-peak call on inflation yet, but it is looking increasingly likely.

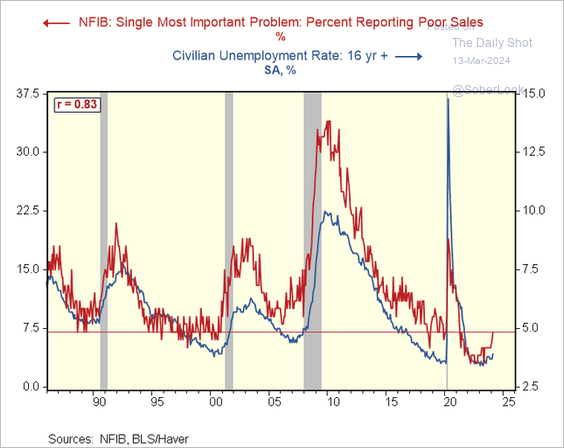

We are standing by our no-recession call, but remind you that we have forecast a slowdown and will feel recession-like. More firms reported “poor sales” as the most important problem, which could indicate higher unemployment ahead.

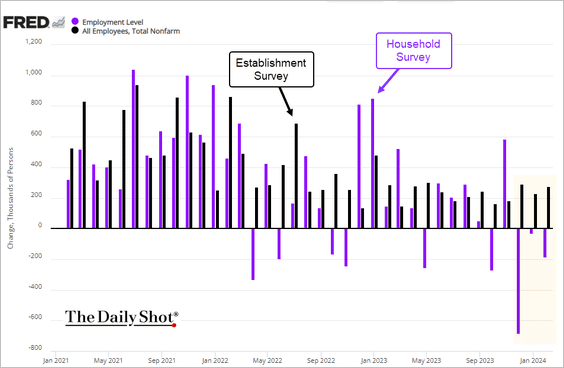

Again we question the job numbers from the “Federal Department of Goal Seeking”: we continue to see a divergency between the Establishment Survey (the official figures above) and the Household Survey

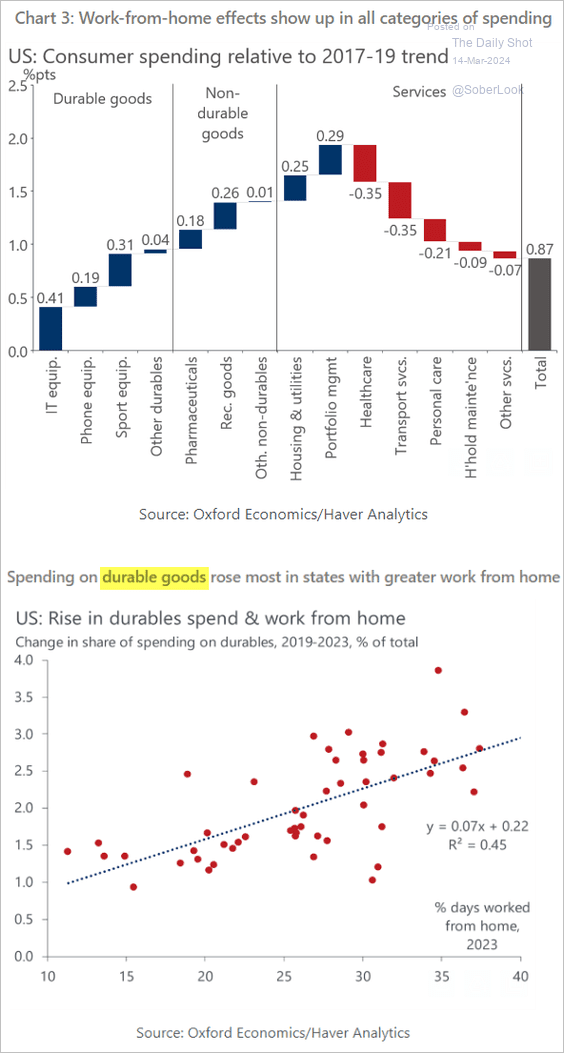

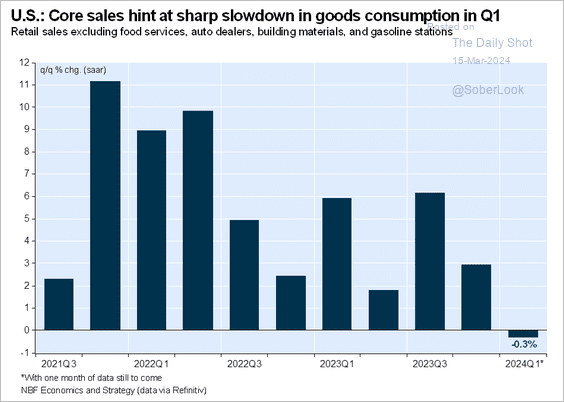

We believe work from home will remain a permanent part of the economy. There simply are not enough workers to give employers leverage to demand full-time return to office. We see work from home still increasing durables spending.

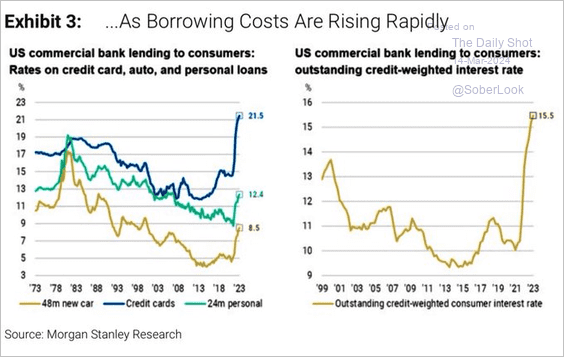

Higher borrowing costs are making their way through the economy.

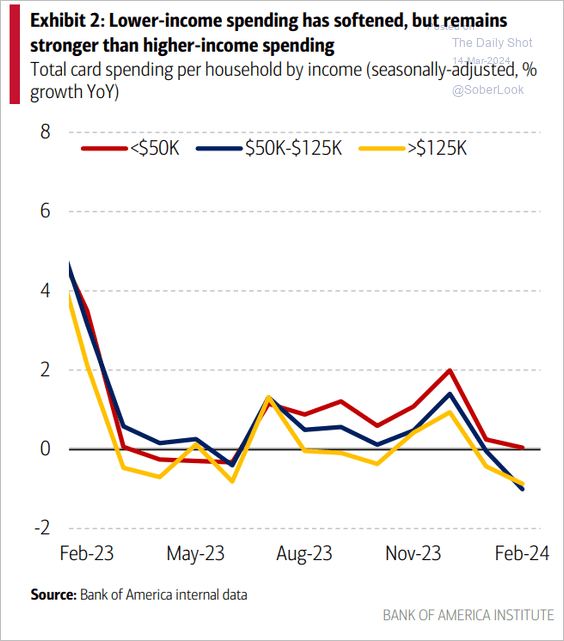

Debit/credit card spending declined in February year-over-year for higher-income households;

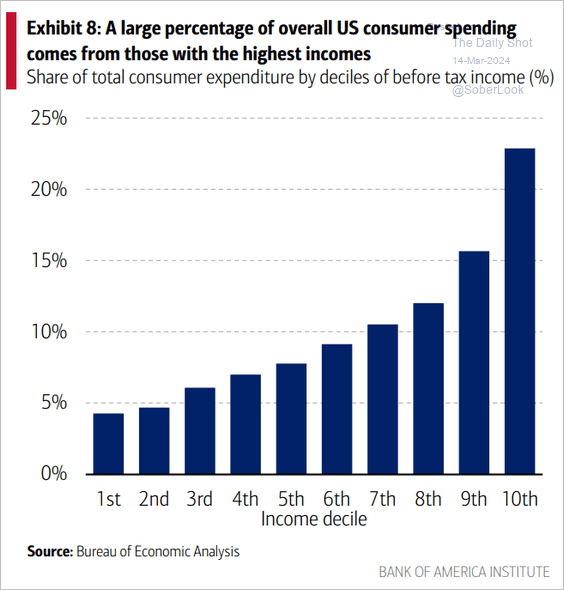

…who drive much of the consumer spending in the US.

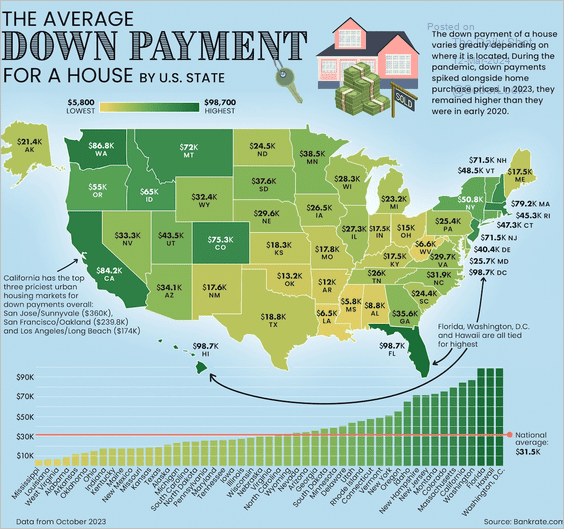

How much are buyers putting down: average down payment by state:

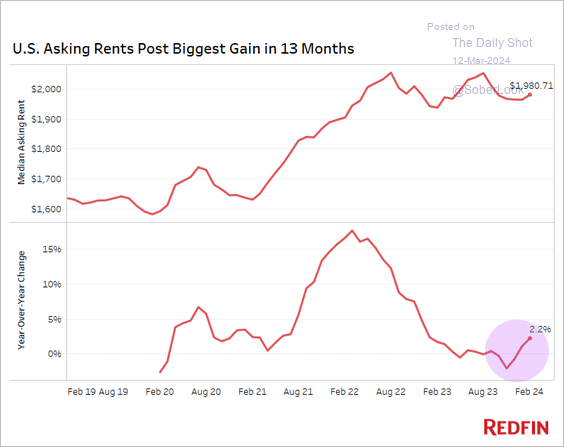

Rental inflation going up again

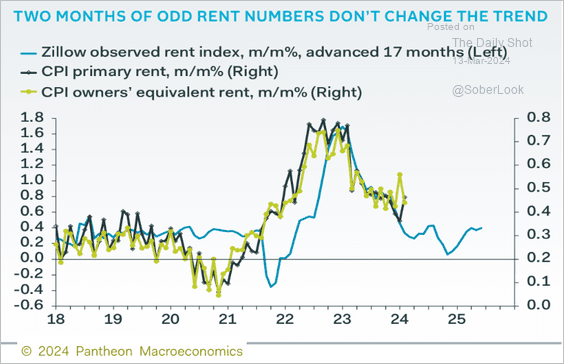

But leading indicators continue to signal softer housing inflation ahead - two months don’t change the trend.

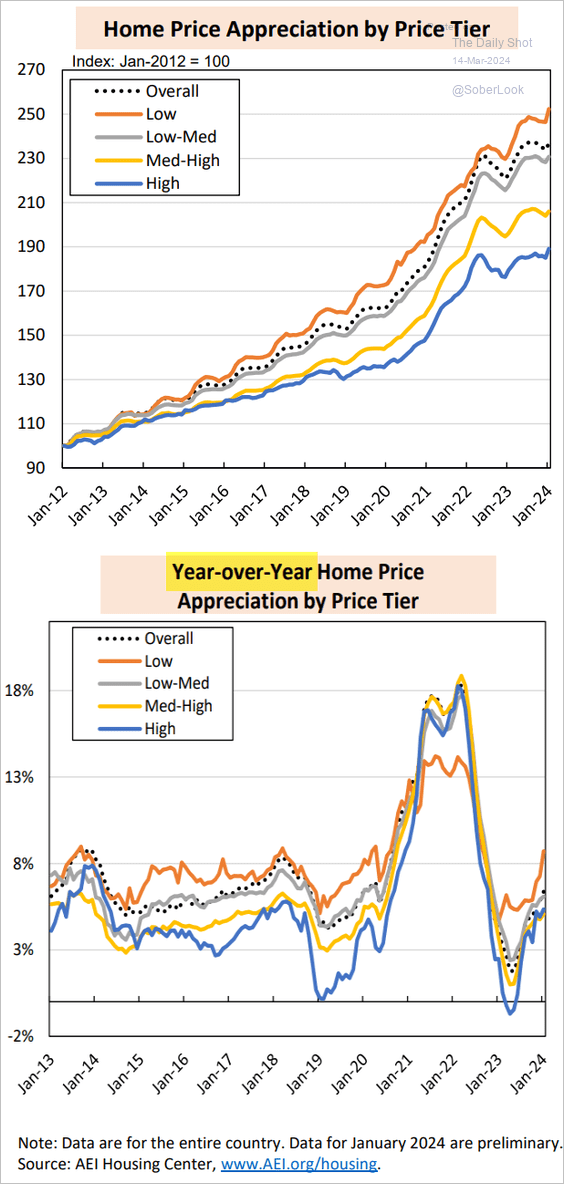

The lowest tier of housing continues to experience the fastest rise in price, and has done so since 2017.

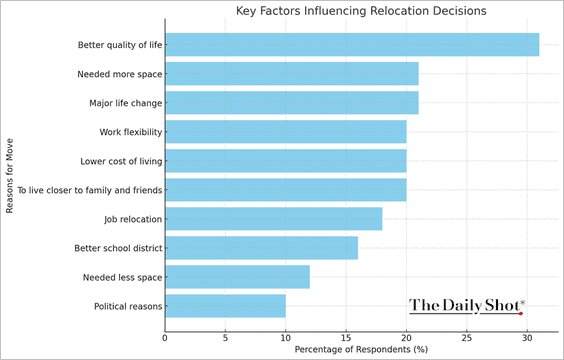

People relocate for better quality of life and more space; they do not relocate for politics.

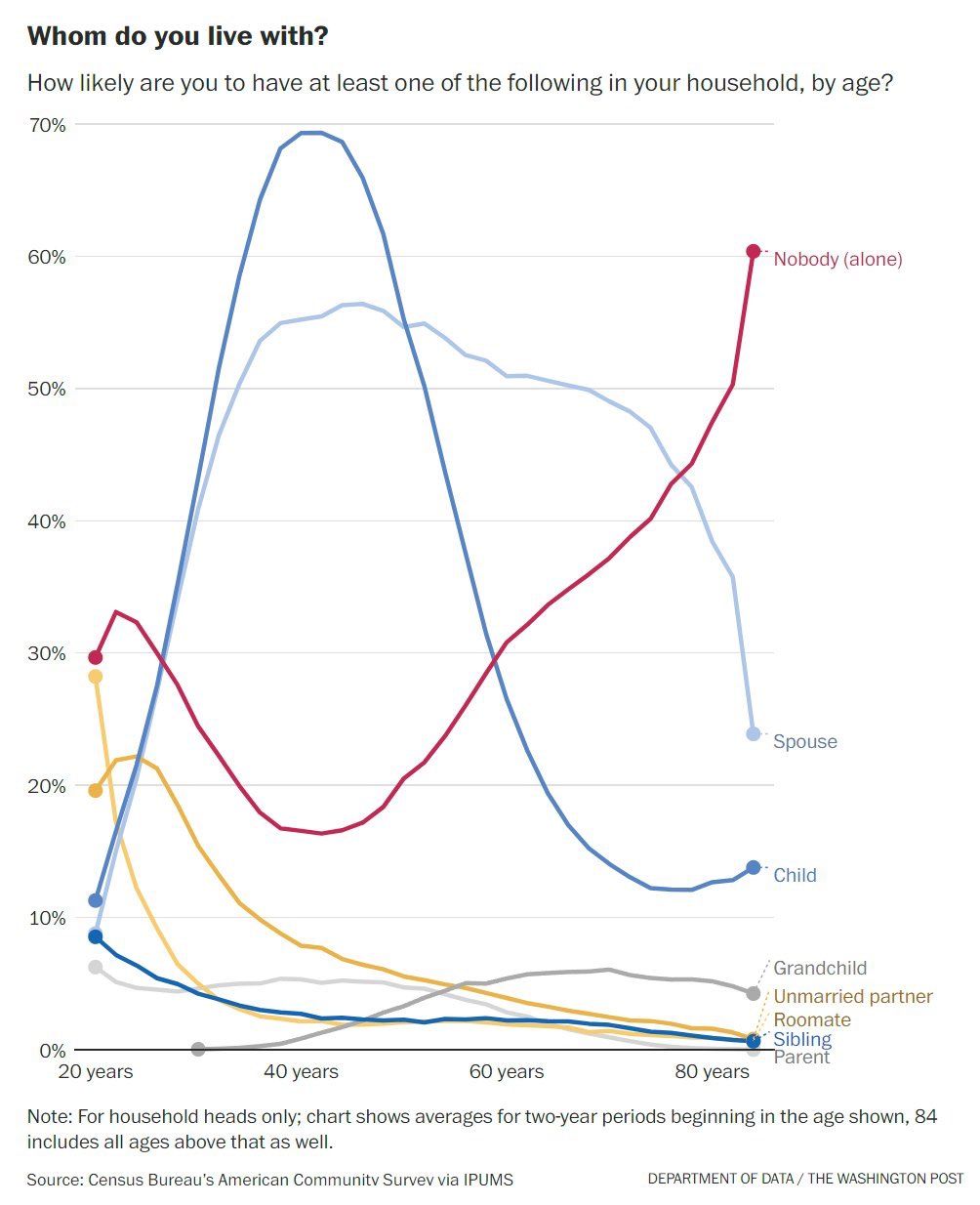

With whom do you live, and when?

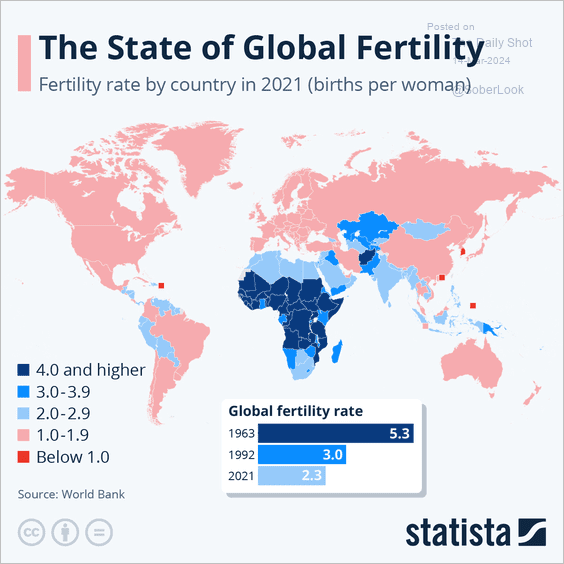

The Future Belongs to Africa and India