- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 032324

Location Strategy Chartbook

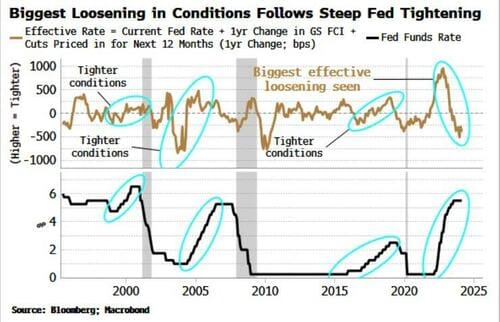

Periods of Fed Funds raises typically occur in conjunction with tightening economi conditions - this time they have taken place with a signficant loosening.

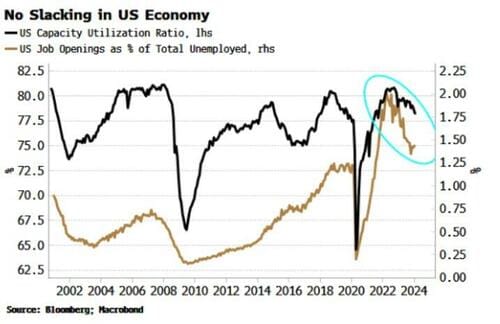

Capacity utilization and job openings have declined, typically indicating tightenening conditions.

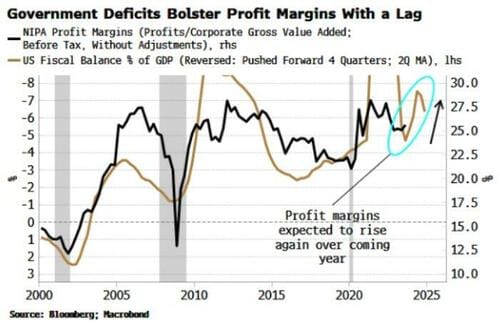

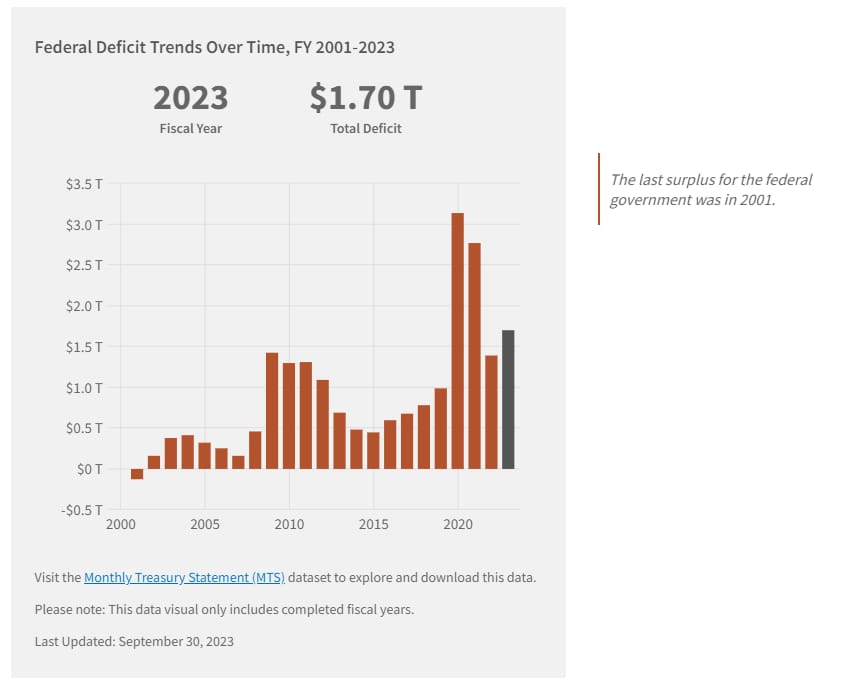

In this cycle, it has been the government’s dissaving that has allowed the corporate sector in aggregate to grow profits and - capitalizing on monopolization and on the unique economic disruption seen in the wake of the pandemic - expand profit margins.

That government “dissaving” came in the form of massive deficit spending under the last two administrations, one of the reasons that we don’t see much difference in the two candidates for president - both favor procyclical inflationary spending.

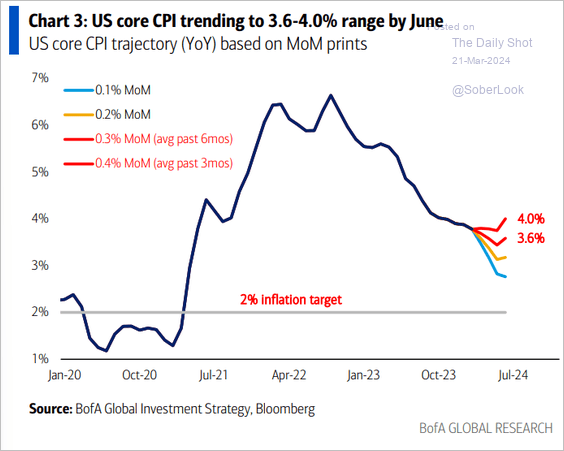

Is there a risk that core inflation could remain persistently above 2%? Given the above charts, we would say yes.

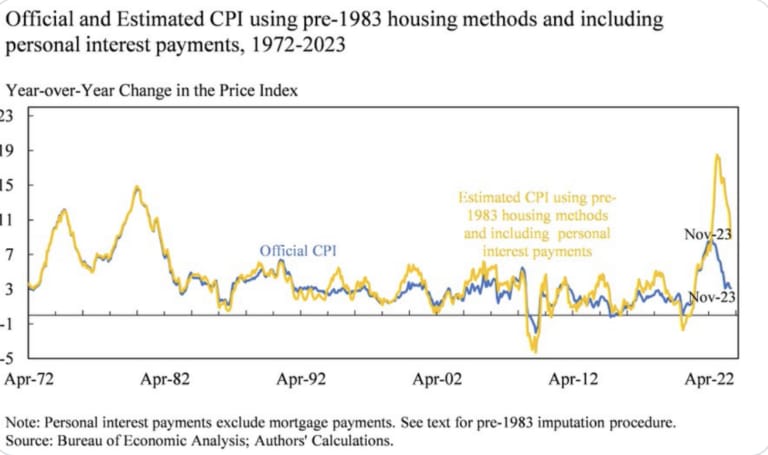

The basket of goods comprising the CPI has changed since the 1970s. If we make an effort to reconstruct the CPI of economist Arthur Okun’s (creator of the Misery Index) era—which would have had inflation peak last year around 18%, we are able to explain 70% of the gap in consumer sentiment we saw last year.

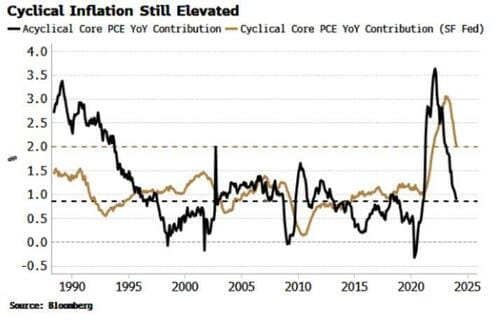

Cyclical Core PCE still elevated

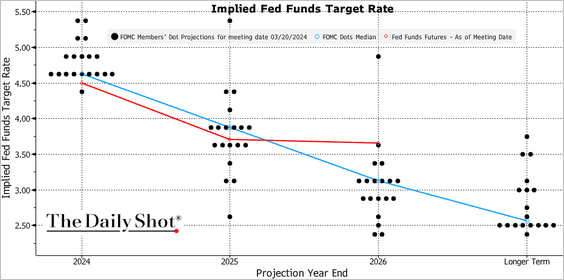

Despite data indicating persistent inflation, the FOMC maintained its projection for three rate cuts this year. The markets interpreted the decision as dovish, sending the S&P 500 and gold to record highs:

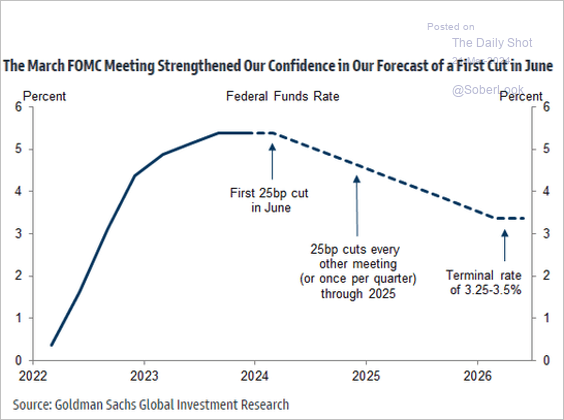

Goldman expects the first rate cut in June (2 charts).

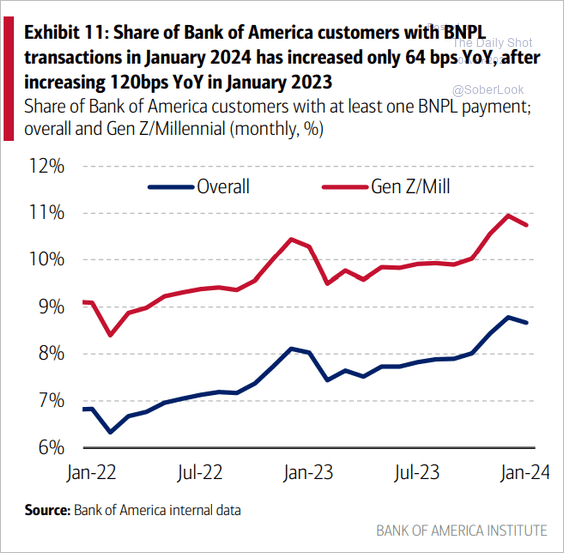

BPNL (buy now, pay later) usage over time:

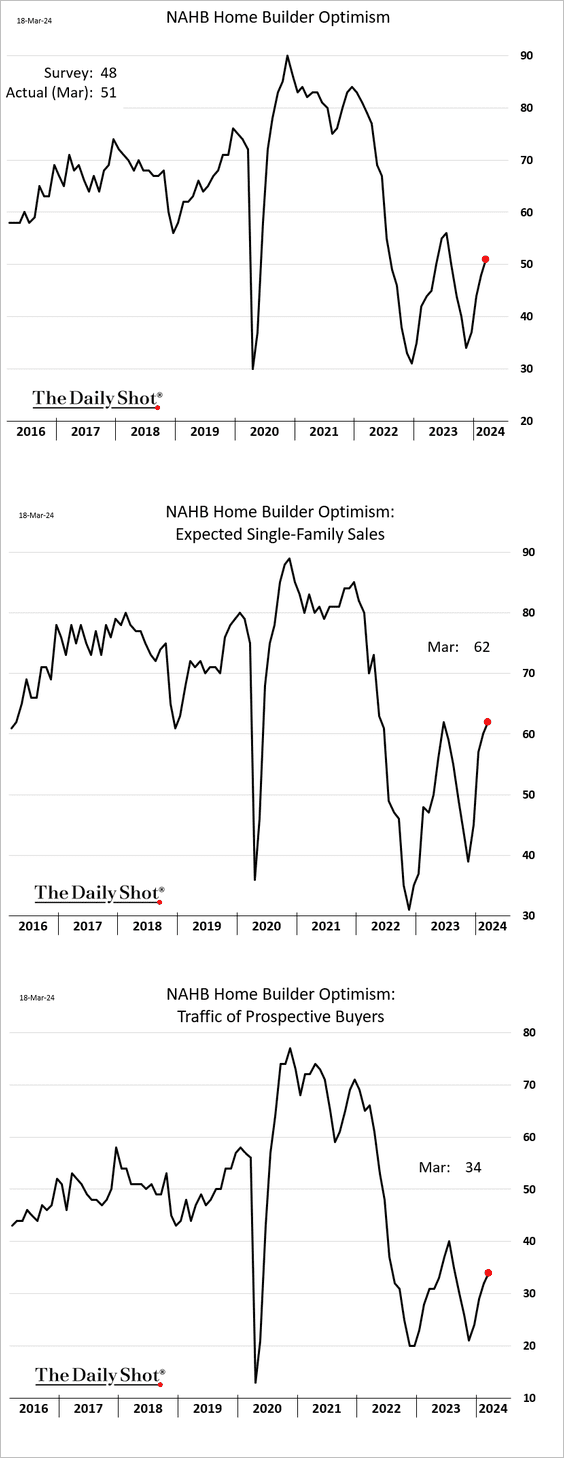

Buyers, optimism and traffic all up

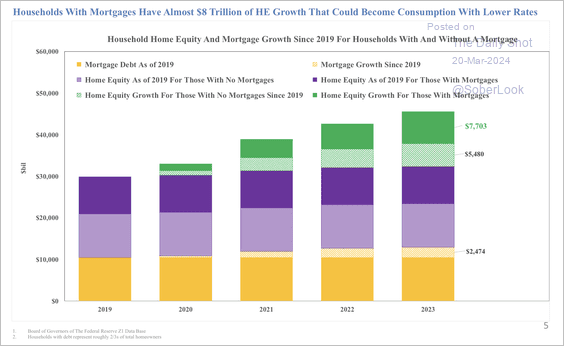

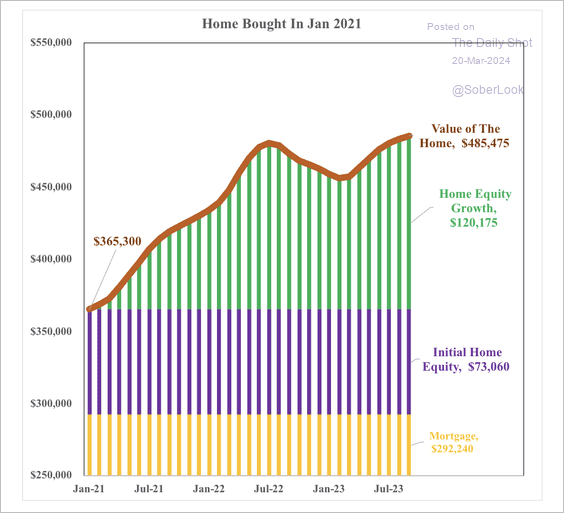

Households with mortgages have experienced a rise in home equity, especially for those who purchased a home in early 2021.

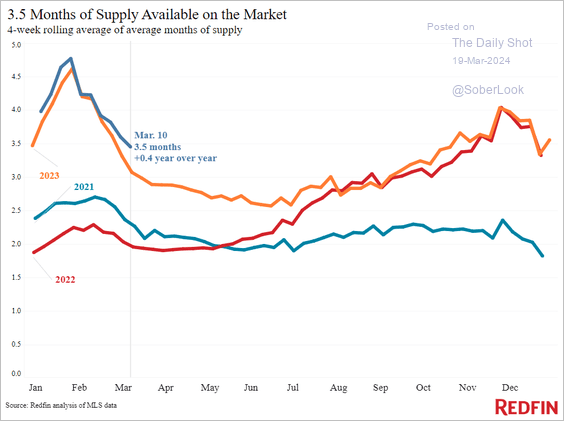

Supply is up

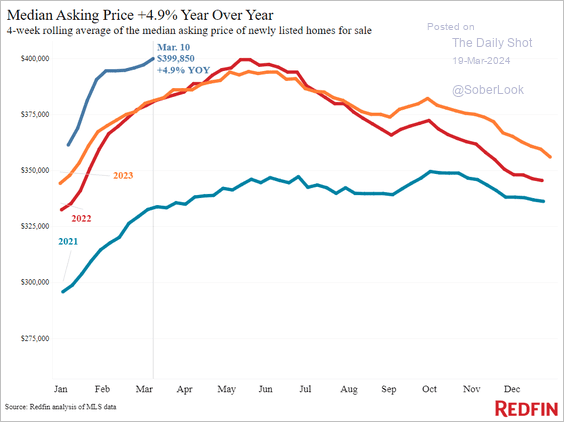

But so are asking prices

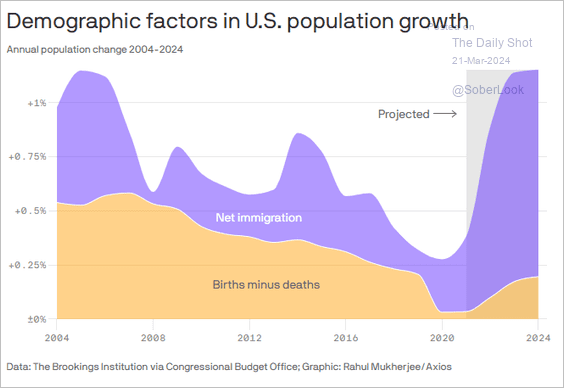

Contributors to US population growth