- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 033024

Some announcements for the quarter. Thanks for your business this year. You may hear from some new faces/voices as we are looking to expand both our local and overseas staff and are trying out some potential candidates. More on that in the coming weeks.

Are you a sponsor or GP on investment projects? Or perhaps an LP investor considering investing in a development? We are proud to announce our new service for you: GreenLight Due Diligence.

Unlike traditional due diligence reporting designed to vet a sponsor or the legal terms of a deal, a GreenLight report evaluates existing and/or proposed assets across four dimensions of feasibility. Make sure your project gets the GreenLight. Contact us for more information, 832.304.3478.

Location Strategy Chartbook

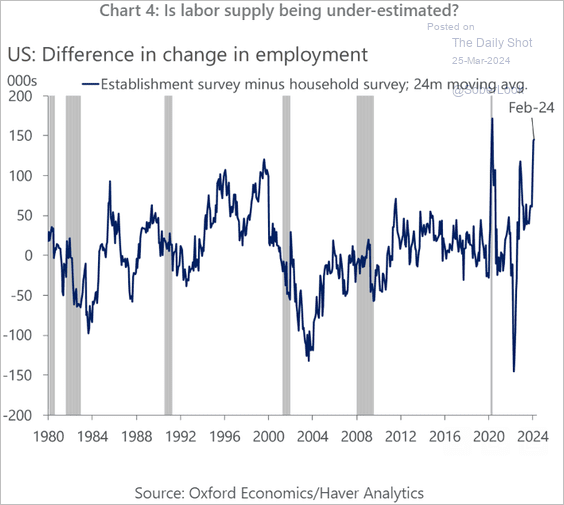

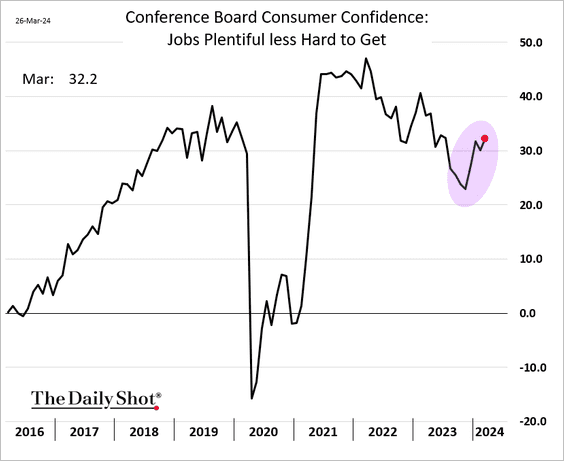

The gap between job growth based on the Household and Establishment surveys has reached extreme levels, raising the question of whether the strength in US job gains might be overstated. Even the Philly Fed has announced the job gains are overstated.

Why we still think the Fed will cut rates this year.

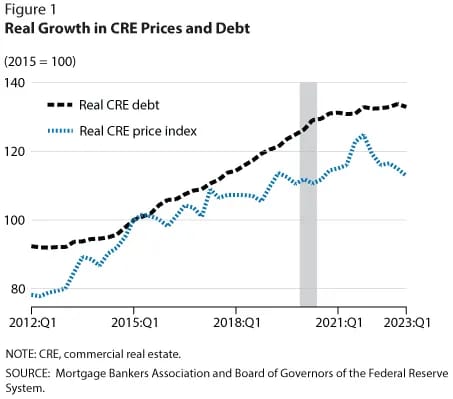

High interest rates have pushed CRE values underwater.

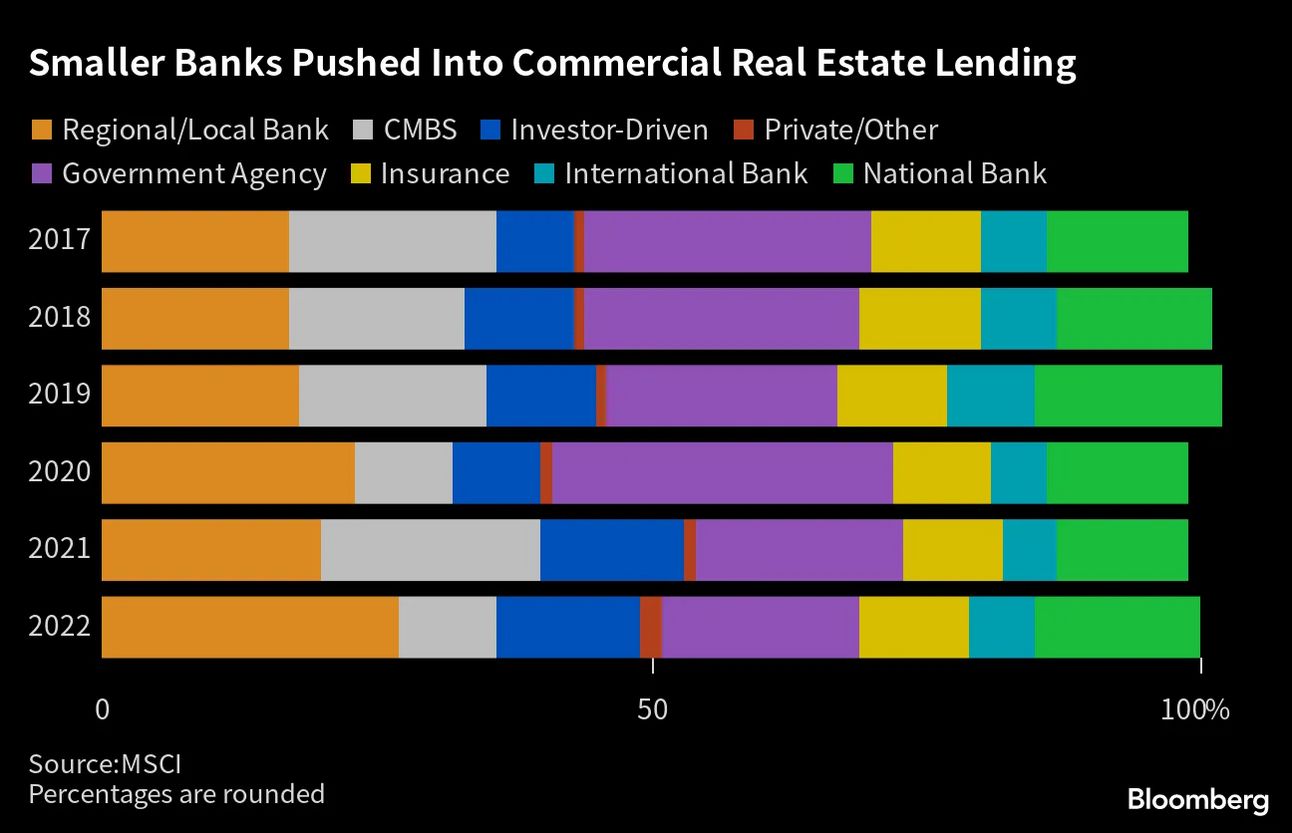

Loans set up through the FDIC with iffy asset valuations saved about 1,600 banks - one third of all banks in the US from failing. There is another almost $1 trillion in CRE loans maturing this year, a 28% increase over last year.

A recent study by the NBER showed 385 banks could fail - mostly small and regional banks who typically hold as much as 1/3 of their portfolio in CRE loans.

The FDIC insures deposits at roughly $0.05/$100, so the FDIC is essentially guaranteeing over $20 trillion in deposits on just over a hundred billion. So we can keep rates high to fight inflation and face tens of billions of losses to come out of general federal revenue with daily announcements of failed banks, all during an election year. Or, the Fed can bring interest rates down relatively slowly.

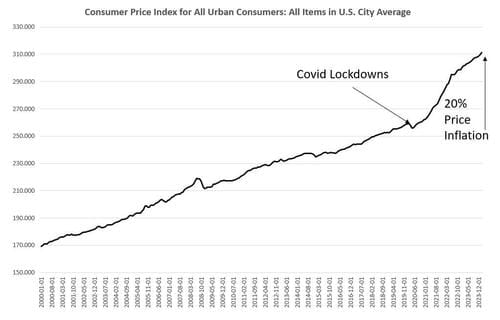

The dollar has lost one-fifth of its value in just four years. This has been devastating for many savers and for those on fixed income.

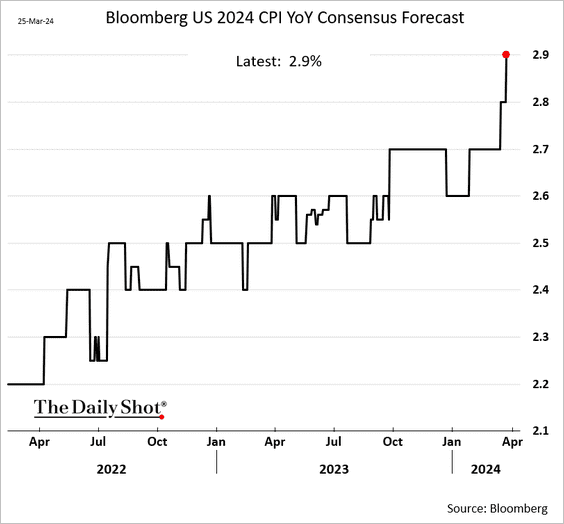

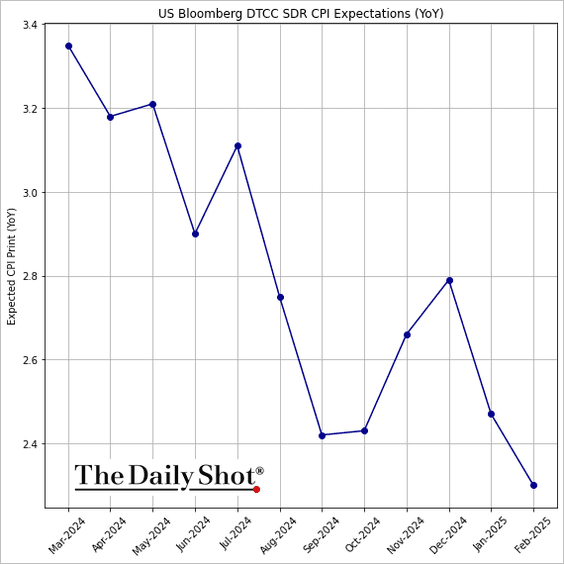

Forecasters have increased their projections for the 2024 year-over-year CPI, partly due to rising energy prices.

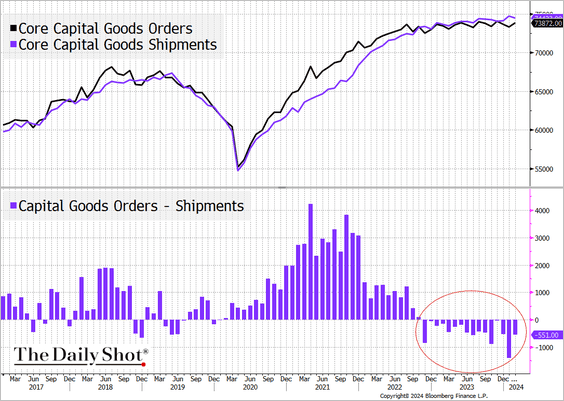

Capital goods shipments exceeding orders indicate potential downside risks for future demand.

The spread between expectations and current conditions remains at recessionary levels.

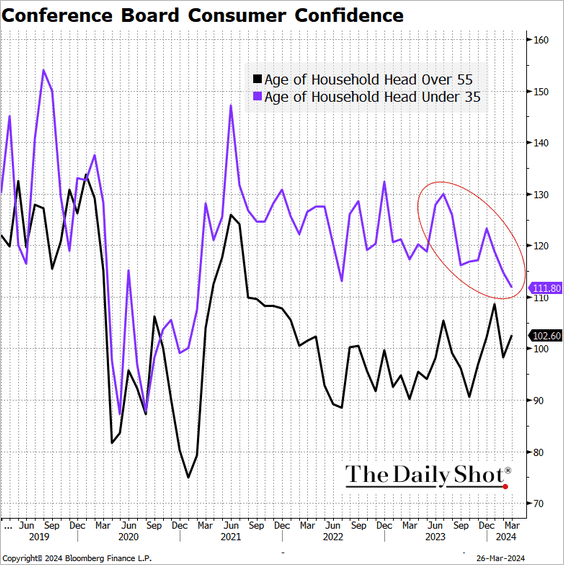

There has been a marked decline in consumer confidence among younger Americans.

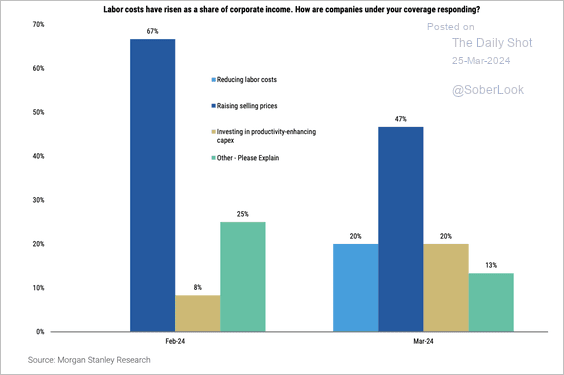

Firms are raising their selling prices to offset higher labor costs, according to an analyst survey by Morgan Stanley, …

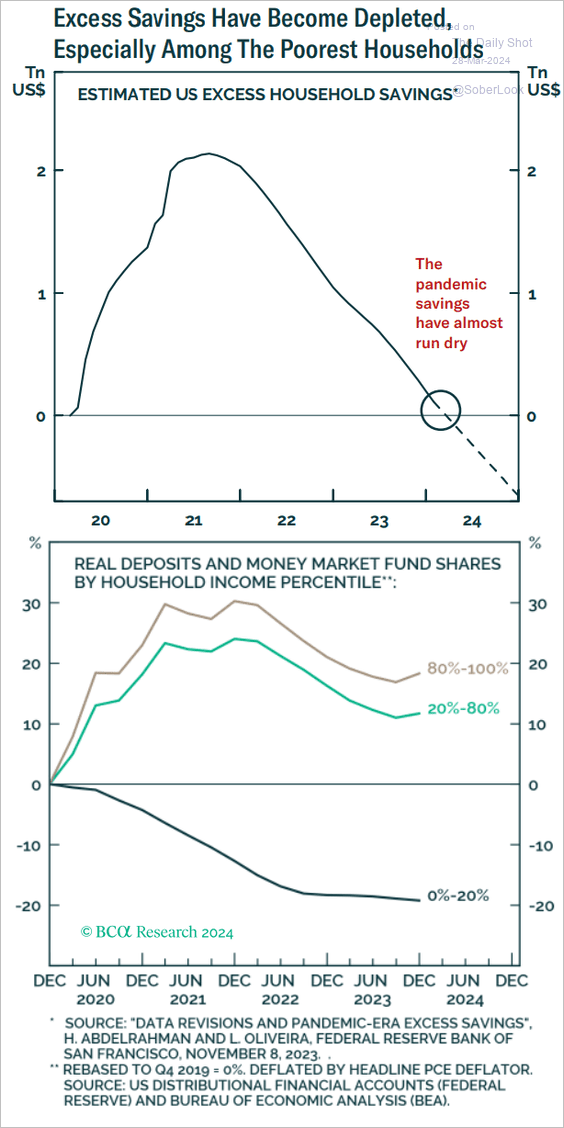

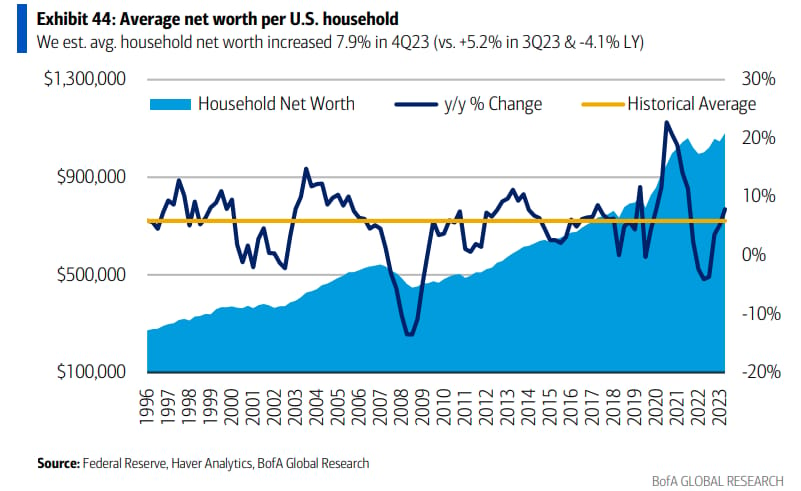

Are households’ excess savings running out?

We est. avg. household net worth increased 7.9% in 4Q23 (vs. +5.2% in 3Q23 & -4.1% LY).

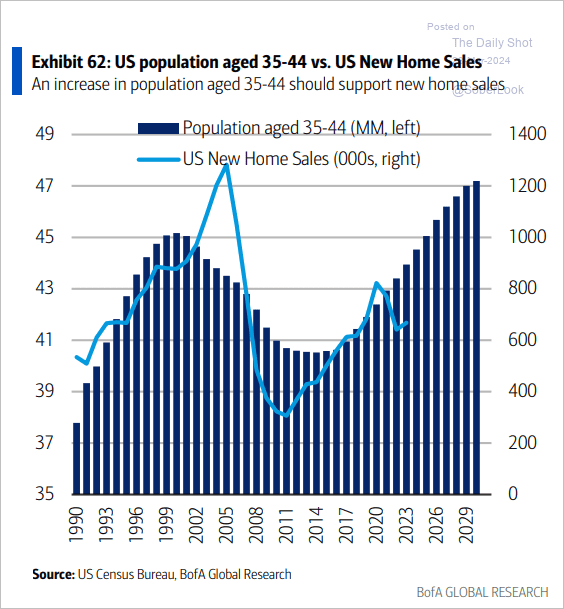

Demographic trends are favorable for stronger new home sales in the coming years.

Home price appreciation slowed in January.

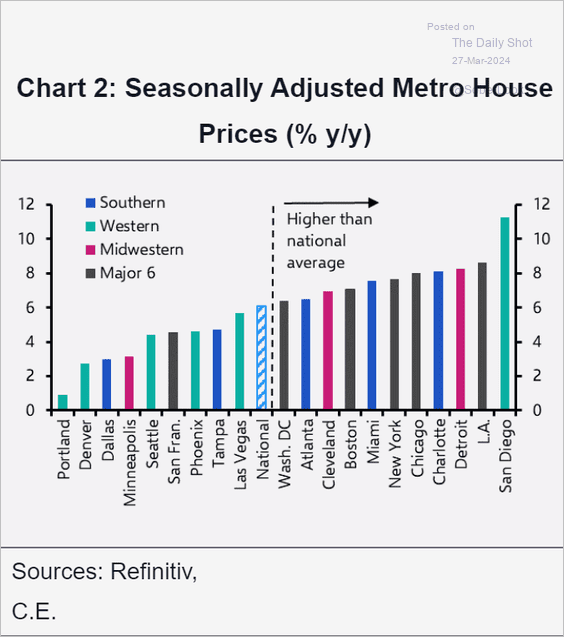

House price gains by metro area:

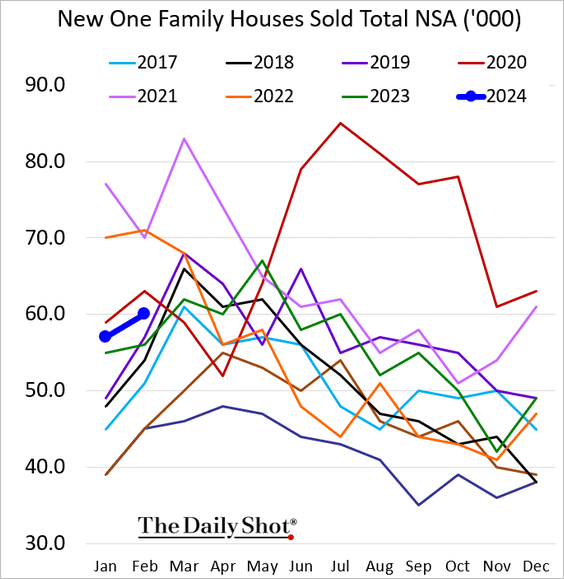

New home sales in February surpassed last year’s levels but fell short of forecasts.

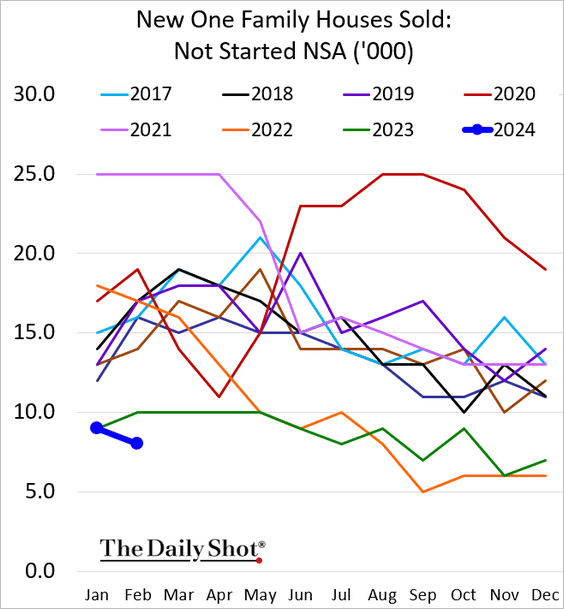

Buyers are showing less interest in purchasing homes that have yet to be constructed.

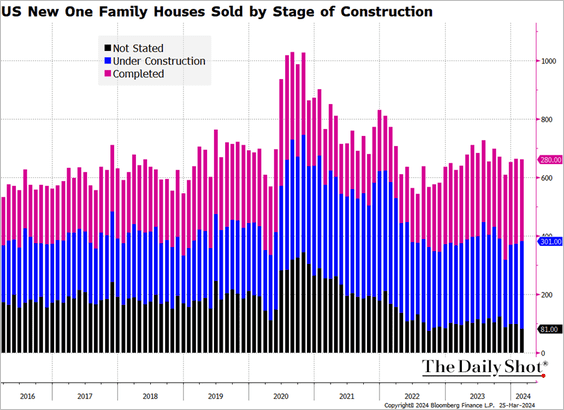

The share of new homes in total housing inventories has been increasing.

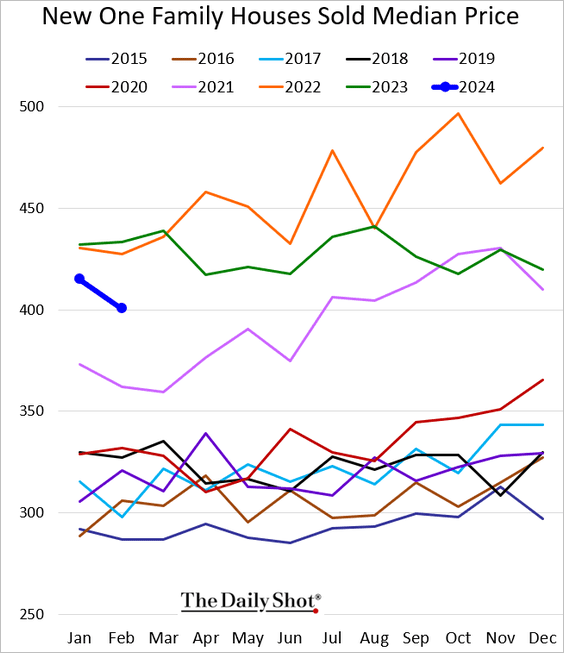

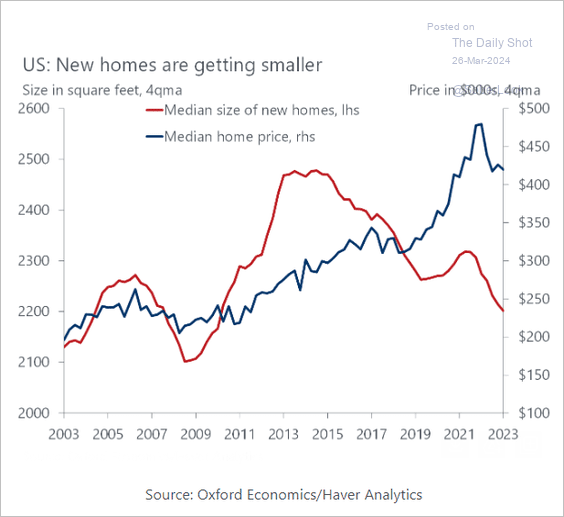

The median price of new homes sold is well below last year’s levels, as builders focus on smaller homes.

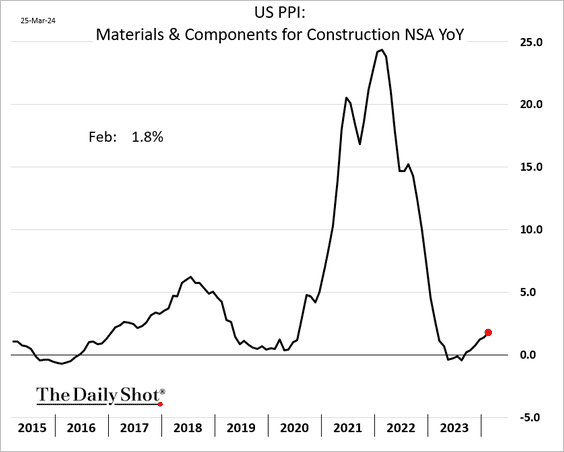

Separately, price increases for wholesale construction materials are beginning to accelerate again.

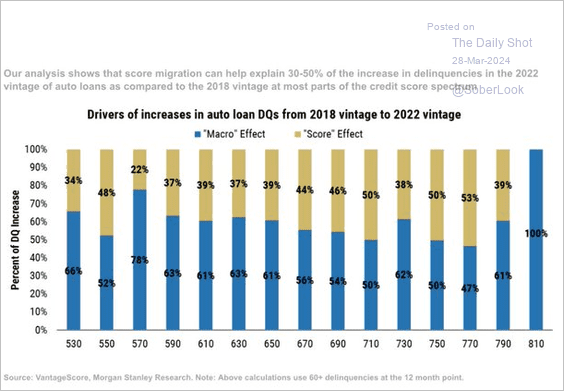

Due to upward credit score migration in recent years, individuals who previously may not have qualified for an auto loan are now obtaining one. This shift has weakened the borrower pool, leading to an increase in delinquencies

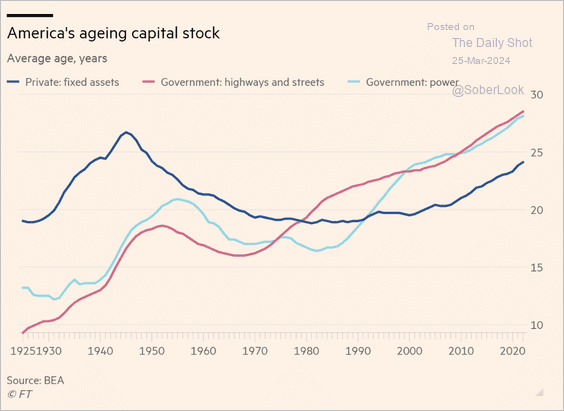

This chart illustrates that substantial investment will be required to rejuvenate the nation’s aging infrastructure.