- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 07.12.25

Location Strategy Chartbook 07.12.25

Real Estate Market Insights

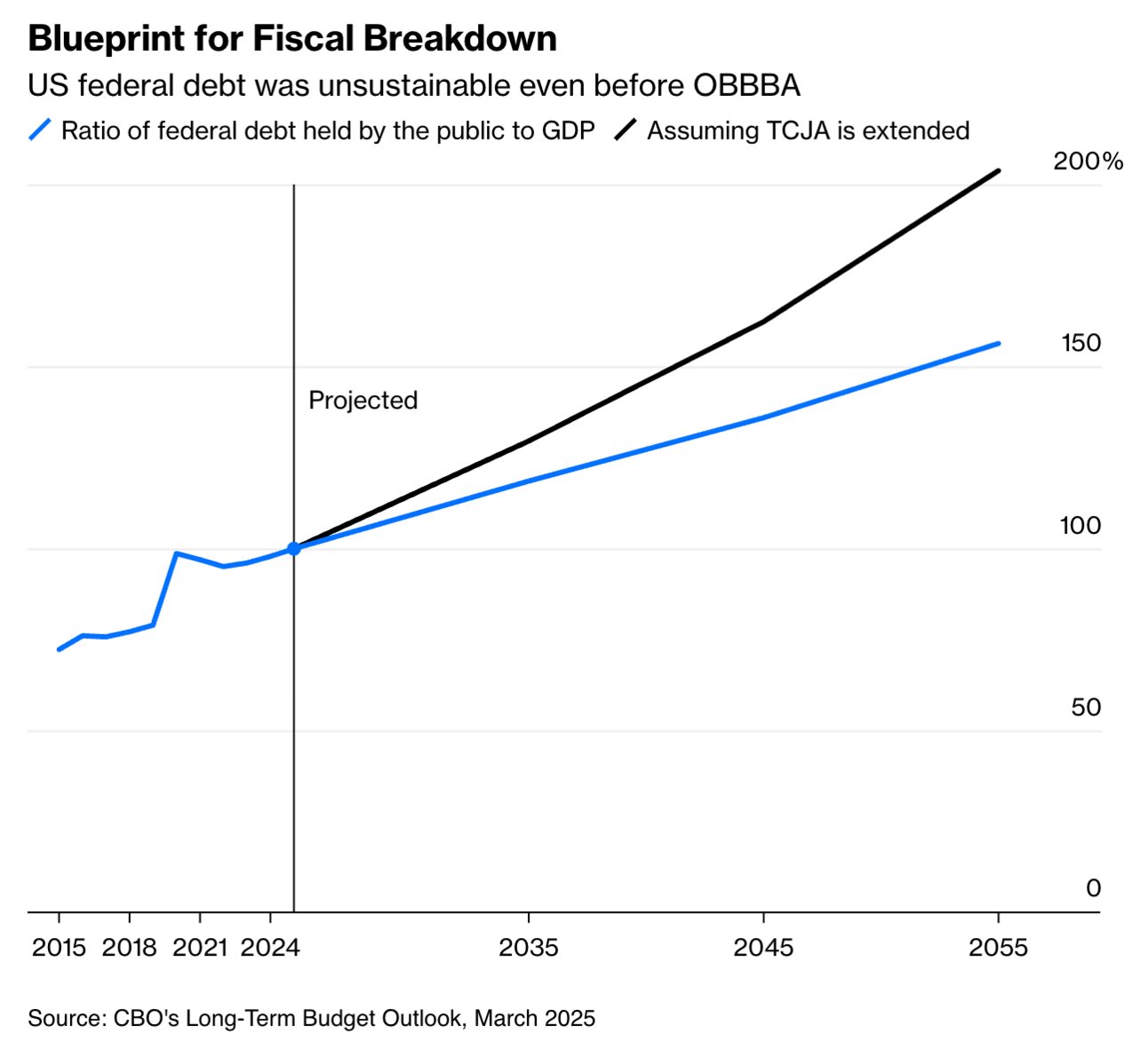

Donald Trump’s $3.3 trillion bill passed the Senate last week. The unprecedented slashing of Medicaid will help fund more than $3 trillion in new tax cuts, meant to replace expiring cuts passed by Republicans in 2017. The majority of those renewed cuts will go to America’s richest. Passage of the full package, which now goes back to the House, also likely means that over the next decade the US will surpass $40 trillion in national debt.

The Senate’s version of the bill will cost the bottom 20% of taxpayers an average of $560 a year while giving an average boost of $6,055 to those at the top end, according to an analysis from Yale University’s Budget Lab. The legislation also provides hundreds of billions of dollars in new funding for defense and for Trump’s crackdown on immigrants both legal and undocumented.

Bloomberg: On plausible assumptions, the final version will add more than $5 trillion to deficits over the next 10 years, moving the track of public debt from unsustainable to all but unhinged. As Congress turns to its budget for next year, it must grapple realistically with this looming crisis.

As written, the measure will add about $3 trillion to the expected 10-year deficit. Include interest payments, and the cost rises to nearly $4 trillion. Assume that assorted “temporary” measures are made permanent — which seems reasonable, given that most of the bill’s cost comes from extending supposedly temporary tax cuts passed in 2017 — and the total could be as much as $6 trillion. Federal debt held by the public would climb from 100% of gross domestic product today to 130% by 2034. (After that, it just keeps going up.)

Complicating the task going forward, many of the bill’s provisions were designed to obfuscate its true costs. Temporary tax and spending changes were timed so that the biggest deficit increases were piled into the early part of the decade. (First, the pleasure of lower taxes and higher spending; later, in theory, the pain of higher taxes and lower spending.) For accounting purposes, the bill’s supporters went as far as to claim that it actually reduces projected deficits — relative to a new “current policy” baseline. In effect, this declared the bill’s centerpiece, extending the 2017 Tax Cuts and Jobs Act at a cost of more than $3 trillion, to be a fiscal nonevent.

WSJ: Americans are enjoying what would have been a record-long expansion before World War Two. The previous one, ended by Covid-19, was the longest ever. Jim Reid, who heads macroeconomic research at Deutsche Bank, points out that five of the top seven were in the past 43 years.

That isn’t a coincidence. Governments and central banks have been willing and able to boost a sagging economy since inflation has been tamed and globalization took off. And all those panics were before the Federal Reserve or deposit insurance existed. Back then governments didn’t even engage in automatic countercyclical spending like unemployment insurance.

Reid wonders if stimulus might flow as freely the next time the economy needs it, though. Federal borrowing has mushroomed and shows no sign of slowing with tax cuts just signed into law. That has spooked the Treasury market on a few occasions recently.

Even if plenty of cash is forthcoming from Washington the next time the economy swoons, what if it results in higher bond yields? They normally fall when a recession hits, cushioning retirement portfolios and lowering the costs of mortgages and corporate loans.

The Fed might not come to the rescue as readily either, says Reid. If inflation is higher because of protectionism and demographic challenges, central banks could be cautious about cutting rates.

And then there’s a danger that really might be an indirect result of such a long period of smooth sailing. While expansions don’t die of old age, former Fed Chair Ben Bernanke once joked they can “get murdered.”

Overconfidence makes policy mistakes like keeping interest rates too high or entering into a trade war more likely.

And, as we saw with the tech and housing busts, confidence also encourages excesses to build up as investors project growth to infinity. Valuations get silly and credit too loose, making downturns more painful.

With stocks so expensive and credit spreads so tight, maybe it’s healthy for investors to be a bit worried.

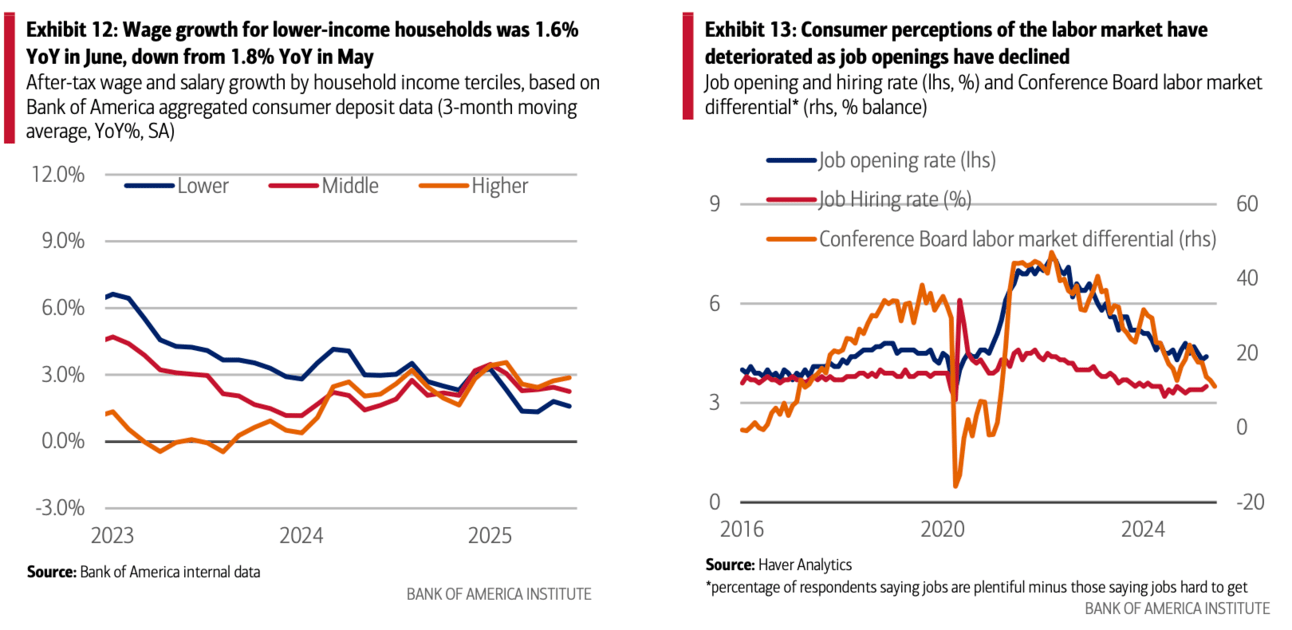

Employers added 147,000 new jobs in June, according to the Bureau of Labor Statistics’ much-watched monthly employment situation report released last week. The unemployment rate ticked down to 4.1%, its lowest level since February.

The report’s headline numbers beat analysts' expectations considerably and were even more surprising following the release of ADP’s report the day before, which estimated a loss of 33,000 private-sector jobs. That was the third-consecutive month in which the government reported substantially higher job gains than the smaller-sample, private-sector-focused ADP report.

The discrepancy is partially explained by the continued outsized contribution of government and adjacent job sectors, such as health care and education. Combined, those sectors accounted for over 80% of job growth in June and more than 68% of jobs added over the past year.

However, in June’s reporting, seasonal adjustments added more than 63,200 education jobs in the state and local government sector, which is unusual and could reflect shifts in the academic calendar beyond the data collection period of the jobs report, which was the week of June 12.

New unemployment claims declined last week (as expected on July 4th holiday week).

The real story is continuing claims, which hit the highest level since November 2021.

It’s difficult to find a new job right now. Young people are struggling to land their first jobs and anyone who has been laid off is having a hard time. The labor market is frozen outside of healthcare, education and law enforcement jobs.

Credit and debit card spending per household increased 0.2% year-over-year (YoY) in June, compared to 0.8% YoY in May, according to Bank of America aggregated card data.

Seasonally adjusted (SA) spending per household rose 0.3% month-over- month (MoM) in June, but that only partially unwound the MoM declines of 0.2% and 0.7% in April and May.

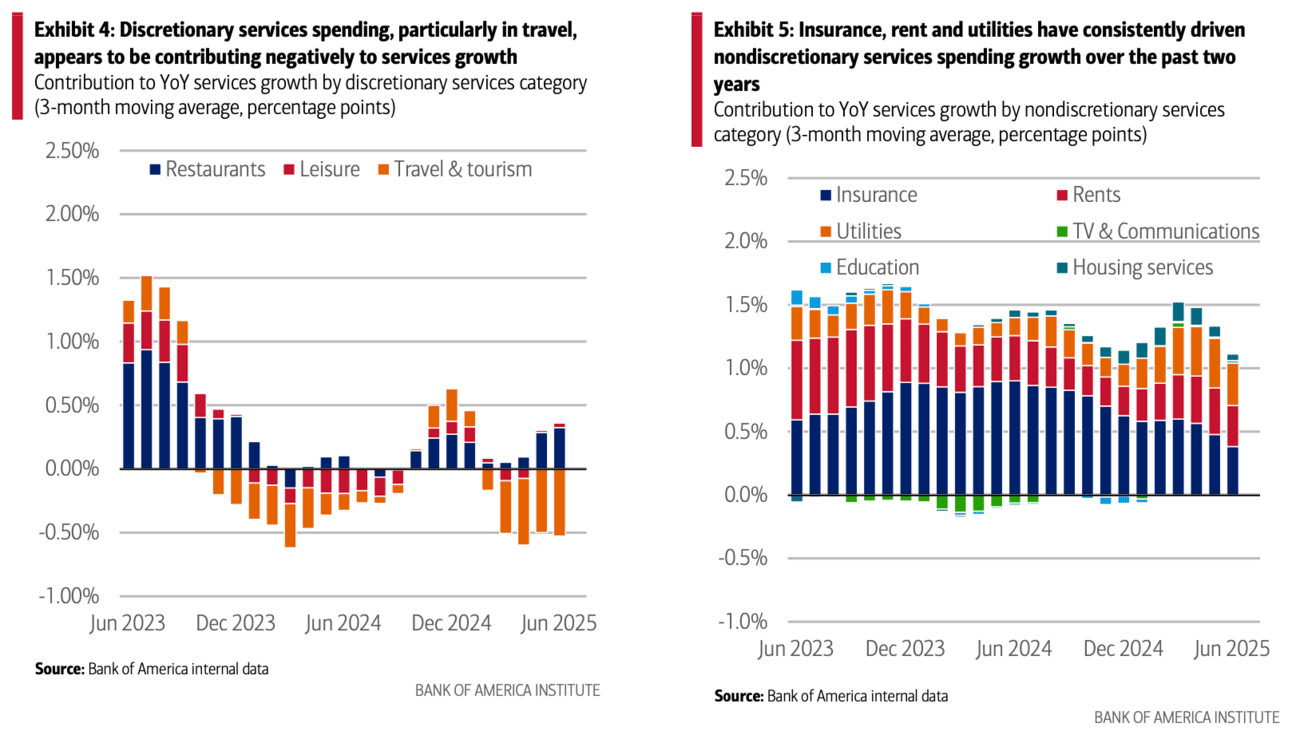

While there was a 0.7% MoM rise in retail spending in June, services spending dropped by 0.1% MoM - the third straight monthly decline.

It appears consumers are pulling back on some areas of discretionary services spending, though this cooling does not currently appear broad-based.

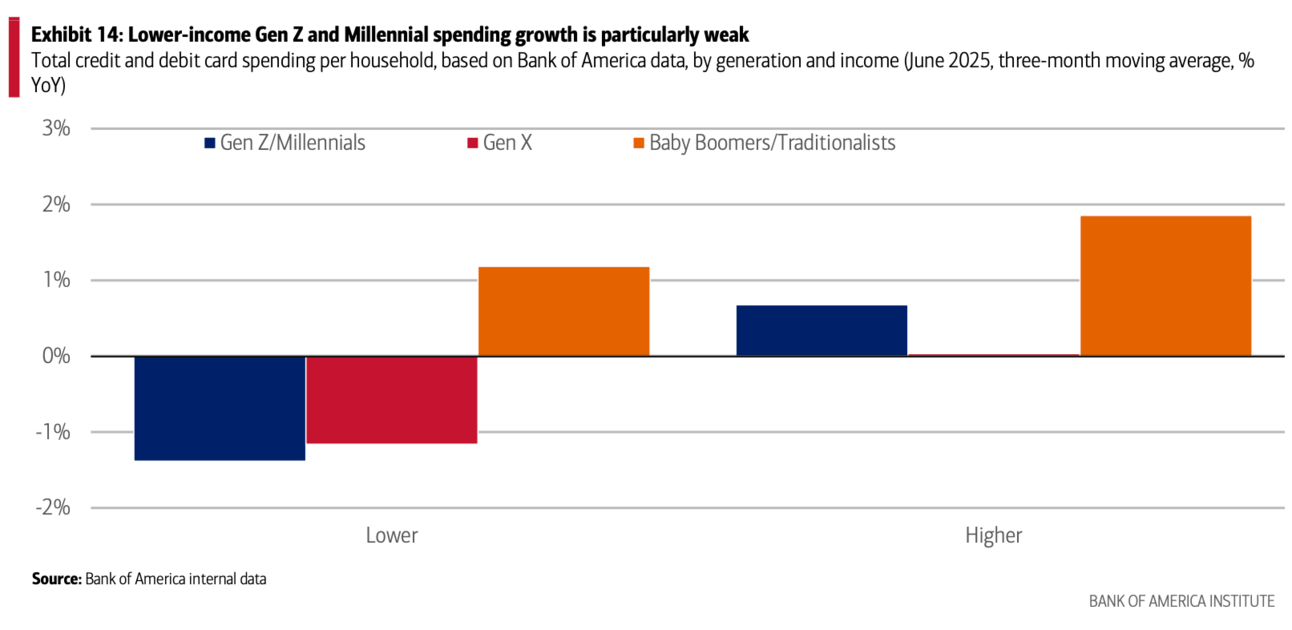

Lower-income households' spending growth is particularly soft, with their total card spending growth negative YoY in the three- months to June; these households also have the weakest after-tax wage growth in Bank of America deposit data. But the spending and wage growth of higher-income households appears to have risen

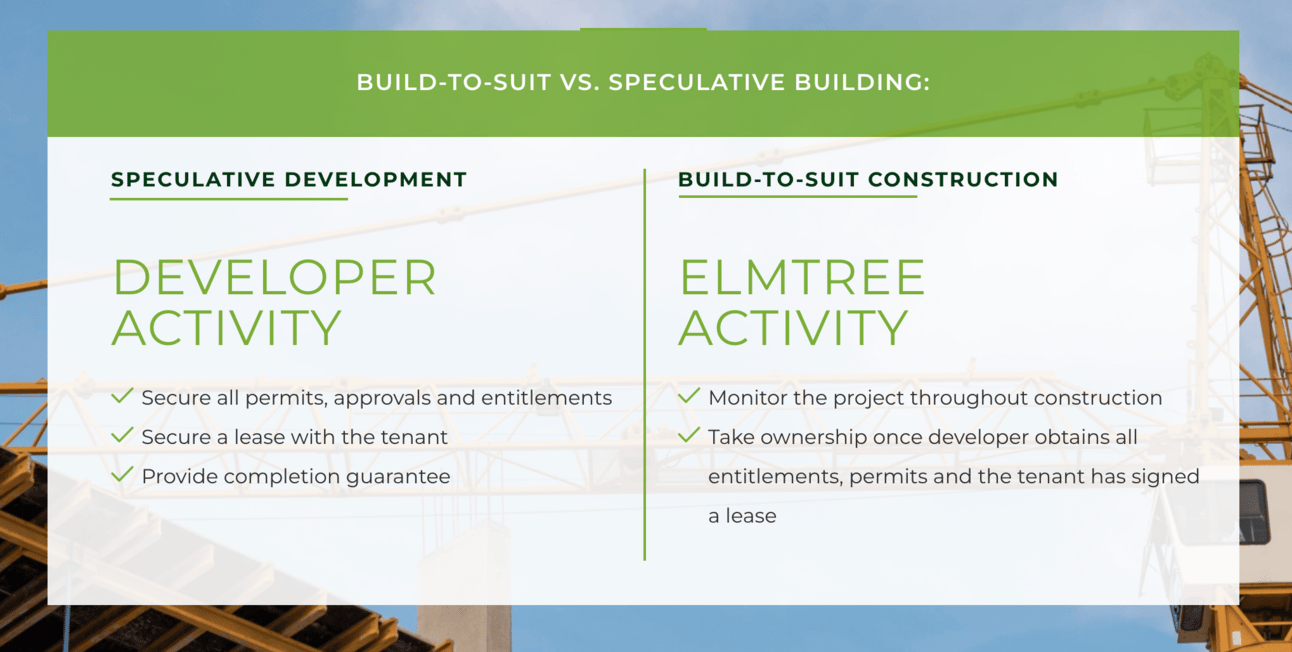

BlackRock has agreed to acquire ElmTree Funds, a commercial real estate investment firm specializing in built-to-suit industrial properties for single-tenant renters.

The firm oversees 257 properties across 37 states, including realized and unrealized properties and ones under contract, letter of intent or agreement, with $7.3 billion in assets under management

Once the acquisition is completed, ElmTree will be integrated into the new Private Financing Solutions (PFS) platform, the result of the recent merger between BlackRock and HPS Investment Partners.

With this addition, PFS aims to scale its presence in the real estate sector, expanding into new markets as an owner-operator. ElmTree will contribute its extensive expertise and network in the commercial real estate market, while HPS will bring its established capabilities as a private credit investor. The synergy between both entities aims to deliver investment solutions with stable income and risk-adjusted returns for both institutional clients and investment-grade companies.

“Structural shifts in the real estate market are creating significant opportunities for private capital. The combination of a leading investor in triple net lease with our private financing platform will allow us to seize those opportunities and offer innovative solutions to our clients,” said Scott Kapnick, chairman of the PFS executive office and CEO of HPS.

James Koman, founder and CEO of ElmTree, noted that the net lease market is estimated at one trillion dollars and reaffirmed the company’s commitment to the build-to-suit industrial model. “Our specialized expertise will be enhanced by HPS’s ability to provide financing and strategic solutions that empower businesses and developers. By joining HPS and BlackRock, we’ll be better positioned to meet market demand and grow alongside our partners,” said Koman.

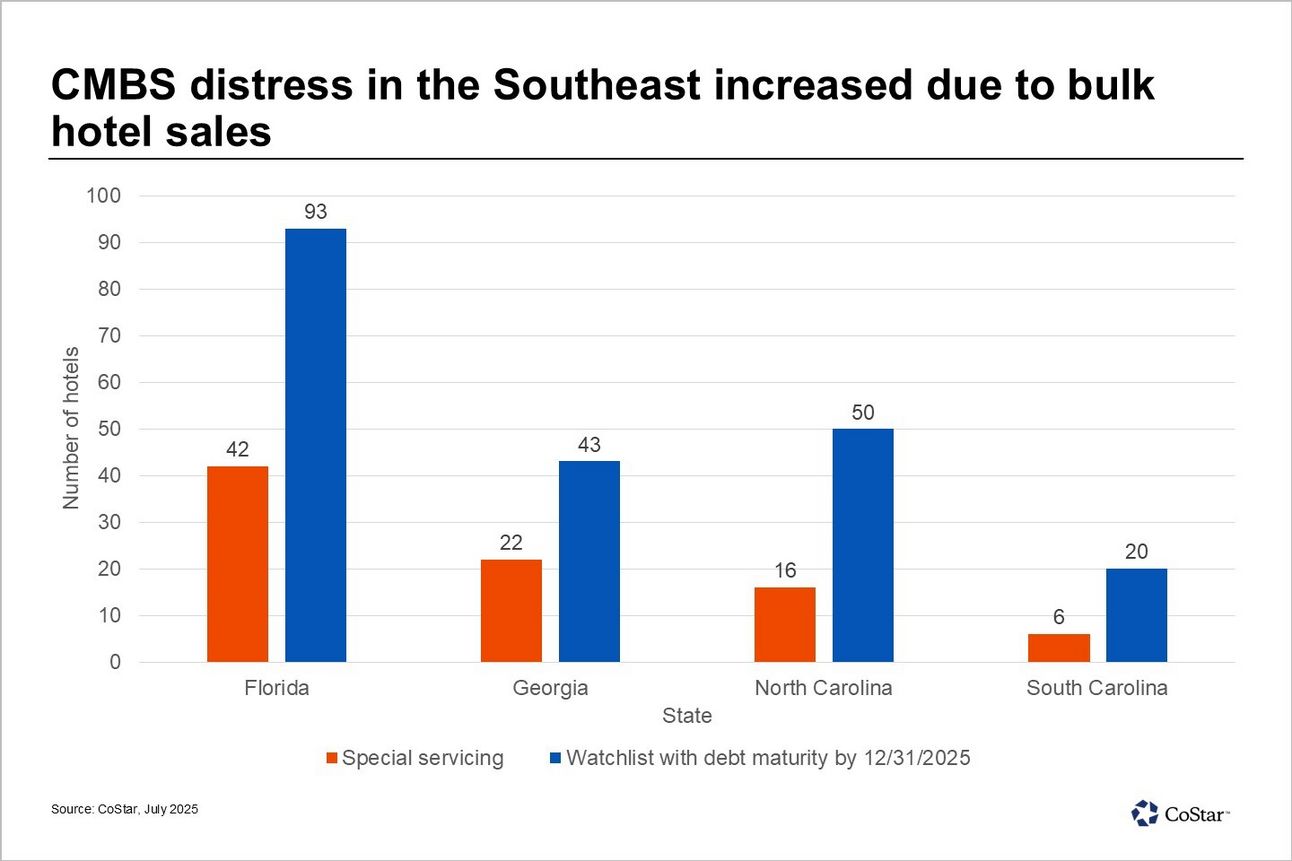

Maturity defaults on hotel commercial mortgage-backed securities loans are on the rise in the Southeast U.S., as some markets in the region experience softening domestic leisure travel or sluggish business travel post-pandemic.

CMBS loan origination volume picked up momentum last year nationally as over $20 billion in securitized debt was issued for hospitality properties, nearly equaling originations for the previous two years combined.

Some CMBS loans that were originated in the past several years are due this year. Slower performance recovery post-pandemic led to less cash flow before debt service, which in turn contributed to underperforming loans.

In the Southeast, 86 hotels are in special servicing, according to CoStar data. Of the 86 Southeast hotels in default, 42 are in Florida, 22 are in Georgia, 16 are in North Carolina and six are in South Carolina. Distressed hotels are concentrated in the mid-tier class, including upper midscale and upscale properties, which account for over three-quarters of the properties in special servicing.

Atlanta as a market has the highest CMBS distress in the region, with 18 hotels under special servicing, according to CoStar data. Atlanta’s subpar performance results from weakening business travel, reduced group volume compared to pre-pandemic levels, and a wave of new hotels that increased competition, especially in the mid-tier class. Orlando, Florida, and Raleigh, North Carolina, are second, with each having nine properties with delinquent payments.

La Quinta properties account for over one-quarter of the distressed hotels. This is mainly due to a $1.5 billion portfolio transaction in early 2022 that privatized CorePoint Lodging, a former publicly traded real estate investment trust that owned more than 100 La Quinta hotels. The hotels were collateralized against CMBS debt, which was due in early 2025 and transferred to special servicing due to maturity default.

14 Courtyard hotels are among the distressed properties in the Southeast. These properties were part of a bulk transaction that took place in mid-2021. CMBS debt originated for this portfolio was transferred to the special servicer two years later, who foreclosed on the collateral and initiated liquidation strategies through several brokerage firms.

The Southeast region contains over 200 hotels on the CMBS watchlist with debt maturity by December 2025, including 93 in Florida, 43 in Georgia, 50 in North Carolina and 20 in South Carolina.

As of the third quarter of 2025, the downtown Houston’s apartment market vacancy rate stands at 11%, a six-year low. Properties are relatively equally split between mid-rises and high-rises, yet there is no significant difference in their respective vacancy rates.

Downtown has been a construction hotspot this past decade, with inventory more than tripling since 2015. Since 2022, nearly 1,800 units have been completed. However, like national and regional trends, groundbreakings have slowed sharply due to a challenging financing environment. Nothing has broken ground since 2022. Looking forward, the house view calls for a slow but steady continued decline in vacancies.

Local property managers have responded to substantial competition from new supply by lowering rents. Rent growth, currently negative 0.3% year over year, places downtown among the worst-performing markets in Houston.

Like other supply-heavy areas such as Neartown/River Oaks and The Heights, downtown has historically been one of Houston's most concession-heavy markets. Local property managers note that often, concessions are necessary to secure a lease. Six to eight weeks of free rent are common for properties in lease-up. For example, the Ely at the Ballpark, which is approaching completion, is offering six weeks of free rent on any unit. The mid-rise is within walking distance of the MetroRail, providing renters easy access to nearby employment hubs.

Aided by a sharp pullback in new supply, rent growth could accelerate in early 2026, so long as demand remains healthy. The house view has annual rent growth exceeding 2% by mid-2026, which would be well above the 10-year average of 0.3%.

Top-of-mind concerns for many local property managers include high office vacancies in the central business district, crime, and a significant presence of homeless residents. Some companies, such as LyondellBasell, have moved west to be closer to their workforce and to newer buildings. Should more firms follow suit and leave the cbd, this could challenge apartment demand.

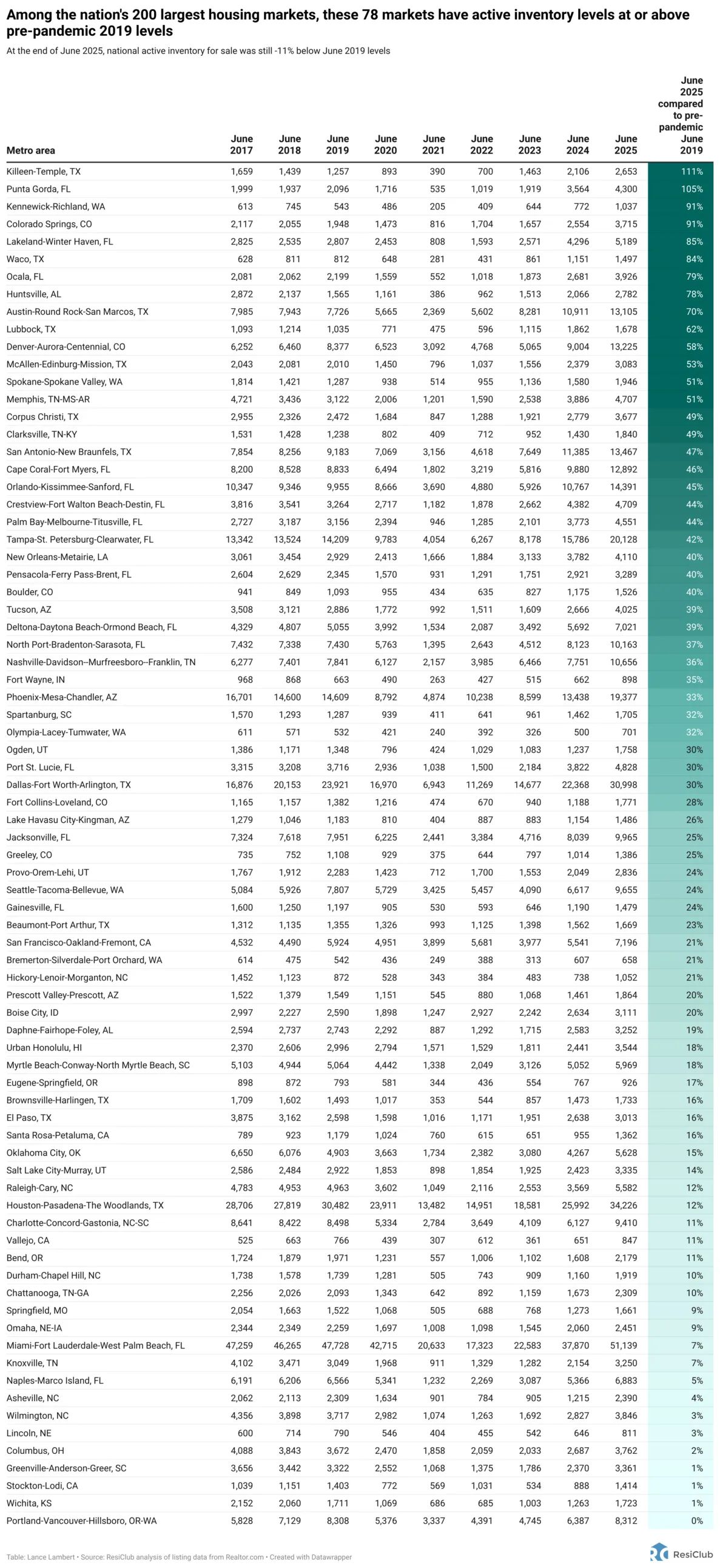

At the end of June 2025, national active housing inventory for sale was still -11% below June 2019 levels. However, more and more regional markets are surpassing that threshold. This list is growing.

January 2025: 41 of the 200 largest metro area housing markets were back above pre-pandemic 2019 inventory levels

February 2025: 44 of the 200 largest metro area housing markets were back above pre-pandemic 2019 inventory levels

March 2025: 58 of the 200 largest metro area housing markets were back above pre-pandemic 2019 inventory levels

April 2025: 69 of the 200 largest metro area housing markets were back above pre-pandemic 2019 inventory levels

May 2025: 75 of these 200 major markets were back above pre-pandemic 2019 inventory levels

Now, at the latest reading for the end of June 2025, 78 of the 200 markets are above pre-pandemic 2019 inventory levels and ResiClub expects that count will continue to rise this year.

Among these 78 markets, you’ll find lots in Sun Belt markets like Florida, Texas, Arizona, and Colorado. Many of the softest housing markets, where homebuyers have gained leverage, are located in Gulf Coast and Mountain West regions. Some of these areas were among the nation’s top pandemic boomtowns, having experienced significant home price growth during the pandemic housing boom, which stretched housing fundamentals far beyond local income levels.

When pandemic-fueled domestic migration slowed and mortgage rates spiked, markets like Cape Coral, Florida, and San Antonio, Texas, faced challenges as they had to rely on local incomes to sustain frothy home prices. The housing market softening in these areas was further accelerated by the abundance of new home supply in the pipeline across the Sun Belt. Builders in these regions are often willing to reduce net effective prices or make other affordability adjustments to maintain sales. These adjustments in the new construction market also create a cooling effect on the resale market, as some buyers who might have opted for an existing home shift their focus to new homes where deals are still available.

In contrast, many Northeast and Midwest markets were less reliant on pandemic migration and have less new home construction in progress. With lower exposure to that demand shock, active inventory in these Midwest and Northeast regions has remained relatively tight, keeping the advantage in the hands of home sellers.