- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 07.19.25

Location Strategy Chartbook 07.19.25

Real Estate Market Insights

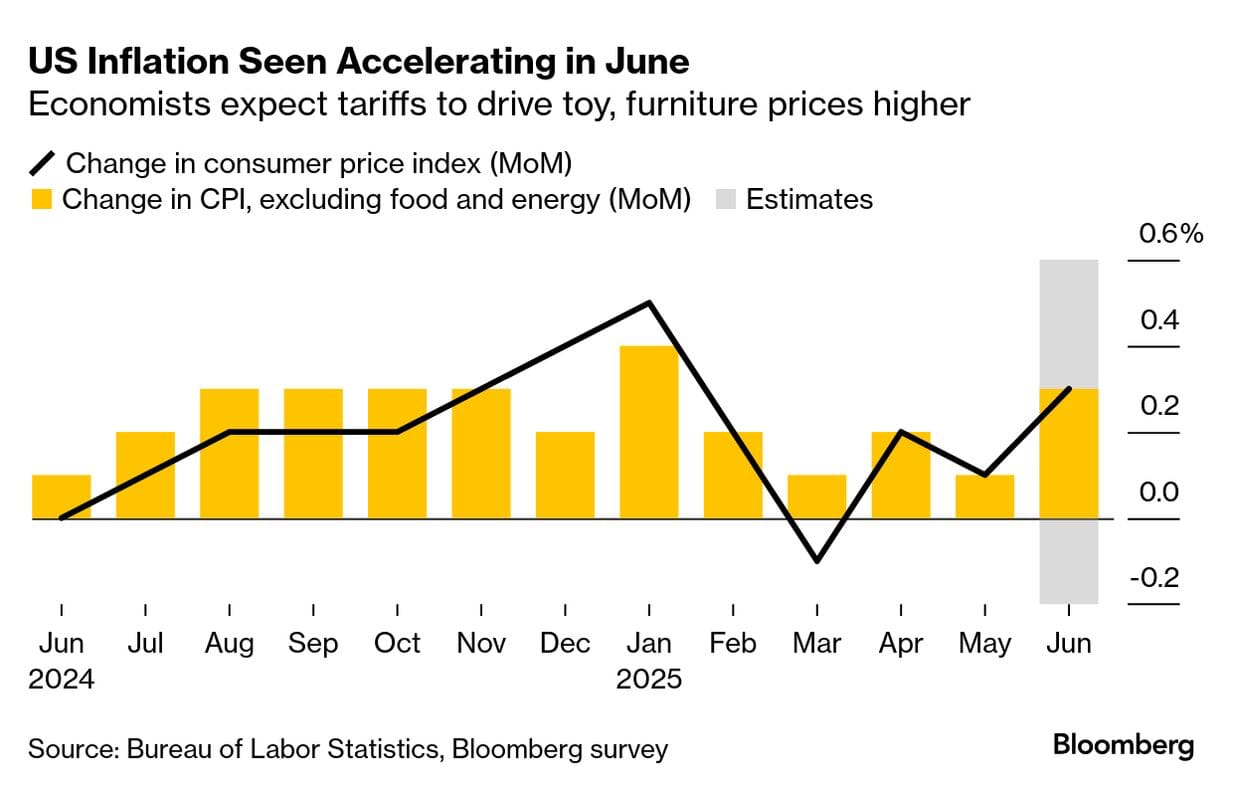

Economists have long warned of a tariff-driven boost to US inflation, and the next report on consumer prices will put their conviction to the test. For four months, consumer price index readings from the US Bureau of Labor Statistics have come in cooler than what economists predicted, and those forecasters are again warning of acceleration, with June data due Tuesday. Economists see price rises in tariff-exposed categories including furniture, toys, recreational goods and cars.

There’s widespread consensus among Federal Reserve officials and private-sector forecasters that inflation will turn higher during the summer as businesses start passing on tariffs to consumers. While many firms chose to initially shield customers by stocking up on inventories in advance or even absorbing part of the higher costs at the expense of lower margins, some are now running out of options

Second-quarter corporate earnings reports may offer important clues on how President Donald Trump's tariff policies are affecting US companies.

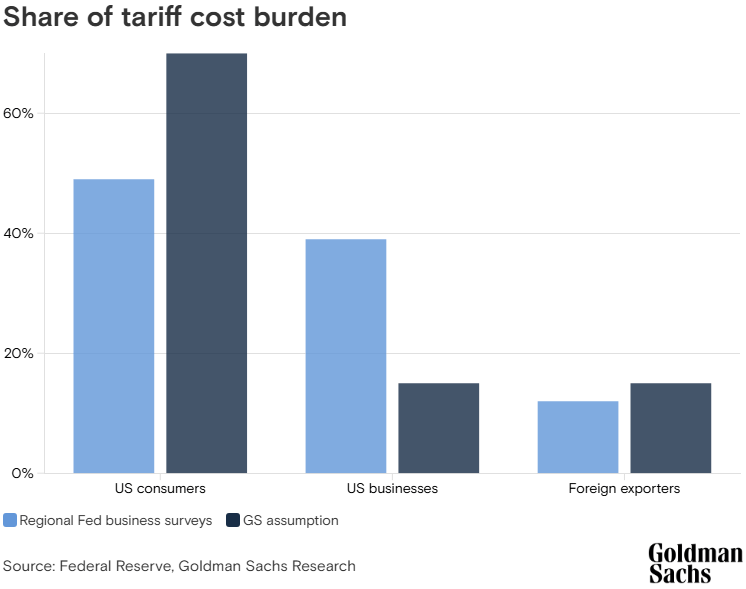

Economists at Goldman Sachs Research assume that companies will pass on 70% of the direct cost of tariffs to consumers through higher prices. But surveys have only showed limited inflation in consumer prices.

“Companies have so far only announced modest price increases this year, although increases have been larger among firms most exposed to tariffs,” writes David Kostin, chief US equity strategist in Goldman Sachs Research, in a recent report.

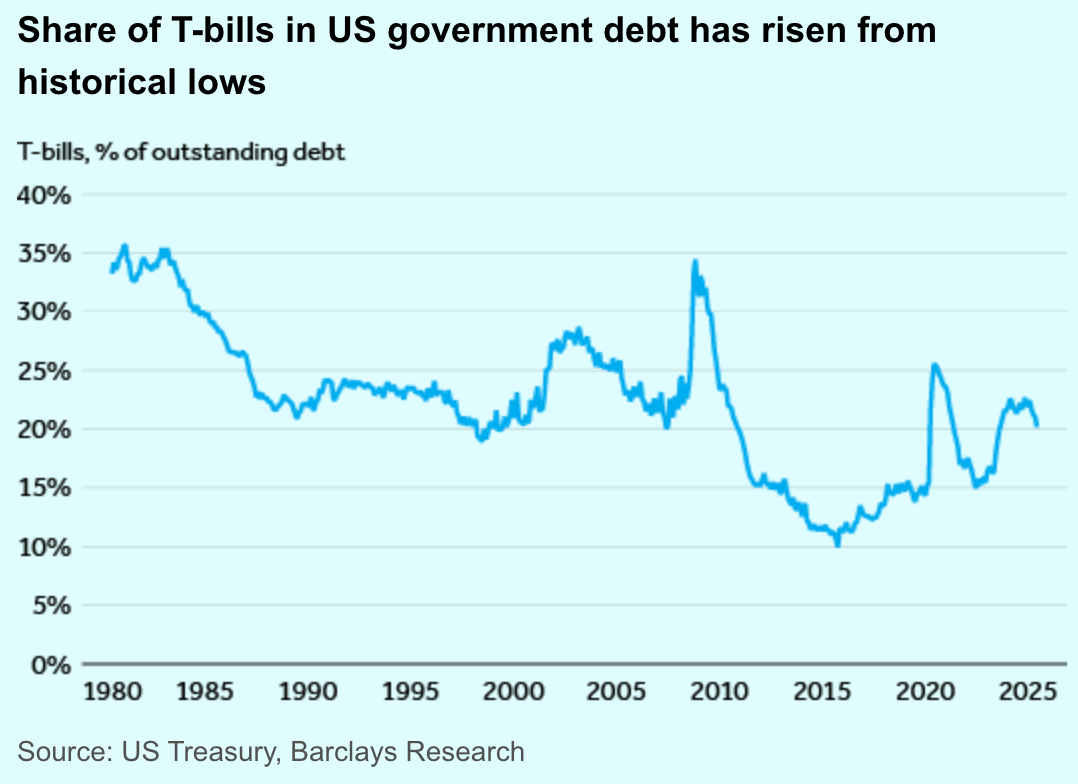

As the yield on the 30-year US government bond lingers around 4.9%, our rates strategists look at the implications of the bill on long-term bond yields and how the Treasury might counter its effects through a change in the composition of bill and bond issuance.

US government budget deficits are likely to remain at about 6.5% of GDP, as new tax cuts in the bill are offset by spending cuts and tariff revenues. That will still mean a rising dollar value of the deficit, from $1.9 trillion in the current fiscal year to $2.9 trillion in 10 years. But that will not necessarily translate to higher bond issuance for several years at least, our strategist argue, as the Treasury shifts issuance away from long-term bonds and notes toward short-term bills, as recently hinted at by Treasury Secretary Bessent.

The issuance of long-term government securities will remain the same in the next two years while T-bill sales rise, our strategists expect. That would likely raise the share of T-bills in outstanding government debt from 22% now to 25% in 2027. Although that might seem very high compared with their 10% share in 2015, it is in line with levels prior to the 2008 financial crisis.

The Treasury aims to fund the government at the least cost to the taxpayer over time. When the term premium is high for government securities, it makes sense to lean toward short-term debt, and vice versa. And we are currently in a high term premium world.

The change in the composition of bill and bond issuance should help compress the term premium for long-term debt by about a quarter percentage point, our strategists believe. That should drive down 30-year Treasury yields through the end of the year. Lower long-term yields can keep government borrowing costs down, as well as lower them for companies and consumers as some of their debt is priced on long-term Treasury yields. Share of T-bills in US government debt has risen from historical lows

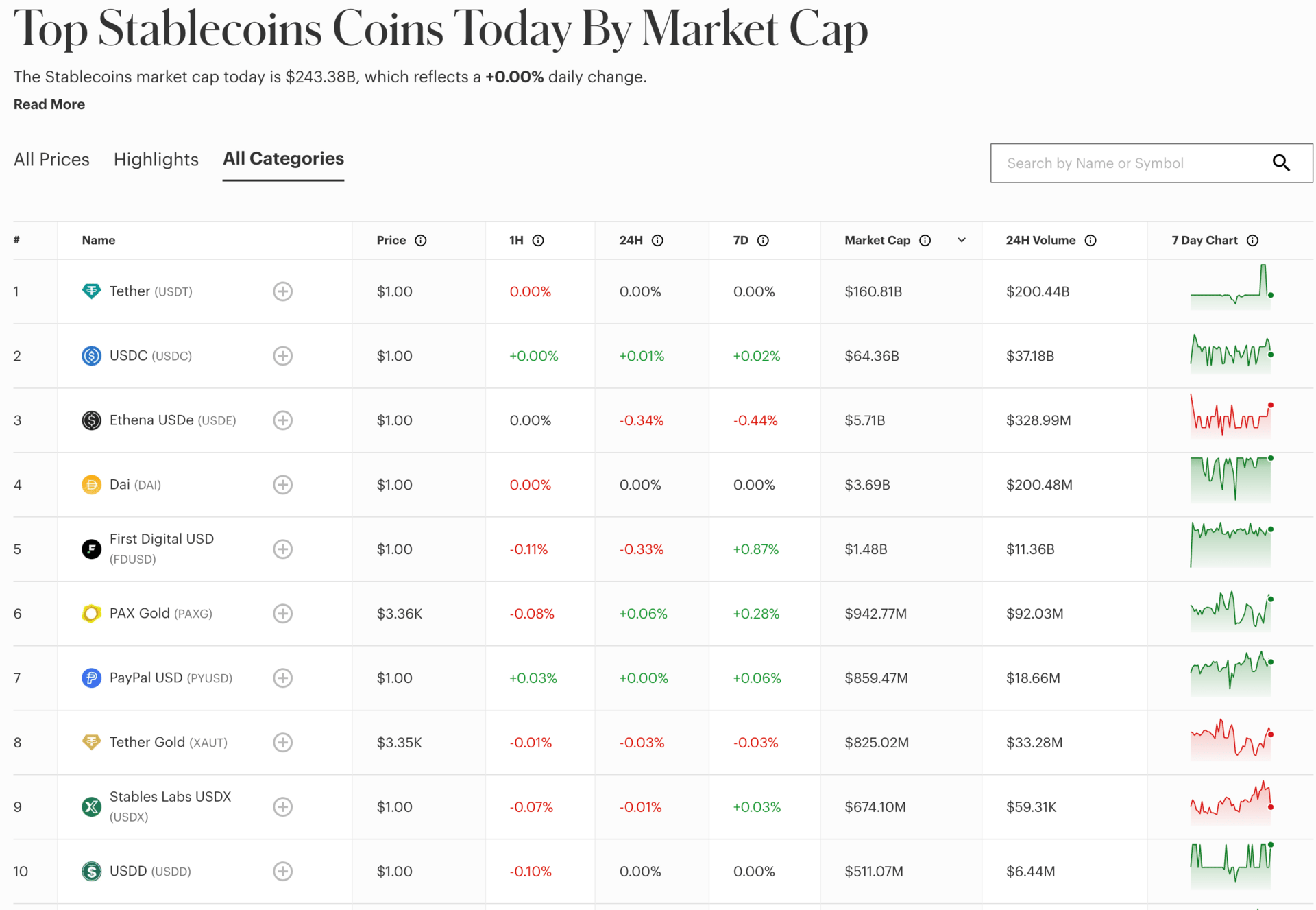

Bloomberg: Congress passed the first federal legislation to regulate stablecoins, marking a political coming-of-age for the crypto industry. It may unlock faster, cheaper forms of payments—and bring legitimacy to a $265 billion market some predict might swell to $3.7 trillion by 2030. Wall Street is warming to the “digital dollar.” Retailers too. But the road ahead is full of obstacles.

In a rare public embrace of the once-shunned world of crypto, the heads of America’s largest banks made one thing clear this week: stablecoins are no longer at the fringe of finance. On earnings calls, JPMorgan’s Jamie Dimon, Bank of America’s Brian Moynihan and Citigroup’s Jane Fraser each described the upstart “digital dollar” as a potential threat to the banking industry’s grip on payments — and signaled they’re preparing to respond.

Unlike more volatile cryptocurrencies, stablecoins are designed to hold their value and settle payments instantly, around the clock. That simple functionality — fast, programmable dollars — has been drawing interest from companies and platforms that might otherwise rely on banks.

Now, senior bankers are previewing how they’ll defend their grip on one of banking’s most fundamental pillars — exploring tools like deposit tokens and bank-issued stablecoins. “They’re trying to get into payment systems and rewards programs,” Dimon said, referring to fintech firms pushing into banking and payments. “We have to be cognizant of that.”

Forbes

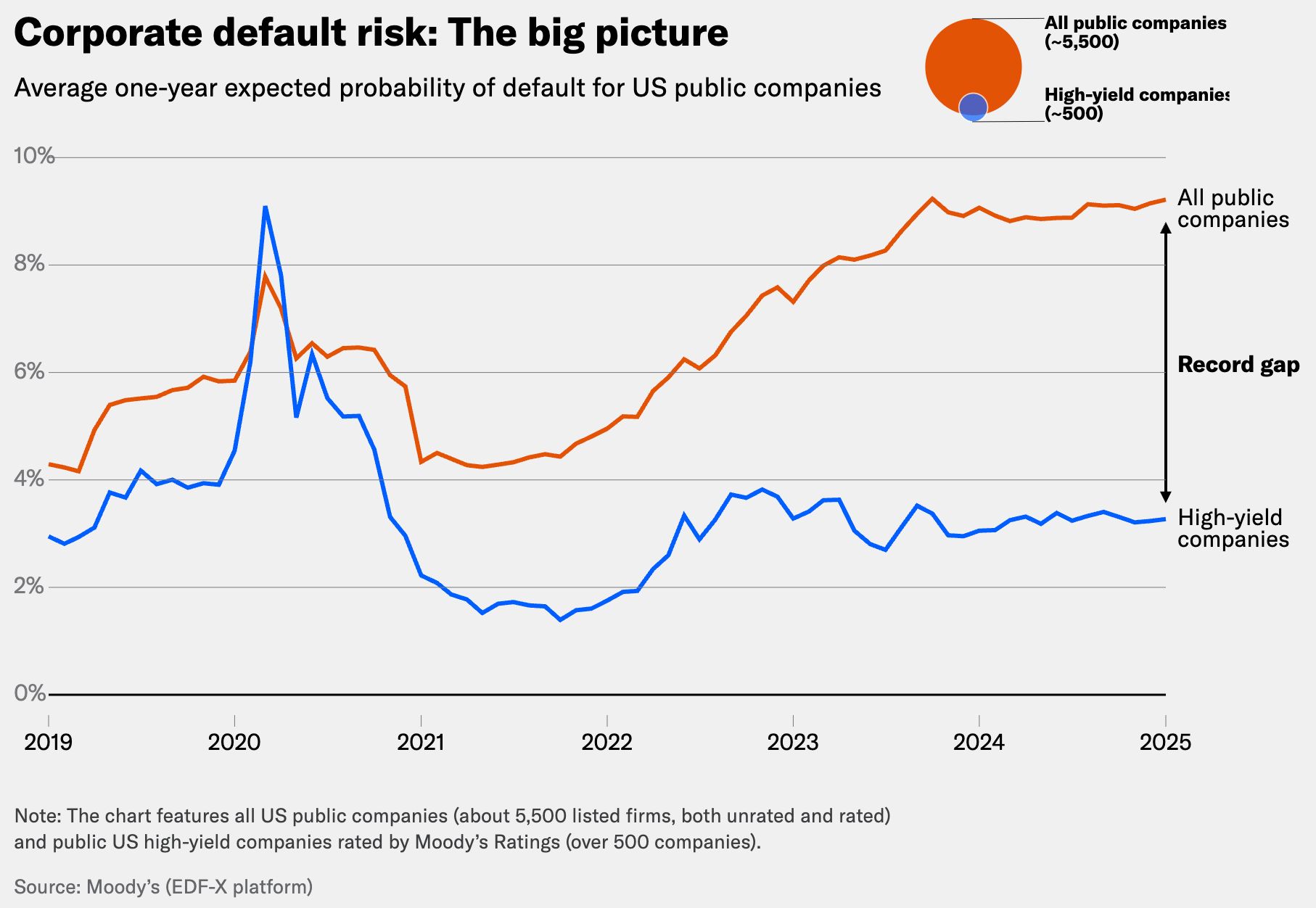

The number of companies at the greatest risk of defaulting are at an 11-month high, as uncertainty around US trade and tariffs worsened credit conditions, according to a Moody’s Ratings report.

In the second quarter, 16 companies were added to the cohort of businesses with the highest default risk, according to Moody’s. The group now stands at 241 companies, the report shows.

“With US tariffs and trade uncertainty unsettling global commerce in April, credit conditions have deteriorated” since the beginning of the year, the analysts wrote. The group includes US non-financial corporates with a Moody’s rating at or below the highly speculative Caa1 rung or with a higher B3 rating but are at risk of a downgrade.

Beauty products company Conair Holdings and brake kit company Power Stop are among companies Moody’s downgraded further into junk in the second quarter, given “significant pressure on their earnings and cash flow from high tariffs on goods sourced from China and other countries,” according to the report. With market volatility, the number of companies that defaulted also increased last quarter compared to the prior period. More than four times as many companies moved off the highly speculative list because of a default than companies that moved off the list via an upgrade, according to Moody’s. Most were technology companies, though Moody’s expects companies within the consumer products sector to see more defaults in coming months.

Distressed debt exchanges remain the leading type of defaults, according to Moody’s. Companies typically propose distressed exchanges — a kind of restructuring agreement — to avoid bankruptcy, improve liquidity, reduce liabilities and manage upcoming debt maturities, the ratings firm said.

Private equity-owned companies, which comprise 76% of those on Moody’s highly speculative list, opt into distressed exchanges more frequently than non-PE owned businesses. “We anticipate this trend of out-of-court debt restructuring will persist throughout the year, given that PE-owned companies make up a significant portion of our distressed debt population,” the analysts wrote. Facing liquidity challenges, upcoming maturities and high interest rates, Moody’s expects private equity firms to “leverage every available option” to avoid bankruptcy, which would erode their equity stakes, according to the report.

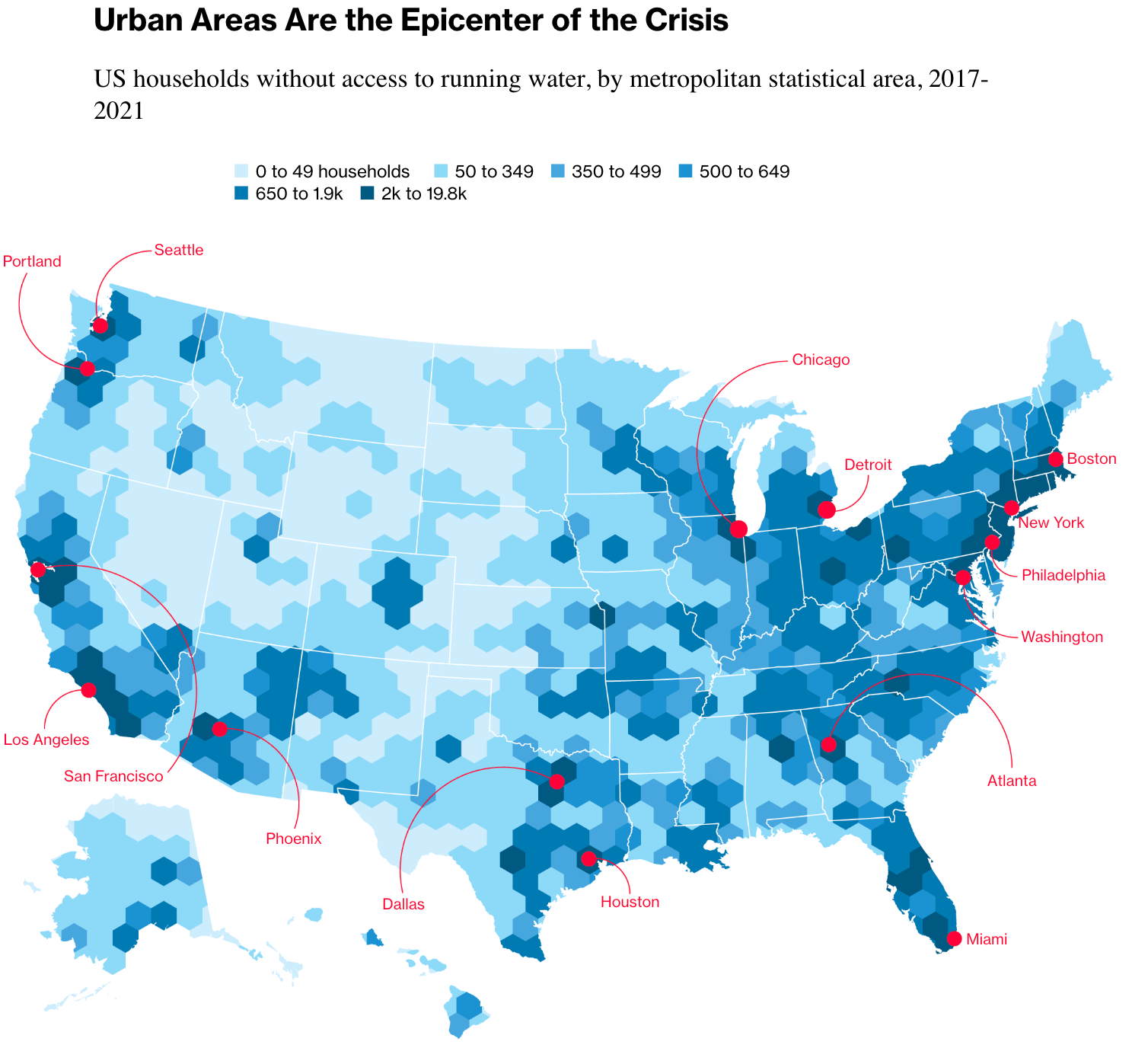

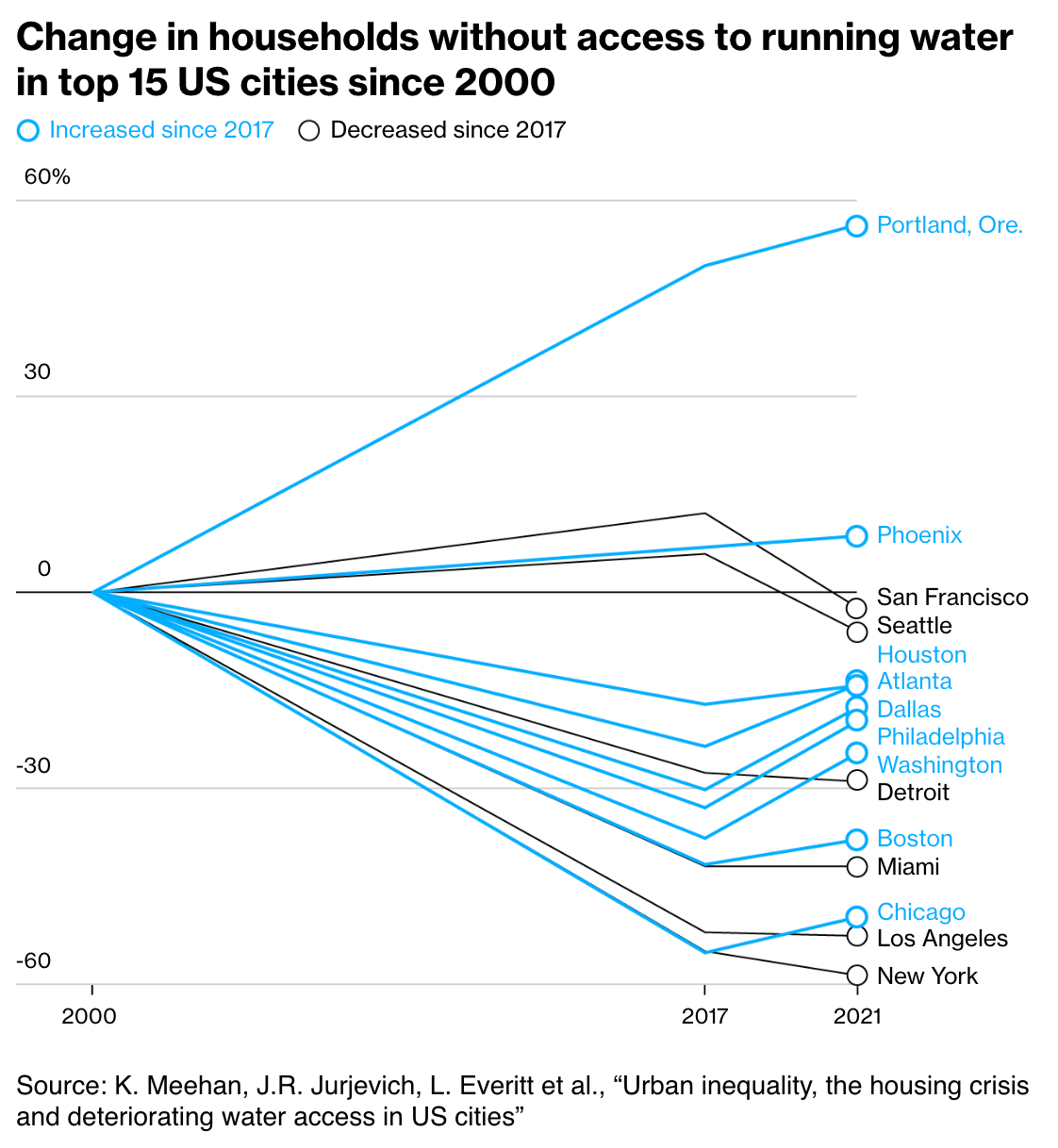

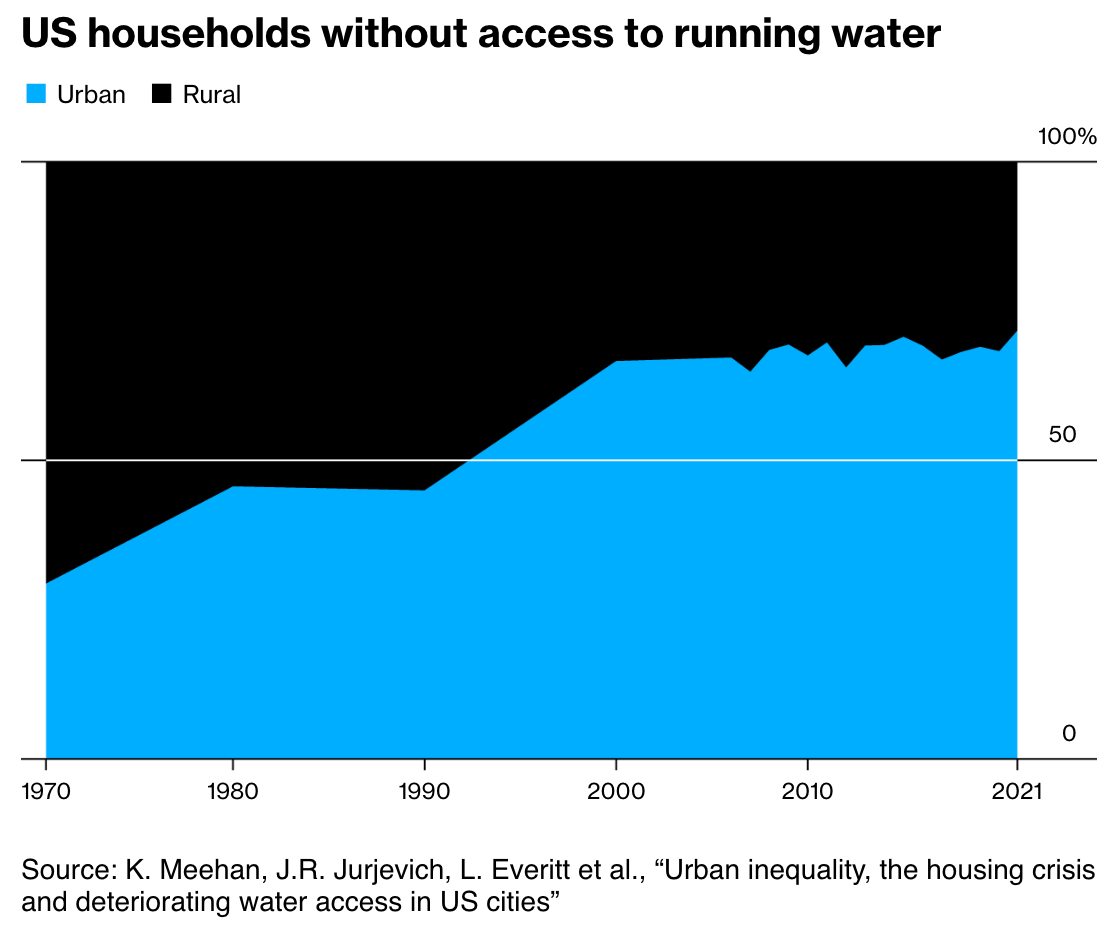

Across the world, access to clean running water has long been considered a key marker of economic advancement. Yet in several of the most prosperous cities in the richest nation on Earth, the share of households living without that critical service is climbing—a trend that researchers say demands attention.

“Plumbing poverty” is surging in Houston, Phoenix, Portland, Oregon and other urban areas.

72% of US households lacking running water live in metropolitan areas, more than double the proportion from the early 1970s.

In many wealthy places—including Houston, Phoenix and Portland, Oregon—the problem worsened from 2017 to 2021, the most recent year for which complete census data is available.

Meanwhile federal water investment has plummeted over the last 50 years, going from 63% of capital spending in 1977 to just 9% in 2017. In his 2026 budget proposal, Trump is seeking an almost 90% cut to the two primary funds that provide federal support for water and sewer systems, a key resource for keeping water safe and accessible at the community level.

LS Note: In conversation with multiple market study clients, real estate attorneys, engineering firms, developers, brokers, etc throughout Texas regarding the challenges and costs around water are a growing issues and concern and evaluation in site selection.

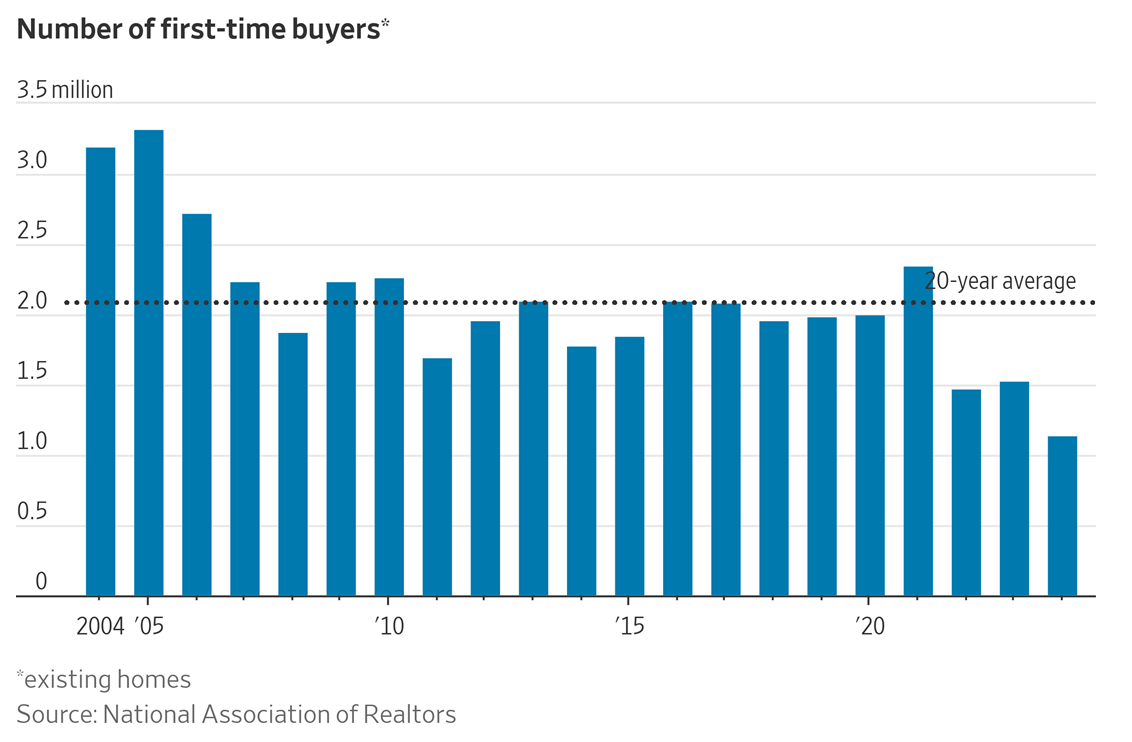

WSJ: First-Time Home Buyers Are MIA. Landlords Are the Winners. America’s renter population has hit a record because fewer people can afford to get on the housing ladder

On average, 2.1 million people a year became first-time buyers over the last two decades. Unaffordable house prices and high mortgage rates have slowed this flow since 2022.

There were 1.1 million first-time buyers last year—380,000 fewer than in 2023 and almost half the historical norm, data from the National Association of Realtors shows.

This year could be even worse judging by the weak spring home-selling season. Based on sales through May, the U.S. is on track to sell 4.03 million homes in 2025, fewer than last year’s tally, which was the lowest since 1995.

The sharpest slowdown is happening among properties that cost less than $500,000, NAR data shows. That is the price range that usually attracts first-time buyers.

The market for newly built homes is also slumping. In May, sales dropped 6% compared with the same month of 2024. This part of the housing market is a good proxy for how first-time buyers are feeling because builders have grown more dependent on demand for starter homes. First-time buyers’ share of new-home sales has doubled in recent years to around 40%, according to the National Association of Home Builders.

Big home-builders with financing arms such as D.R. Horton targeted young buyers by offering mortgage-rate buydowns that make monthly repayments more affordable. But these sweeteners are no longer working as well as they used to.

Builder Lennar said it had to offer incentives equivalent to a 13.3% price discount in its second quarter to entice buyers—the highest rate since 2010. This is eating into builders’ profit margins.

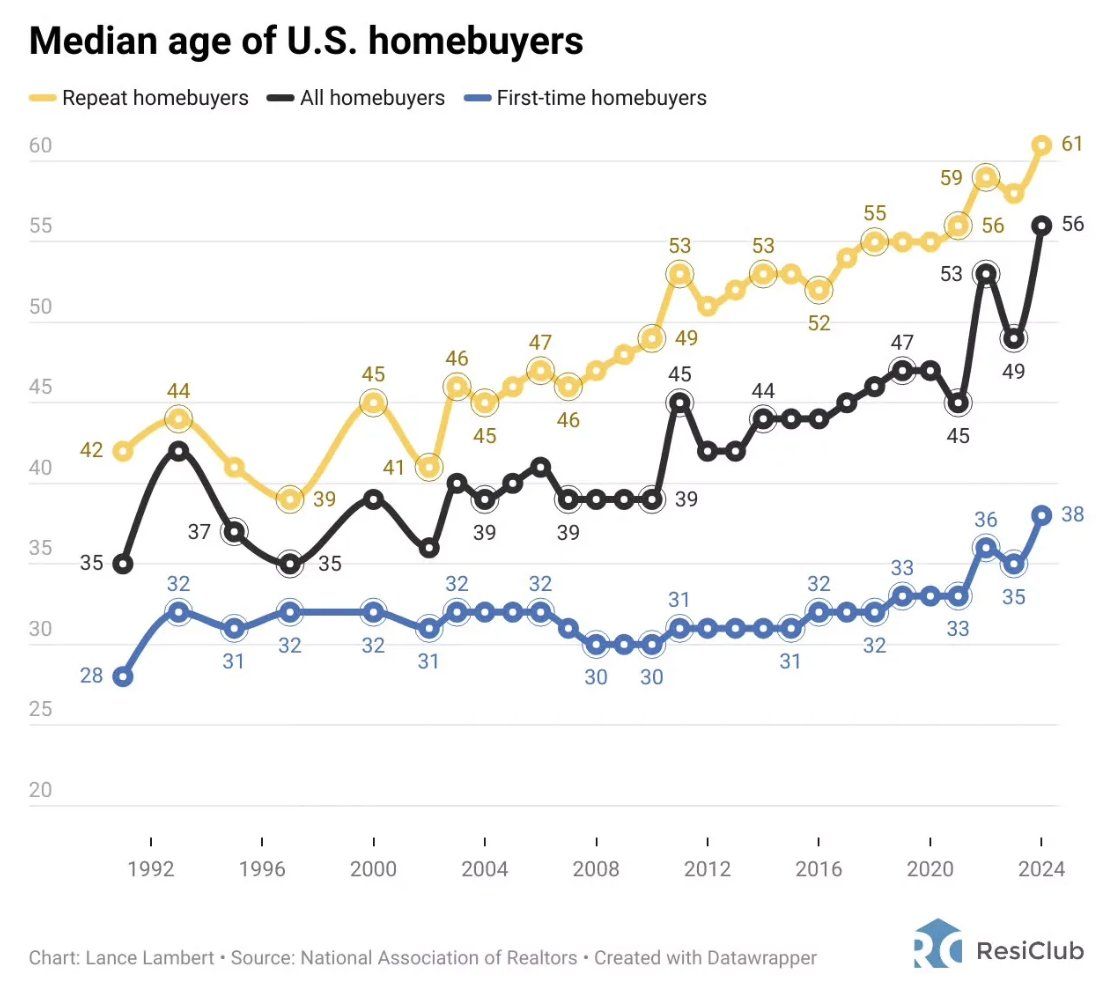

The flip side of sluggish demand from first-time home buyers is a rapidly swelling population of tenants. In a bullish sign for landlords, the number of renter households in the U.S. has reached a record 46 million. At least 1.2 million of these households could be “trapped renters” who would like to buy, based on the above-average renter household formation seen over the past three years. The true extent of pent-up demand to buy is probably much greater. Gen Z and millennial Americans have lower rates of homeownership than baby boomers did at the same stage of life.

At today’s prices, buyers would need to earn $127,000 to afford the monthly mortgage repayments on a median-priced home, up from $79,000 in 2021, according to Harvard’s Joint Center for Housing Studies. Only 6 million of the country’s 46 million renters clear this hurdle.

A fresh obstacle to homeownership is emerging. Credit scores recently took a hit after a pause on reporting student-loan delinquencies to credit agencies ended.

This caused the delinquency rate on the outstanding balance of student loans to jump to 8% in the first quarter, up from 1% previously. Around 2.4 million newly delinquent borrowers who would have qualified for a mortgage before the reporting change will no longer be eligible, according to the Federal Reserve Bank of New York. With more households stuck renting, apartment vacancy rates are falling. This should help landlords recover from a glut that kept a lid on rent growth for the past 18 months. The stage is set for fresh rent increases as the market tightens.

Costar: A company that bills itself as the largest player in the fast-growing U.S. industrial outdoor storage sector has landed a new loan backed by a portfolio of 64 properties across 22 states, a deal that marks Alterra IOS’ second big financing of 2025.

Alterra on Wednesday announced it borrowed $343.6 million from Truist Financial and Bank of Montreal to replace maturing debt. That follows a $189 million loan in February from Blackstone Mortgage Trust to finance recently purchased properties.

The latest loan was executed on behalf of Alterra IOS Venture II, a closed-end fund with $524 million of equity commitments, Alterra said in a statement.

The loan backs properties with a combined 580 acres in top logistics markets including Atlanta, Houston, Chicago, Northern California and Dallas-Fort Worth, according to the statement.

Alterra’s new financing deal is the latest example of industrial outdoor storage, a once-obscure niche in the broader industrial property sector, attracting new investors and lenders in recent years.

Facilities typically have acres of land and a relatively small building for offices and indoor storage. Tenants use the outdoor space to store vehicles, trailers, containers and building materials, often near major expressways, airports, railroads and ports.

Alterra says it is the largest owner of such properties in the country, having acquired more than 350 properties in 37 states.

Philadelphia-based Alterra made a splash in late 2024 with the $490 million sale of a 14-state portfolio to Peakstone Realty Trust.

Investors including Manulife Investment Management and TPG Angelo Gordon also have been pouring dollars into industrial outdoor storage.

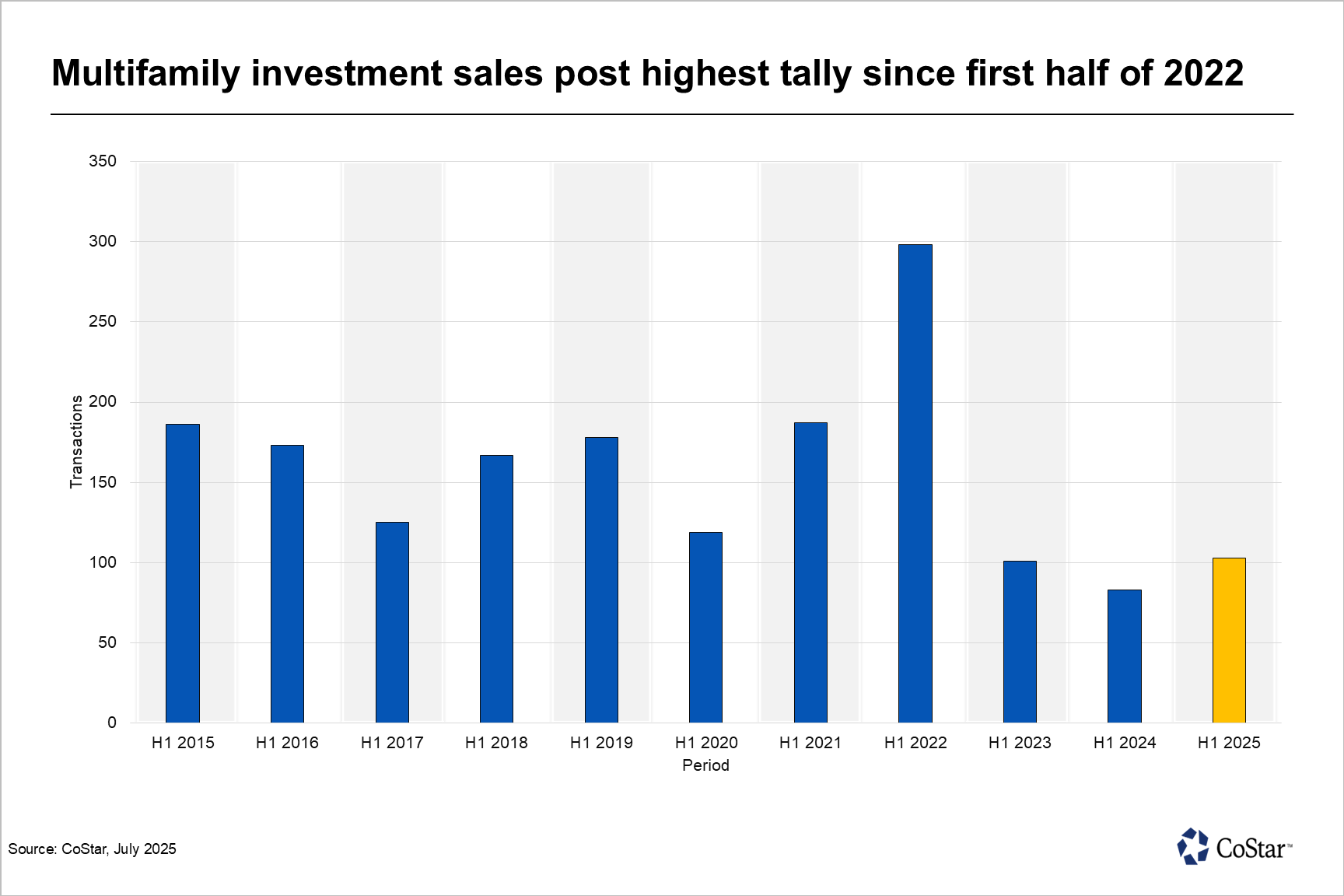

Investors return to Houston's multifamily market. Momentum in Houston's multifamily investment market continued to build in 2025 following a steady recovery throughout 2024. Disclosed multifamily sales volume stood at roughly $1.2 billion in 2024, more than double the 2023 figure.

This pace carried into the first six months of the year. The total number of transactions during this time was roughly 24% above the same time last year and the highest first half of the year figure since 2022, suggesting that investor activity is holding firm, despite uncertainty for the broader economy.

Freddie and Fannie are the most active lenders, but debt funds and banks are back as well. Life insurance companies are active with stabilized, Class A deals.

Local brokers note that investors are shying away from value-add deals for a variety of reasons, including difficulty in obtaining financing and general distress among some of them, and are instead targeting core and core-plus properties. New supply in the luxury segment is slowing, but demand has remained strong.

CoStar’s data echoes this: over the past six months, roughly 60% of properties 100 units or larger that traded were four- and five-star properties, up from the 2015 to 2019 average of 34%.

The most active bidders are private, family-office money, private equity and syndicators. Institutional capital is slowly and selectively returning. In June, Berkshire acquired the 297-unit The Ivy from Stonelake Capital Partners for an undisclosed price. The 2017-built 17-story high-rise is in the River Oaks area, one of the most affluent neighborhoods in Houston, and was around 94% leased at the time of sale.

Large four- and five-star properties like this one now trade in the high 4% to low 5% range, up from the 2.5% to 3.5% range seen a few years ago. Meanwhile, three-star buildings are now trading in the 5.5% to low 6% range, while the one- and two-star properties are now pushing north of 6%.