- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 08.02.2025

Location Strategy Chartbook 08.02.2025

Real Estate Market Insights

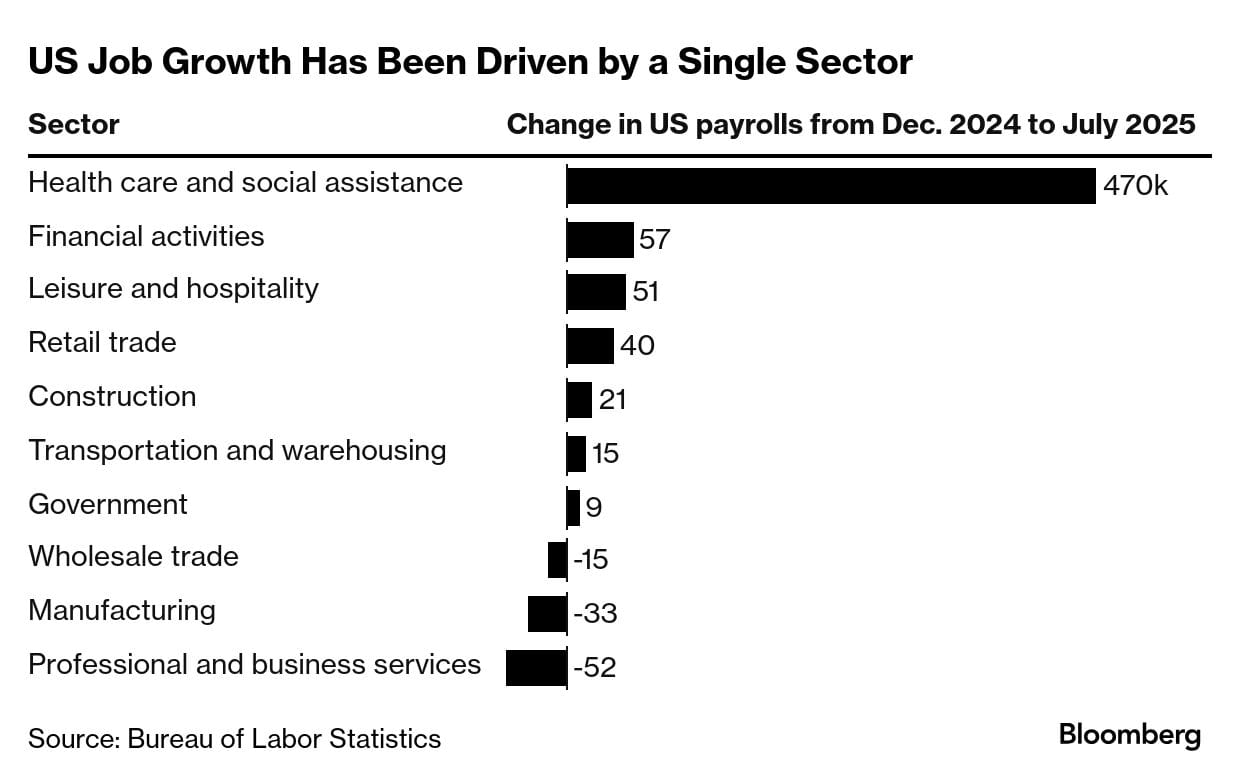

Bloomberg: US job growth cooled sharply over the past three months and the unemployment rate rose, showing the labor market is shifting into a lower gear amid widespread economic uncertainty. Payrolls increased 73,000 in July after the prior two months were revised down by nearly 260,000, according to a Bureau of Labor Statistics report out Friday. In the last three months, employment growth has averaged a paltry 35,000 — the worst since the pandemic.

The data send a stronger signal that the labor market is weakening more notably. Not only is job growth cooling markedly and unemployment rising, it’s harder for unemployed Americans to get a job and wage gains have largely stalled.

That poses further risks to a slowdown in consumer and business spending that’s already underway. The report caps a week of high-profile data that show underlying economic momentum is cooling and inflation progress is stagnating, reasons why the Federal Reserve chose to keep interest rates unchanged again in a divided decision. Chair Jerome Powell maintained that the labor market is solid and the central bank needs to be wary of inflation risks — especially with President Donald Trump’s latest round of tariffs.

There was one piece of seemingly good news—an acceleration in health-care hiring—in the otherwise alarming report. Looking ahead, it probably represents even greater cause for concern.

Health care tends to be more immune to economic turmoil. If there’s an aging population with Medicare access and abundant Medicaid support, there’s always a customer to serve. Back in the early 1990s, in 2001 and during the Great Recession of 2007 to 2009, health-care employment increased while other industries shed jobs.

Without gains in health-care employment last month, the US wouldn’t have added any jobs at all. Even more so, since the start of the pandemic health care has been a critical contributor to employment. During the past three years, the sector accounted for 43% of all new jobs, up from about 22% in the three years before the onset of Covid-19.

Donald Trump set a 10% global minimum tariff, with rates of 15% and higher for countries with significant trade surpluses with the US. Canada is among the hardest hit with levies increased to 35%, but USMCA goods remain exempt. Switzerland got slammed with 39%.

As large US budget deficits raise questions about debt sustainability, fiscal concerns are beginning to affect prices for longer-maturity government bonds and the US dollar. There are signs, however, that the country's equity market will power ahead this year.

Goldman Sachs Research's economic outlook for the US, meanwhile, is on the cautious side, set against a backdrop of tariff increases: While the US is expected to avoid a recession, its GDP is forecast to grow by only about 1% this year as tariff rates rise, says Jan Hatzius, Goldman Sachs' chief economist, on an episode of The Breaks of the Game podcast. The risk of recession is around 30%, which is double the historical average.

“On the economy, it's going to continue to be a slog,” Hatzius says in the episode, hosted by Tony Pasquariello, global head of hedge fund coverage in Global Banking & Markets. While import taxes have had little impact on prices so far, Hatzius expects core inflation to increase by about a percentage point to more than 3% this year.

Brandon Roth, IPA: Last week I reached out to the institutional JV equity market to find out who has closed a deal recently and what the profile looked like.

Most groups said they haven't closed anything relevant. Example responses include:

"Unfortunately, we haven’t closed any JVs recently. We’ve actually been building out our 'direct' business (i.e., no JV partner)."

"Wish I had something to contribute. We have not been very active in the last 12 months."

"We’re primarily focused on issuing preferred equity in this environment where we are getting attractive risk adjusted returns behind Freddie Mac."

"Sorry we haven’t closed on anything recently. It’s been a tough/slow market for new JVs and development (where we typically JV)."

"Unfortunately, our equity business outside of the data center space has been sidelined for almost two years now so I don’t have any relevant data points to share."

That being said, there were 17 groups that provided 35 recent deals. This is a mix of private equity funds, insurance companies, family offices, and foreign capital.

Not a huge surprise, but 29 out of the 35 deals (83%) were multifamily or industrial.

Best Buy: Best Buy and IKEA U.S. have partnered to pilot new in-store planning and shopping experiences that combine the latest and greatest major appliances from Best Buy with the well-designed, functional and affordable home furnishings from IKEA. This is the first time IKEA products and services will be accessible through another U.S. retailer, creating innovative ways for both retailers to meet customer needs in a rapidly changing environment.

“This partnership between IKEA and Best Buy is about making great design and functionality more accessible for the many,” said Rob Olson, chief operation officer, IKEA U.S. “By bringing together our home furnishing expertise, products, and services with Best Buy’s leadership in appliances and technology, we’re creating a one-stop destination where customers can design their dream kitchen, storage solutions or laundry space with ease. It’s a great step on our journey to helping people create beautiful, functional homes at a price they can afford.”

The new in-store collaboration will launch in 10 stores throughout Florida and Texas starting this fall, featuring 1,000-square-foot IKEA footprints that showcase inspirational kitchen and laundry room settings. These spaces are designed to inspire customers and help them create a cohesive, beautiful living space with the best high-tech appliances. At the IKEA in Best Buy experience, customers can also receive support from IKEA co-workers to plan and order home furnishing solutions and Best Buy’s blue shirts will also be in the store to provide advice on electronics.

LS Comment: Where is co-branding and product placement in new real estate development whether it be single family, multi-family, or office?

Costar: Adolfson & Peterson wrapped up partial demolition on the 1970s-era vintage buildings in the former Oak Lawn Design Plaza in Dallas that was once a seven building property in the Design District.

"We kept a portion of all the structures, but we are revising the sizes to feel like new space," Allison Pales, project manager with Adolfson & Peterson who is overseeing the work, told CoStar News. "The look will be completely different with a beautiful wood trellis system. Some of the buildings will be taller with more full-height windows and openings."

Completion of the redevelopment is expected in March 2026. Once completed, the property will offer nearly 50 spaces for retail, restaurants, wellness providers and showrooms.

Along with adding a new roof and replacing systems, the redevelopment plans include adding a new parapet and masonry facade and a storefront glass system.

Adolfson & Peterson started demolition on the project in March, more than a year after Asana Partners acquired the 160,000-square-foot property on a 9-acre site at 1444 Oak Lawn Ave. with plans to transform it into an open air upscale shopping and dining hub that is being called The Seam. GFF is the architect of record on the project that a state permit estimates will cost at least $27 million. New York City-based Morris Adjmi Architects is the design architect.

MA Founder and Principal Morris Adjmi said the firm's planning and design approach was centered on enhancing connectivity throughout the site and within the neighborhood and enhancing the pedestrian experience.

While active housing inventory is rising in most markets on a year-over-year basis, some markets still remain tight-ish (although it's loosening in those places too). As ResiClub has been documenting, both active resale and new homes for sale remain the most limited across huge swaths of the Midwest and Northeast. That’s where home sellers this spring had, relatively speaking, more power.

In contrast, active housing inventory for sale has neared or surpassed pre-pandemic 2019 levels in many parts of the Sun Belt and Mountain West, including metro area housing markets such as Punta Gorda and Austin. Many of these areas saw major price surges during the Pandemic Housing Boom, with home prices getting stretched compared to local incomes. As pandemic-driven domestic migration slowed and mortgage rates rose, markets like Tampa and Austin faced challenges, relying on local income levels to support frothy home prices.

This softening trend was accelerated further by an abundance of new home supply in the Sun Belt. Builders are often willing to lower prices or offer affordability incentives (if they have the margins to do so) to maintain sales in a shifted market, which also has a cooling effect on the resale market: Some buyers, who would have previously considered existing homes, are now opting for new homes with more favorable deals. That puts additional upward pressure on resale inventory.

In recent months, that softening has accelerated again in West Coast markets too—including much of California.

LS Commentary: We live in an experiential economy, in a social media driven economy, is this the optimal way to sell the dream?

Imagine: WIFE, look I found our dream house! Check out the tan house online!

Which one?

3295W. Oh wait maybe it was 2969W or 3094W

With AI, technology, are Builders maximizing selling design, differentiation and the American dream?

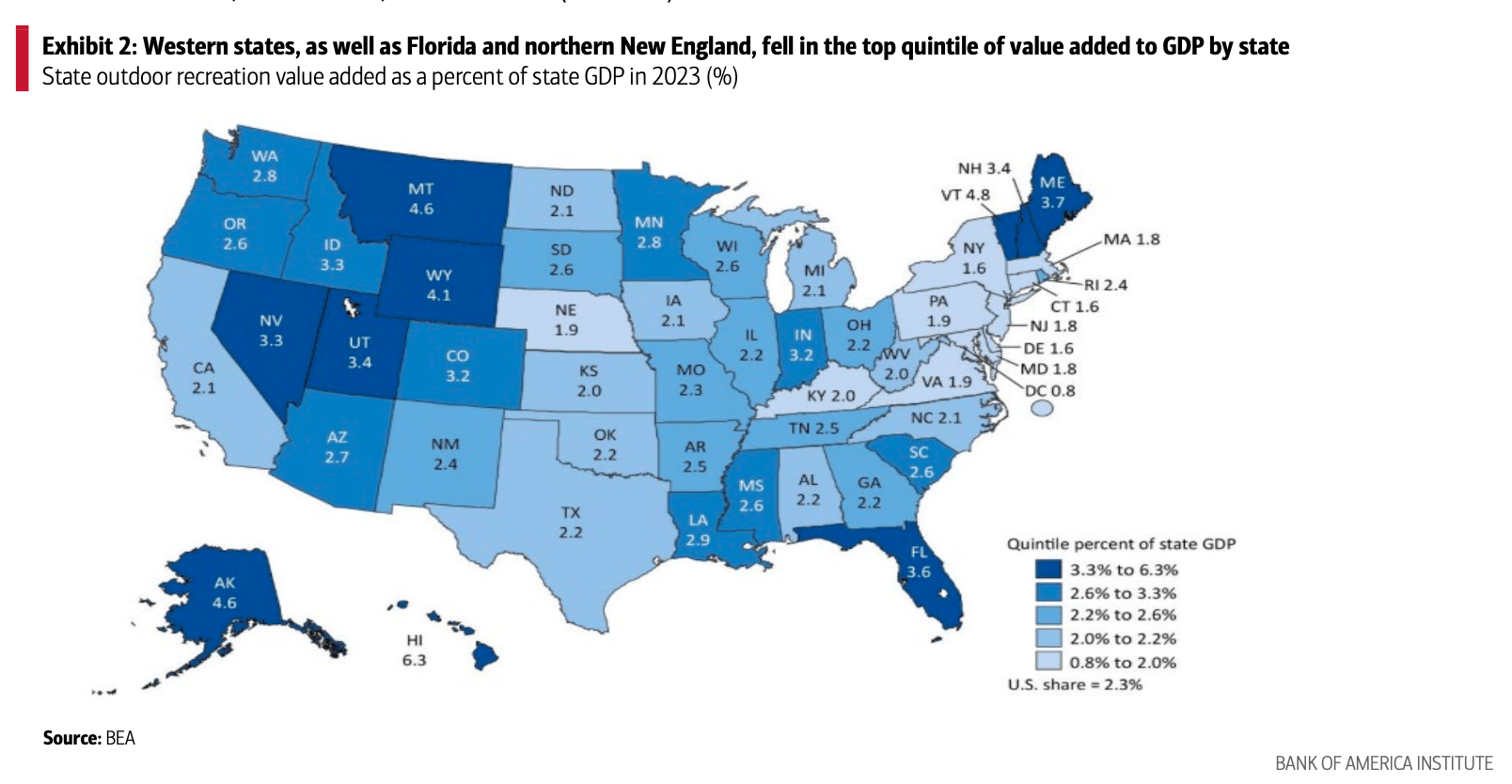

Outdoor activities are increasing in popularity, and, according to Bank of America aggregated credit and debit card data, spending growth on outdoor recreation has been performing better than that of indoor recreation for the past six months, the first consistent period of relative strength since early 2021.

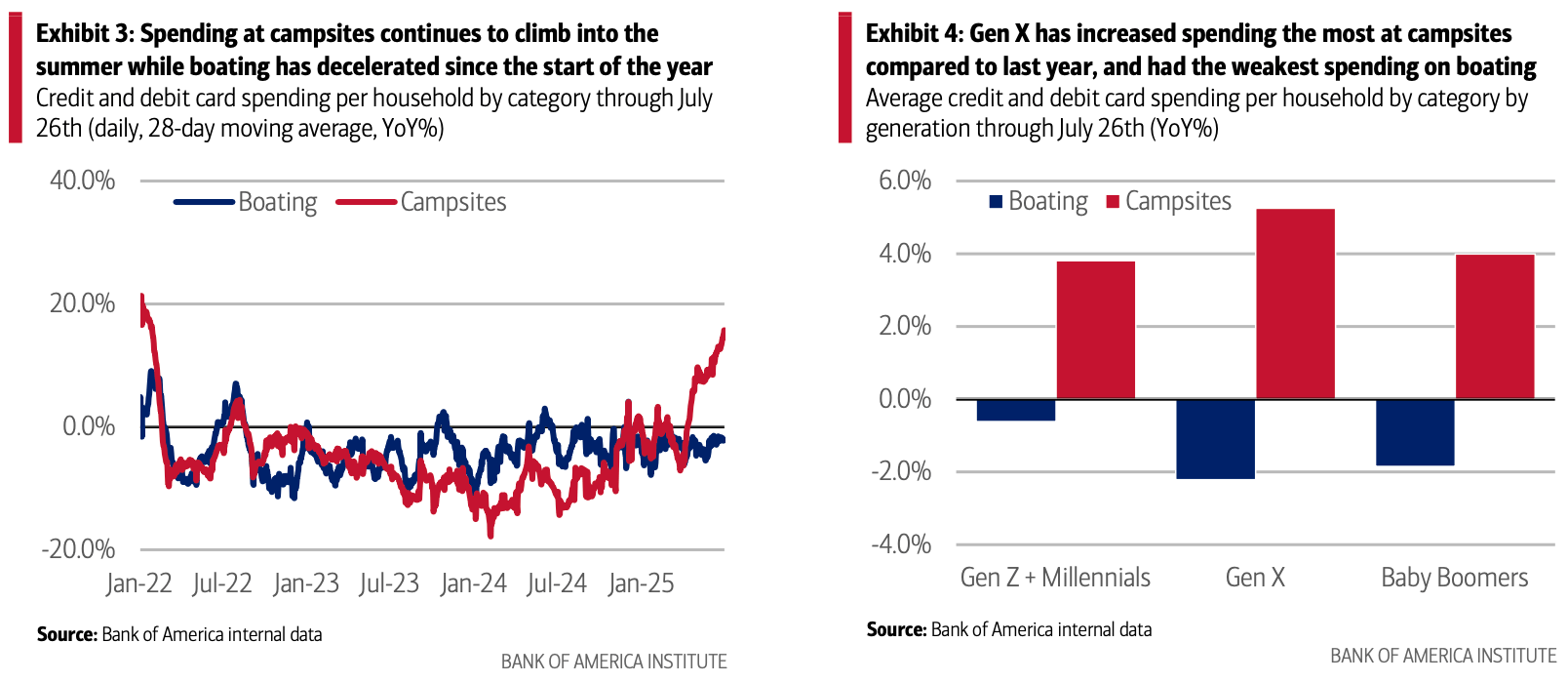

With these activities picking up in the summer months, we find boating spending growth has decelerated faster than last year, but spending growth at campsites reached the highest level since February 2022 - up 15.6% year-over-year in the week ending July 26th. Interestingly, Gen X had the strongest spending growth year-to-date at campsites, and the weakest on boating.

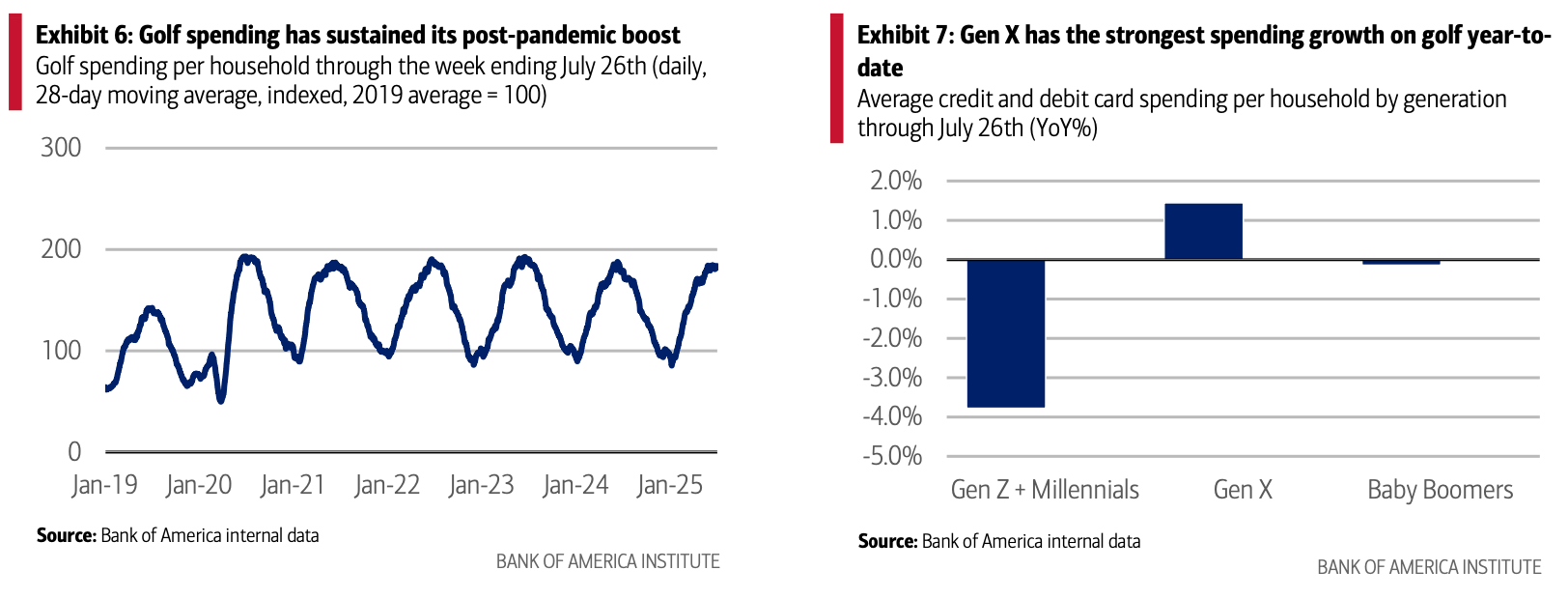

Golf is also on the summer upswing, with spending up more than 80% from the 2019 average level, according to Bank of America aggregated credit and debit card data. Gen X has been the primary driver of this growth, especially in the West. Plus, according to the National Golf Foundation, women and girls account for approximately 60% of the net gain in green grass golfers since 2019.

According to the BEA, outdoor recreation falls into three categories: 1) conventional activities such as boating and hiking; 2) other activities such as gardening and outdoor concerts; and 3) supporting activities such as construction, travel and tourism, and government expenditures. Across the country, value added for outdoor recreation as a share of state GDP ranged from a high of 6.3% in Hawaii to 1.6% each in Delaware, Connecticut, and New York