- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 08.09.2025

Location Strategy Chartbook 08.09.2025

Real Estate Market Insights

The Trump administration is preparing to sell stock in mortgage giants Fannie Mae and Freddie Mac in an offering that could raise approximately $30 billion and begin later this year.

According to a report from the Wall Street Journal, citing people familiar with the matter, administration officials are discussing plans that could value the combined companies at roughly $500 billion or more. The offering would involve selling between 5% and 15% of their stock.

Officials are still debating whether the mortgage giants would go public as a single company or as two separate entities.

Brandon Roth, IPA: Last Wednesday, Jerome Powell held a press conference where he said:"...there's also a downside risk to the labor market. In coming months, we'll receive a good amount of data that will help inform our assessment of the balance of risks and the appropriate setting of the federal funds rate"

Two days later, payroll data was released showing:

July payrolls rose just 73K, missing expectations of 110K.

May and June were revised downward by 258K jobs.

The 5-year treasury yield declined nearly 20 bps within 15 minutes of the jobs data being released.

In addition, the market's expectation for a 25-bp rate cut at the next Fed meeting increased from 38% a week ago to 91% today.

The chart below compares today's forward SOFR curve versus one week ago. The market is now projecting SOFR to decline ~50 bps to 3.75% by the end of the year.

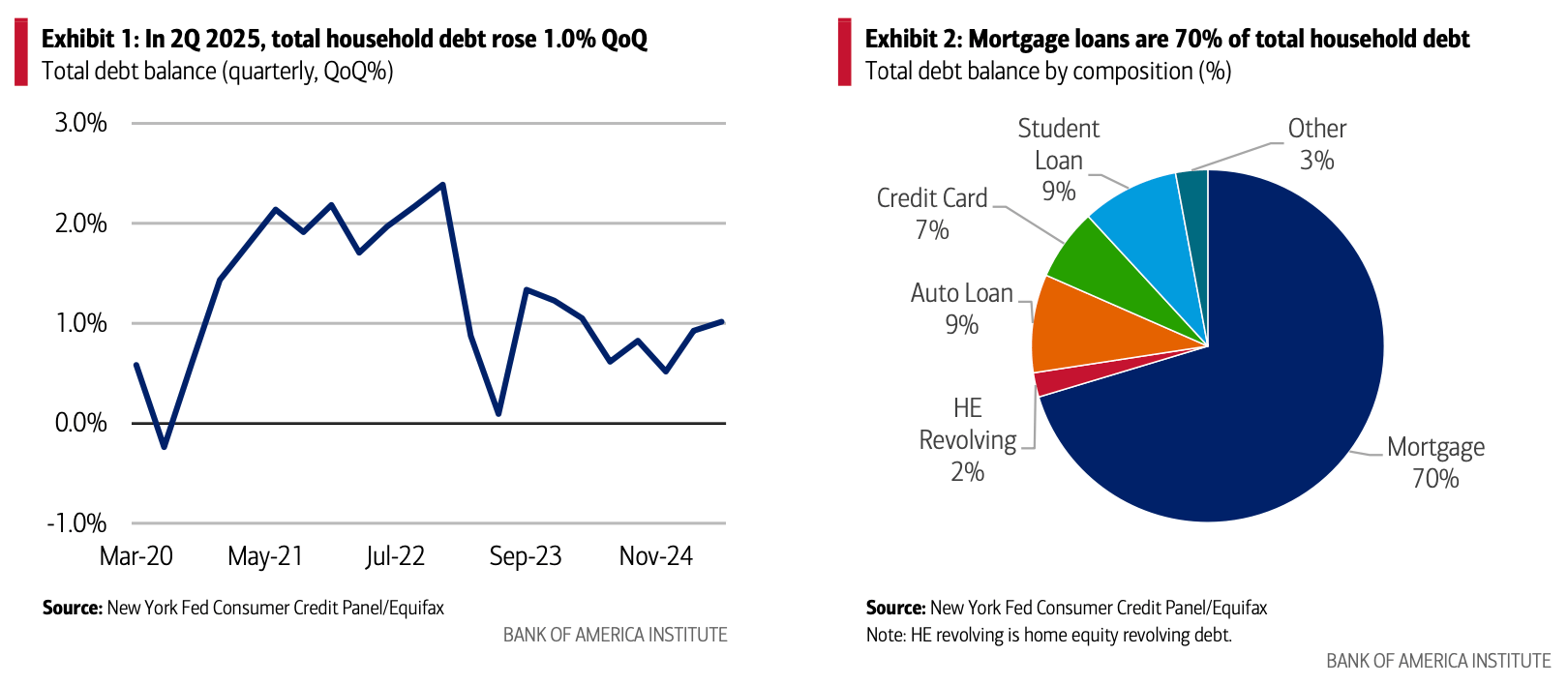

Americans are inching further into debt, with debt levels up 1.0% quarter-over-quarter (QoQ) in 2Q 2025. Total household debt increased by $185 billion to hit $18.39 trillion in the second quarter, according to the latest New York Fed Quarterly Report on Household Debt and Credit.

Looking by composition, the greatest share of total debt is held by those with mortgages. According to the New York Fed, mortgage balances grew by $131 billion and totaled $12.94 trillion at the end of June. And in the second quarter, mortgage balances grew 1.0% QoQ - less than credit cards (2.3% QoQ) but greater than auto loans (0.8% QoQ).

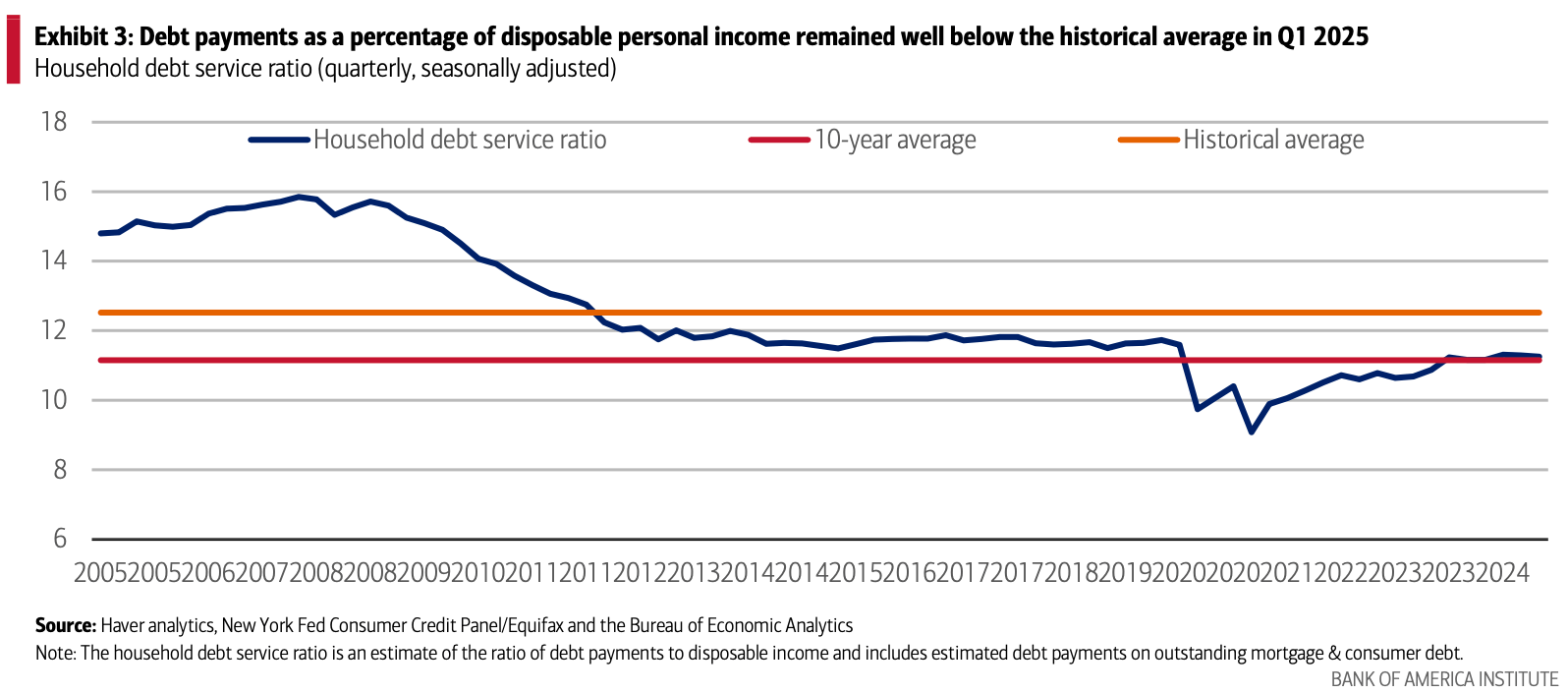

The good news is the ratio of household debt payments to disposable personal income dropped to 11.25 in Q1 2025 from 11.29 in Q4 2024 and remains below the historical average of 12.52, suggesting to us there is some room for consumers to increase borrowing, so long as the labor market holds up. Plus, household debt to GDP has been steadily declining in recent years, meaning the debt service ratio is increasing primarily due to the rise in interest rates, according to BofA Global Research

According to third-party loan account data, in June, the average mortgage loan balance was almost 32% above the 2019 average. Note that this data is representative of overall industry loans, and not specifically mortgage loans issued by Bank of America. While the rate of acceleration has slowed, the increased payment level could pose cost pressures for some homeowners.

Since the post-pandemic housing boom, homebuyers have taken out larger mortgages amid rising home prices, and for some, it has now become harder to keep up with those payments. And according to BofA Global Research, the challenge is most acute for those who got mortgages in the past couple of years at high home prices and high mortgage rates, especially lower-income Federal Housing Administration borrowers.

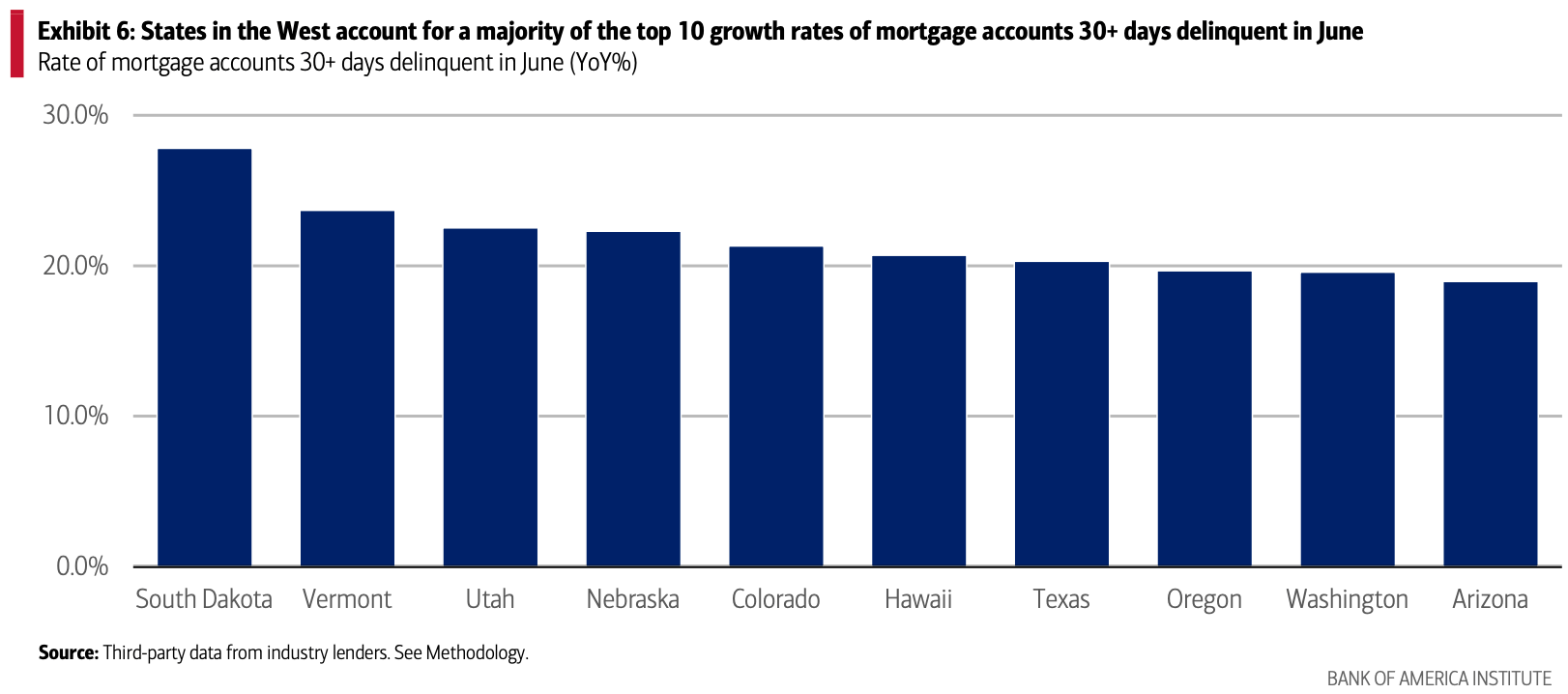

According to third-party data on industry loan account trends, the rate of mortgages 60-149 days past due was up 21.3% YoY in June, having come down significantly from September 2024’s peak of more than 33% YoY.

The delinquency rate for home loans on one-to-four-unit residential properties increased to a seasonally adjusted rate of 4.04% of all loans outstanding at the end of the first quarter of 2025, according to the Mortgage Bankers Association’s (MBA) National Delinquency Survey. Still, overall national delinquency and foreclosure rates remain below historical averages, though some households are clearly feeling more financial pressures.

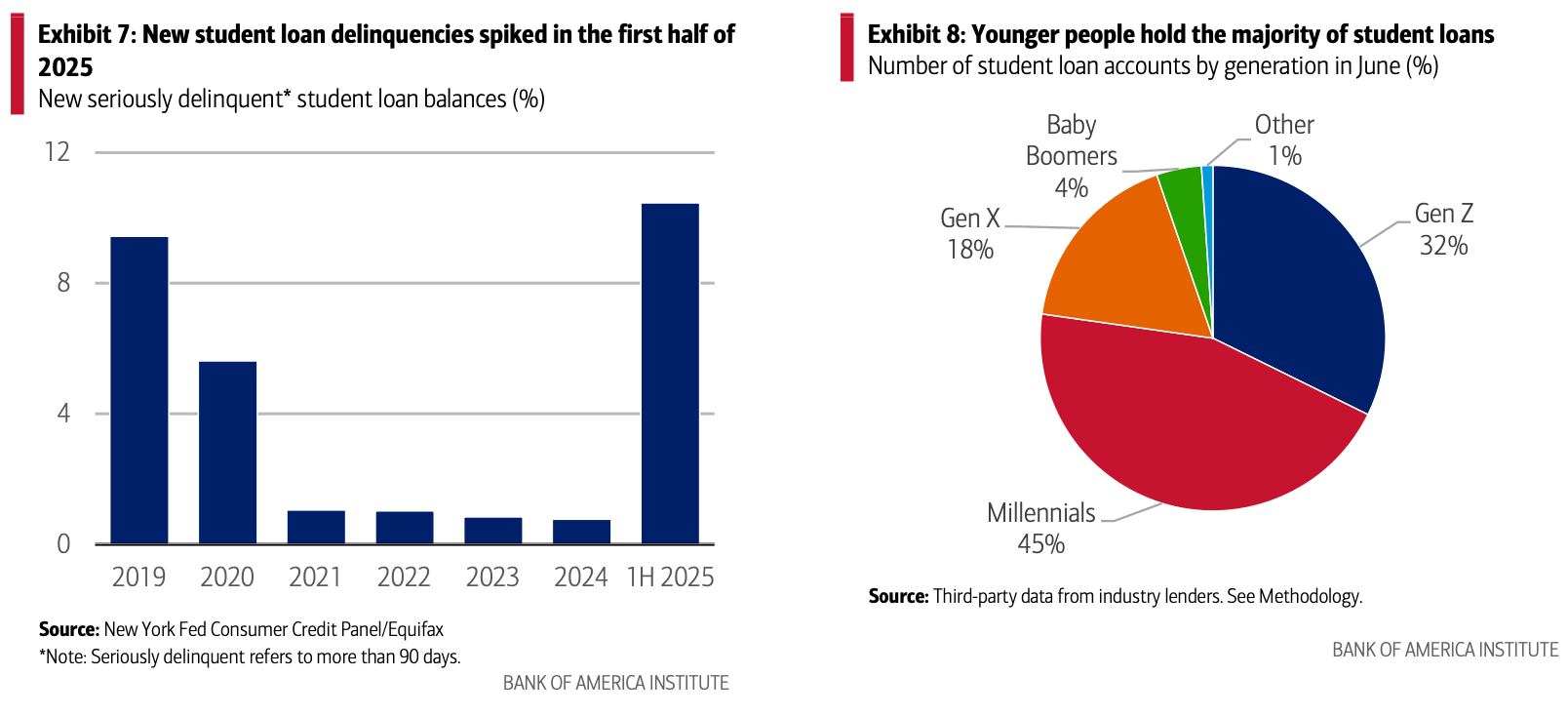

One of the most notable jumps in the data within the Household Debt and Credit reports so far this year was in student loan balances which edged up by $7 billion and stood at $1.64 trillion in the second quarter of the 2025. Markedly, the data also shows a large uptick in balances that went from current to delinquent, primarily due to the resumption of student loans being included in credit reports after a nearly five-year pause. Note that this data is inclusive of student loan accounts across the industry.

Although Gen Z and Millennials make up more than three-quarters of student loan holders, the majority of those student loan holders who became seriously delinquent, or 90 or more days past due, in Q2 2025 were age 50+, according to the New York Fed. This could put additional pressure on card spending, especially among Gen Xers, whose overall spending growth has been weaker than Baby Boomers and Traditionalists

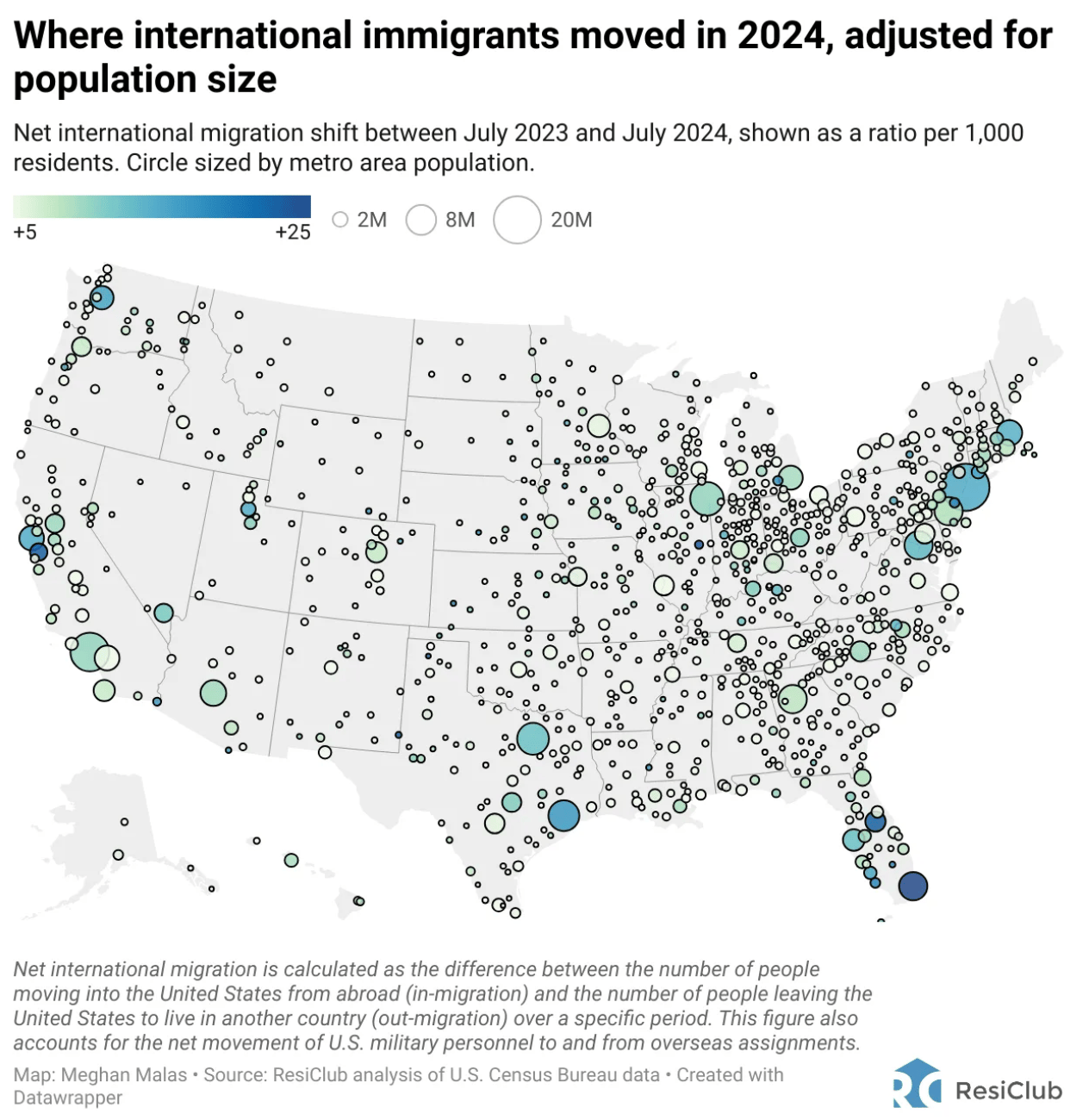

Between summer 2021 and summer 2024, the U.S. saw a substantial upswing in net international migration—much of it coming through the Southern Border. As of July 2024, the U.S. population stood at 340.1 million, up 3.3 million from 336.8 million in July 2023. Of that population increase, 2.8 million (or 85%) came from net international migration. That international migration burst, of course, is behind us now. Recently, border crossings have plummeted. The updated forecast by researchers at AEI expects that net international migration in 2025 will be somewhere between +115,000 and -525,000.

What does this international migration slump mean for the U.S. housing market? All else being equal, an immediate and direct housing impact of fewer immigrants coming through the Southern Border, in my view, is lower aggregate rental demand—specifically at the lower end of the market—than if that burst had continued.

Rental markets likely to see the biggest impact are in metro areas that have experienced the most international immigration in recent years.

In particular, major markets such as New York City, Miami, and Houston could feel the greatest effects.

Many economists, including those at the AEI Housing Center, believe this pullback in international migration could dampen U.S. total employment growth and reduce overall U.S. economic activity. Heading into 2025, many analysts speculated that it—a sharp pullback in immigration through the Southern Border—would quickly put upward pressure on builders labor costs; however, so far, dampened residential construction activity has more than outweighed any of those pressures.

"Labor also seems to be more available in our markets potentially stemming from slower multifamily construction and reduced starts in the industry." Hilla Sferruzza, CFO of Meritage Homes, said during the builder’s July 24, 2025 earnings call

“From labor availability, it's plentiful. We have the labor that we need. Our trades are looking for work. And that's why you've seen sequential and year-over-year reduction in our cycle time. Because we have the support we need to get our homes built. And, you know, given those efficiencies, reductions in stick and brick [costs] over time. Some of that is from design. And efficiency of the product that we're putting in the field. And some of that is just from the efficiency of our operations.” D.R. Horton CEO Paul Romanowski said during their earnings call on July 22, 2025

Brad Hargreaves, Thesis Driven: 1,500 families signed up for The Beginning Clubhouse before they even opened the doors. While Soho House kicks kids out at 6pm, these founders are building a club exclusively for families. Here's how they're creating a category that didn't exist in NYC:

Soho House kicks kids out at 6pm

Country clubs optimize for childless professionals

"Family spaces" are either Chuck E. Cheese chaos or sterile community centers

The problem is simple: Modern families already spend $2,400/month on fragmented services:

Boutique gyms '

Co-working

Childcare

But there's nowhere that everyone's actually happy for 3+ hours.

60% of private clubs report net-new member growth since 2022.

Enter The Beginning: A 45,000 sq ft family club opening summer 2026 in Brooklyn Heights.

The founders aren't just building a business. They're local parents solving their own problems.

50 Columbia Heights, originally built- in 1924 spans seven floors with view of the Manhattan skyline and is walking distance to Brooklyn Bridge Park.

~$400/month for adults

~$200/month per child

Target capacity: 1,500 families

They hit that number in pre-registrations alone

The market gap: Traditional hospitality real estate completely ignores families with money.

This isn't just another club.

It's infrastructure for a lifestyle that doesn't exist yet.

The Radical Play Concept Partners have proven the need with a similar project based in Dallas.

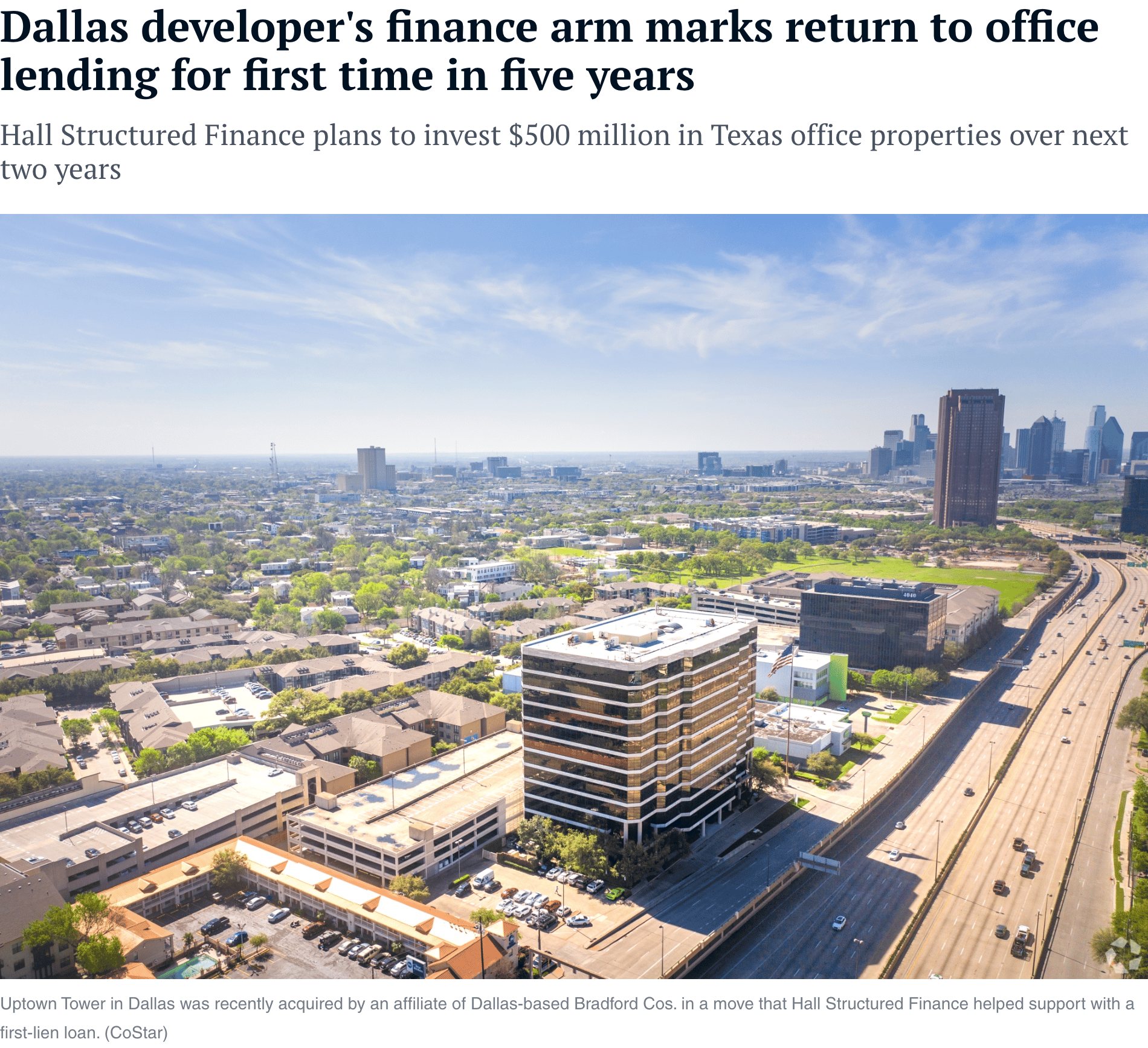

Hall's finance arm, Hall Structured Finance, made a first-lien loan for $30.8 million to an affiliate of Dallas-based Bradford Cos. that recently acquired Uptown Tower, a 12-story, nearly 254,000-square-foot office building at 4144 N. Central Expressway in Dallas. In recent years, Hall Structured Finance has backed apartment and hotel properties, but now office is part of its business with the 1980s-vintage property being the first of many more office investments planned by the firm.

Bradford Cos. is planning to renovate Uptown Tower with upgrades that include a new first-floor lobby, fitness center, new common areas and garage access controls.

"The market is still pretty capital-constrained, and a lot of lenders are understandably on the sidelines," Hall, founder and CEO of Hall Group, the parent company of Hall Structured Finance, told CoStar News. "A lot of lenders have a problem with office deals. We stayed out of the market when we thought a lot of things had changed" about the office sector after the onset of the pandemic.

"I think now there's clarity," he added. "I wouldn't say that all office is coming back, because I don't believe that is what's going to happen, but I do think well-located properties that have good amenities are absolutely going to be ... in really good shape" over the next two to three years, Hall said.

Hall Structured Finance is expecting to invest at least $500 million in the next two years in both new and value-add office properties in Texas markets, with the Dallas area expected to land some of those deals.

"We have a couple of sizeable new construction deals that we are discussing in Dallas," Hall said.

The return to lending on office properties comes months after Hall Group opened The Tower at Hall Park at a 162-acre, 15-building development in Frisco, Texas. The 16-story office property with leases in tow from Chobani and the Frisco Economic Development Corp. recently landed a 10-year lease from Brightline Dealer Advisors for just over 10,000 square feet. The insurance agency expects to move into its new space in November.

At Hall Park, Hall said his team pivoted from having an office park with 2.2 million square feet of office space to a mixed-use hub with a focus on amenities. That focus continues today, he said.

"Our job is no longer about physical space alone," Hall said. "At Hall Park, we are thinking about how we can improve our services and how can we help tenants recruit and retain employees."