- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 08.16.2025

Location Strategy Chartbook 08.16.2025

Real Estate Market Insights

Underlying US inflation accelerated in July, though the cost of tariff-exposed goods didn’t rise as much as feared, boosting expectations that Federal Reserve officials will lower interest rates when they meet next month. The core consumer price index, which excludes the often volatile food and energy categories, increased 0.3% from June, the strongest pace since the start of the year.

Bloomberg: We’re long past the days when Americans, buoyed by extra savings and pandemic-era stimulus checks, were spending on restaurant meals with abandon after being cooped up for months. Now, chains including McDonald’s, Wendy’s and Sweetgreen are warning that people are being far more cautious with their money. When that’s the case, one of the easiest things for them to cut is that morning McGriddle or Egg McMuffin. Breakfast is “absolutely the weakest” mealtime in terms of sales, McDonald’s Chief Executive Officer Chris Kempczinski said last week.

The reasons are simple. “When consumer uncertainty increases and consumers choose to eat another meal at home, breakfast is often the first place that they do that with,” Ken Cook, Wendy’s interim CEO, said. It’s not that hard—or expensive—to buy a store-brand cereal and some milk and call it a day. (The inflation data released Tuesday shows the cost of food away from home rose 0.3% in June, while grocery costs fell 0.1%.)

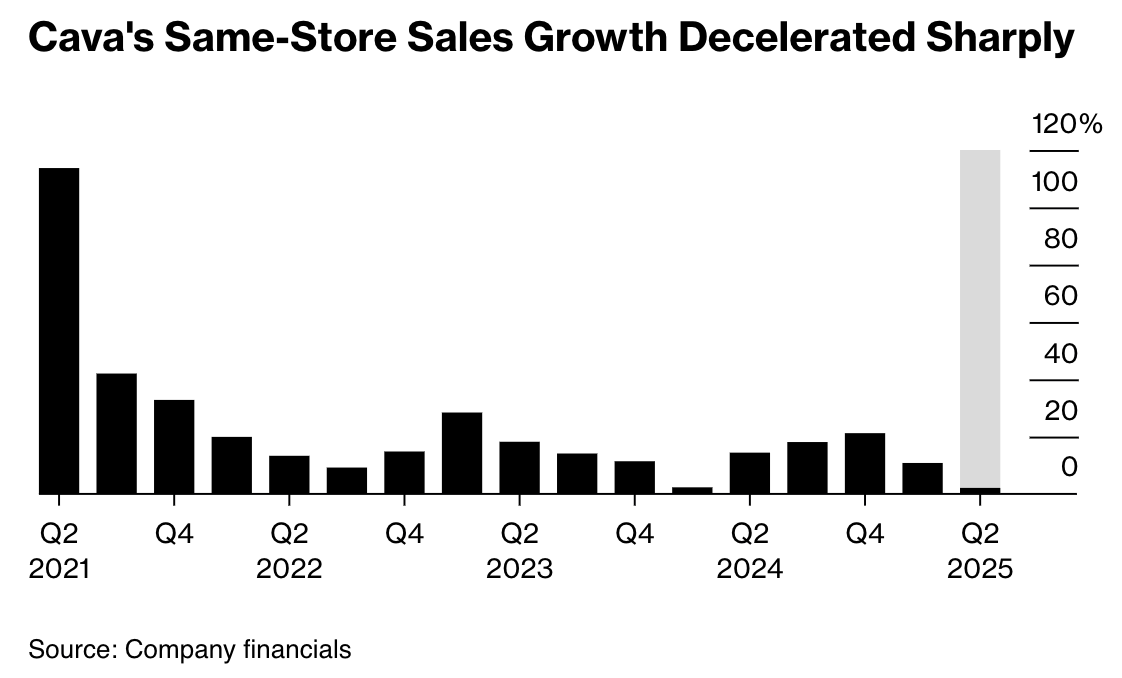

Cava Group Inc. trimmed its annual sales outlook after a sharp deceleration in the second quarter as skittish diners spent less on restaurant meals, showing the pressure the brand is facing to keep up with its speedy growth in recent years.

Sales at established restaurants rose 2.1% for the quarter, growth that stands out against competitors such as Sweetgreen Inc. and Chipotle Mexican Grill Inc., which experienced slumps they’ve attributed to a shaky economy. Still, the marked annual outlook slowdown illustrates how difficult it is for restaurant chains to break through as Americans fretting about inflation and tariffs scrutinize their restaurant outings.

More data from the government shows inflation reigniting because of the US trade war. Wholesale inflation accelerated in July by the most in three years, suggesting companies are passing along higher import costs related to tariffs. Simultaneously, applications for US unemployment benefits edged lower last week, suggesting employers may be reluctant to fire workers.

The producer price index increased 0.9% from a month earlier, the largest advance since pandemic consumer inflation peaked in June 2022, according to a report from the Bureau of Labor Statistics

The PPI rose 3.3% from a year ago. The BLS report could indicate companies are adjusting their pricing of goods and services to help offset costs associated with higher levies, despite the softening of demand in the first half of the year. Treasuries fell on news of the data, and the latest record-breaking rally in US stocks lost steam

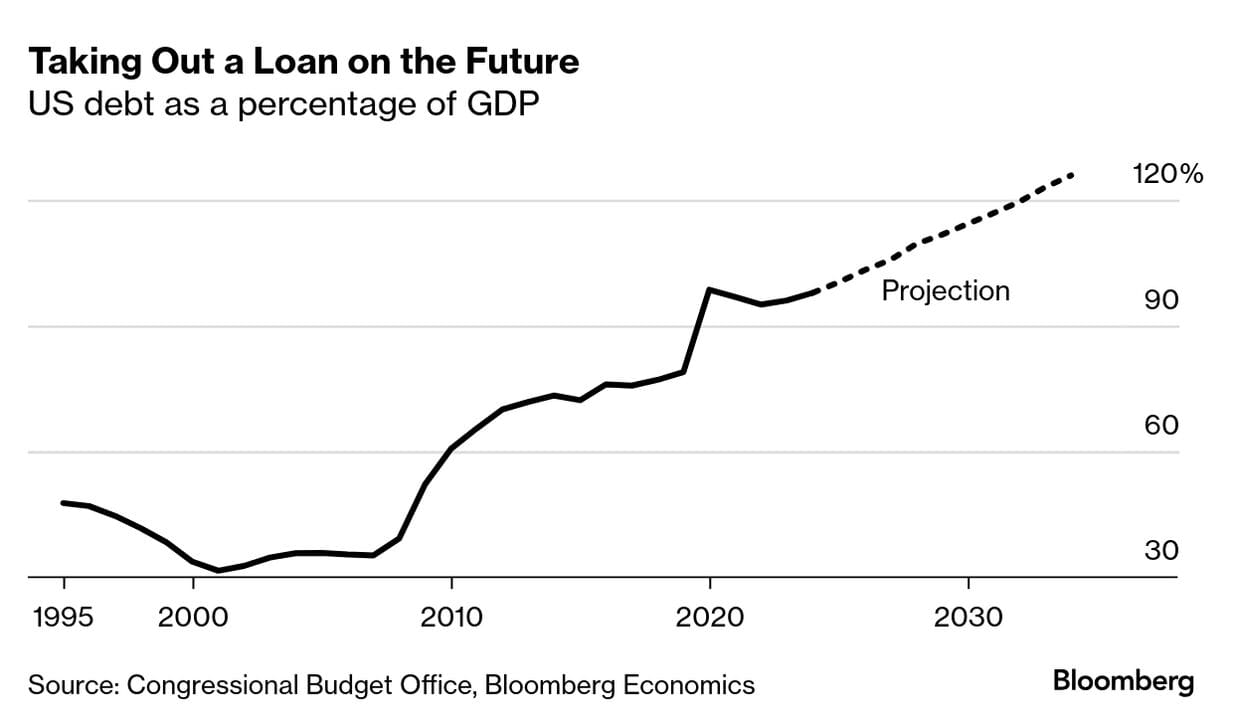

It’s a cliché to wail, “Who will think of the children?” But honestly: Will anyone? The CBO projects the debt could be almost double the size of the GDP by 2050, with a third of every tax dollar going to paying interest. Such massive debt payments would seriously constrain future legislators, hamstringing their ability to respond to a crisis. It could also crowd out private borrowing, propel interest rates higher and push homeownership further out of reach for young people who’ve already weathered a financial crisis and pandemic and will have to load up on debt to pay for college. “Deficits don’t seem to matter until all of a sudden they do, and then they are going to matter a whole lot” as investors get nervous and capital flees, says Elizabeth Popp Berman, a professor of organizational studies at the University of Michigan and author of Thinking Like an Economist.

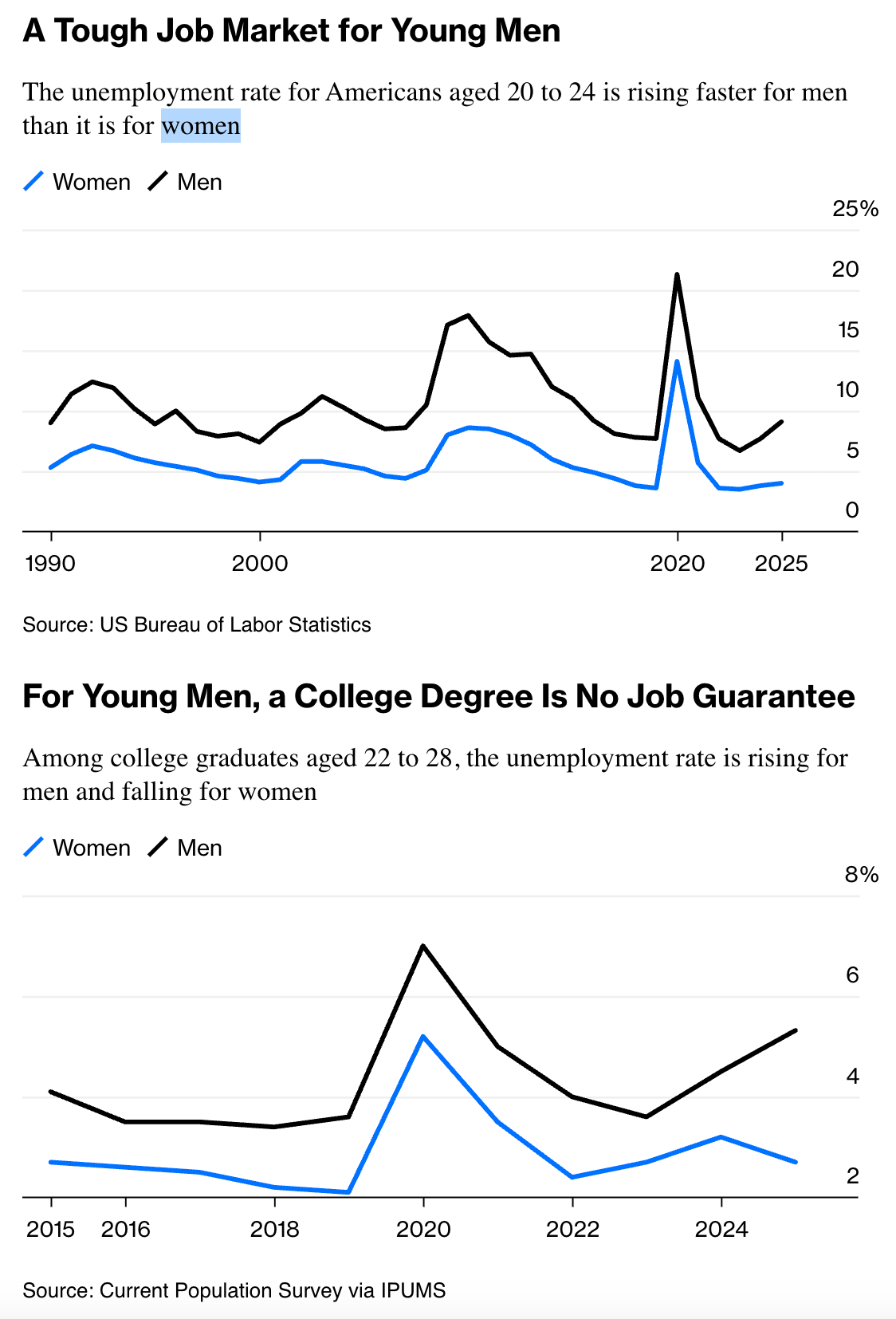

Despite all the drama about the weakening jobs numbers, the US labor market is actually doing OK. There is one major exception, however: if you happen to be a young man. While the overall unemployment rate was still a respectable 4.2% in July, for young men aged 20 to 24, it was 8.3%, which is near recession levels — and for recent college graduates, the annual rate is 5.3%. Both of these numbers are about double the comparable figures for young women. During the pandemic, the economy was so bad for working women that it inspired the term “she-cession.” Could the US now be headed for a “he-cession”?

The job market is weakening, which tends to affect men and young people first. Men tend to work in jobs more sensitive to the business cycle, such as construction or manufacturing, while women work in more impervious sectors such as health care or education.

Younger workers also tend to be the first laid off (or not hired at all) when the economy starts to turn. But the data suggest that something deeper is happening.

The unemployment rate for recent male college graduates who work in retail is at 8.2%, for example, and is just 4.7% for women. Most of the unemployment is among those who work in department stores or restaurants. Meanwhile, unemployment rates remain low for men in manufacturing (under 4%) and elevated but not recession-level in construction (6%).

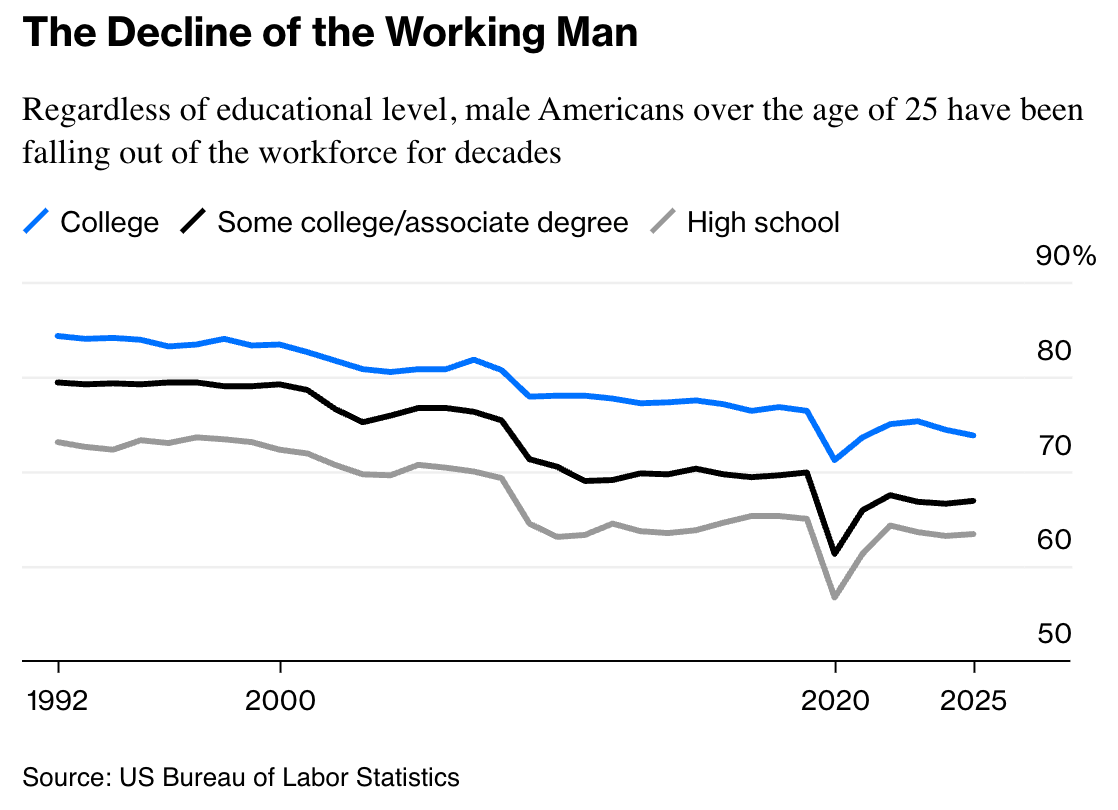

Men have dominated the labor market for most of the modern era, and still earn more than women, but the jobs market has not been kind to men for the last few decades. Many men, even in the prime of their lives, aren’t working. And going to college is no longer an automatic way to improve your job prospects

Mortgage Bankers Association: In Q2 2025, compared to a year earlier, a rise in originations for office, health care, and industrial properties led to an overall increase in commercial/multifamily lending volumes. There was a 140 percent year- over-year increase in the dollar volume of loans for office properties, a 77 percent increase for health care properties, a 53 percent increase for industrial properties, and a 30 percent increase for retail properties.

Originations for multifamily properties decreased 35 percent, and hotel property loan originations decreased 30 percent compared to the second quarter of 2024. Among investor types, the dollar volume of loans originated for depositories increased by 108 percent year-over-year. There was a 93 percent increase in loans for investor-driven lenders, a 72 percent increase in loans for life insurance companies, a 59 percent increase in government sponsored enterprises (GSEs – Fannie Mae and Freddie Mac) loans, and a 10 percent decrease in commercial mortgage-backed securities (CMBS) loans.

Seven major special servicers manage $50.6 billion in distressed commercial mortgage-backed securities loans across more than 1,600 properties, with office buildings representing the largest exposure, according to a CoStar News analysis of Morningstar Credit data.

As of Tuesday, the seven firms controlled 75% of the total $67.6 billion in specially serviced loans, while more than 28 firms managed the remaining 25%. Loans in special servicing typically indicate an issue the borrower has with making payments.

KeyCorp Real Estate Capital Markets services 394 loans valued at $12.2 billion, the most of any servicer, Morningstar data shows. Rialto Capital Advisors is next with 396 loans valued at $10 billion, followed by LNR Securities Holdings with 341 loans valued at $8.9 billion.

Four of the seven servicers had the largest loan balances on office properties. Rialto holds $3.8 billion in office loans across 126 properties, while LNR manages $4.3 billion in office assets across 125 loans. Situs Holdings carries $1.8 billion in office exposure despite managing only 10 such loans, indicating significantly larger individual deal sizes.

Multifamily properties represented the second-largest exposure on Morningstar’s list. KeyCorp services 313 multifamily loans totaling $2 billion, while CWCapital Asset Management has the highest concentration in this sector, with 162 multifamily loans out of its 244 loans.

Among firms servicing loans backed by retail properties, Green Loan Services is the smallest firm by loan count with 13 loans. It carries $1.9 billion in exposure across only two properties, also signaling a preference for big property deals.

CWCapital Asset Management, managing 244 loans totaling $6 billion, maintained the most balanced portfolio composition. The firm’s largest single exposure was the multifamily sector, at $1.9 billion, followed by office loans, at $1.5 billion.

Lodging properties, particularly hurt by pandemic-related disruptions, appeared across most servicer portfolios. KeyCorp holds $2.6 billion in lodging loans across 11 properties, while LNR manages $1.1 billion in hotel assets.

Midland Loan Services rounds out the group, servicing 117 loans totaling $4.7 billion. Debt backing mixed-use and office properties each amounted to more than $1 billion.

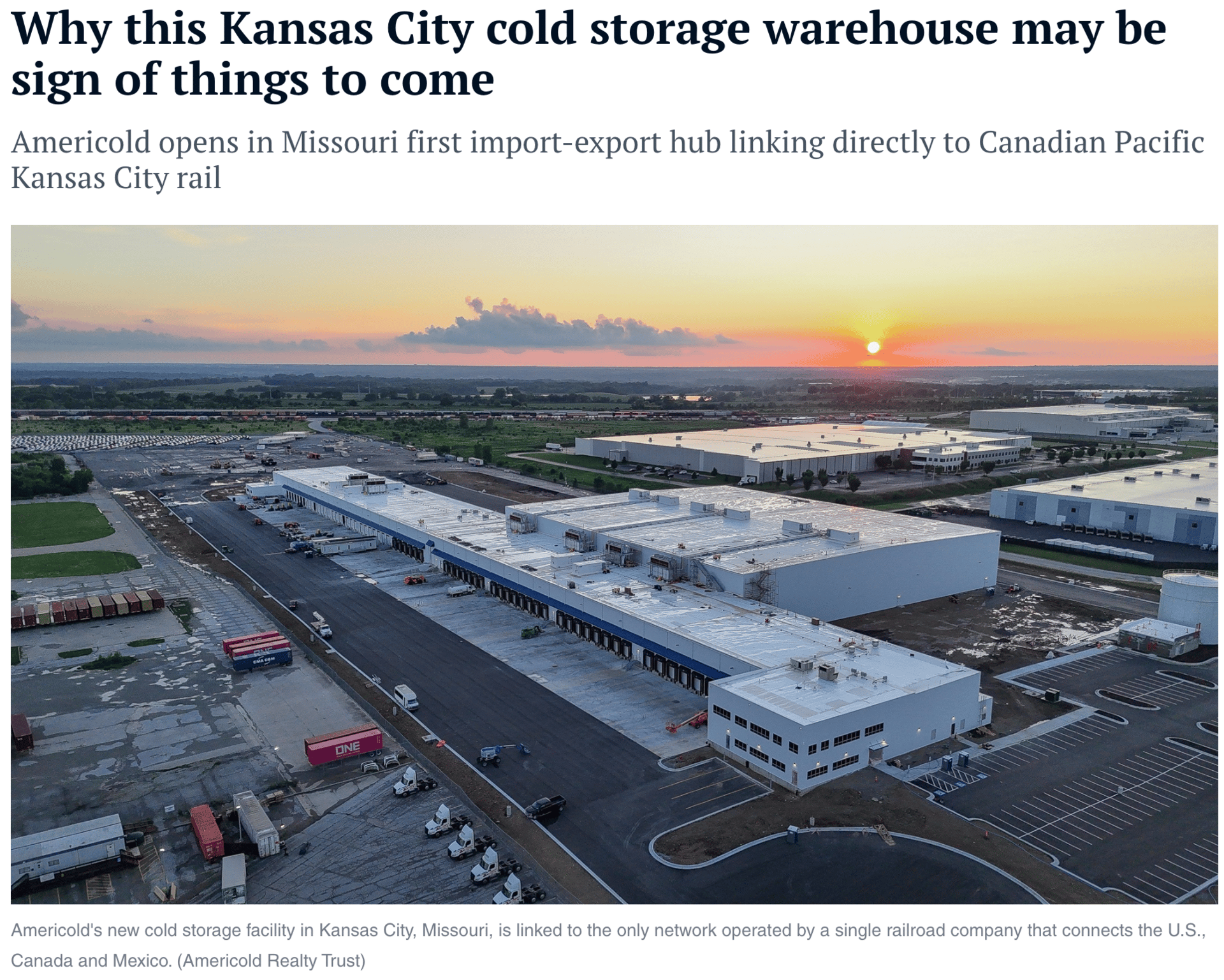

A new warehouse in Kansas City, Missouri, that opened this month is doing more than holding chilled and frozen food. I

The warehouse was developed by Americold Realty Trust, a real estate investment trust that specializes in cold storage facilities, in a partnership with railway Canadian Pacific Kansas City. The property is Americold’s first import-export hub with a direct link to CPKC, the only rail network run by a single company that connects Canada, the United States and Mexico.

The creation of a cross-continental network, operated by a single railroad, with these kinds of warehouses is critical for shippers, said Rich Thompson, international director of supply chain and logistics solutions at property services firm JLL.

Union Pacific said last month it agreed to buy Norfolk Southern for $85 billion. The deal requires regulatory approval and is expected to close by early 2027.

Freight trains provide a viable option that, as of now, some real estate professionals consider underutilized. Trucks control about 85% of all freight movements worldwide, and commercial truck crossings at U.S.-Mexico border ports reached record levels in 2024 — and are on pace to match or break those records this year, according to a new report from brokerage Marcus & Millichap.

But trains can move large quantities of heavy goods much more efficiently than trucks, according to LJA Engineering, a Houston-based consulting firm that works on transportation real estate developments.

Americold’s new $127 million cold storage warehouse is near the Centerpoint Intermodal Center in South Kansas City. It features on-site food inspections by the U.S. Department of Agriculture to eliminate delays at the Canadian and Mexican borders, according to Americold.

It holds strategic importance for CPKC’s Mexico Midwest Express as the only single-line rail service for refrigerated goods between the U.S. and Mexico, Americold said.

The Kansas City property is the first of several chilled import-export hubs that Americold plans to build across North America with direct links to railroad networks. The Atlanta-based REIT declined to identify potential locations but said it is looking at western Canada and Mexico.

The new breed of logistics properties, such as Americold’s 335,000-square-foot property, “have evolved from simple loading docks to sophisticated hubs, which can include automated handling equipment and advanced management systems,” according to LJA. LJA was not involved with Americold’s new facility in Kansas City.

“By positioning these facilities near population centers, civil engineers can seamlessly merge rail and … trucking to provide targeted distribution flexibility,” LJA said.

Between 2019 and 2024, insurance expenses per hotel key surged to an average of 195% across the nation’s top 25 markets, reflecting a convergence of structural pressures rather than simple rate adjustments. The spike has been fueled first and foremost by escalating climate-related risks.

Hurricanes, floods, wildfires and severe storms are not only more frequent but also more destructive than in years past. Insurers have responded by repricing exposure, particularly in coastal and high-fire-risk states, where catastrophic loss potential is rising sharply.

Compounding the issue, replacement costs for damaged properties have soared as labor shortages, supply-chain disruptions and construction-material inflation drive rebuilding expenses far beyond pre-pandemic levels. Because insurers calculate premiums based on the cost to restore a property, even inland markets with less-direct climate exposure have seen substantial increases.

Topping the list in 2024 was Miami, where insurance costs reached an unprecedented $361 per key on an annual basis, up 189% since 2019, making it the priciest hotel market for coverage in the country. Hawaii's Oahu Island followed at $307 per key and a 193% increase from 2019, reflecting continued vulnerability to climate and natural disaster risks. San Francisco-San Mateo ranked third at $260 per key (up 178%), where high replacement costs and urban risk factors keep premiums elevated.

Many carriers have scaled back coverage, reduced policy limits or exited certain high-risk regions altogether, shrinking the pool of available providers. With fewer competitors in the market, pricing power has shifted toward insurers, leaving hotels — particularly independents and smaller portfolios — with limited negotiating leverage.

Legal and regulatory environments are also adding to costs. Increased claims litigation, evolving building codes and heightened environmental compliance standards have raised insurers’ operating expenses, much of which is passed directly to policyholders.

Markets like Miami, San Diego and New Orleans are now managing insurance premiums that have nearly doubled or tripled in just five years. As revenue growth moderates in many cities, hoteliers are exploring higher deductibles, risk-pooling arrangements and capital improvements in resilience to help offset the mounting burden of insuring their properties in an era of heightened uncertainty.