- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 08.23.2025

Location Strategy Chartbook 08.23.2025

Real Estate Market Insights

WSJ: Federal Reserve Chair Jerome Powell opened the door for rate cuts next month when he said the labor market might be softening enough to rein in inflation that is being pushed up by tariffs.

“The balance of risks appears to be shifting,” Powell said. While labor markets appear to be stable, “it is a curious kind of balance that results from a marked slowing in both the supply of and demand for workers.” That has led to an “unusual situation” in which the risks of worse-than-expected labor-market outcomes are rising, he said. “And if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment,” Powell said. The still-restrictive interest-rate stance amid a changing economic outlook “may warrant adjusting our policy stance,” he said.

He also suggested that a so-called neutral setting for interest rates—or the level that neither spurs nor slows economic activity—might be higher than it was last decade. The Fed’s benchmark rate is currently around 4.3%.

Powell said the effects that tariffs are having on consumer prices “are now clearly visible” and are expected to accumulate in the months ahead. The question for the Fed is whether those price increases will “materially raise the risk of an ongoing inflation problem.

Powell for the first time suggested somewhat greater confidence in a base-case forecast that the effects of higher goods prices due to tariffs would be relatively short-lived. He cautioned that a “one-time” increase in prices didn’t necessarily mean “all at once” because it will take time for tariff increases to filter through supply chains, he said. Powell said it was possible, however, that tariffs-driven cost increases could spur a more lasting inflation problem, for example, if workers who see their inflation-adjusted incomes falling are able to secure higher wages from employers. “Given that the labor market is not particularly tight and faces increasing downside risks, that outcome does not seem likely,” he said. He said the central bank would also remain highly focused on ensuring that measures of consumers’ and businesses’ expectations of future inflation didn’t climb. Many economists and central bankers believe those higher inflation expectations can be self-fulfilling. “Come what may, we will not allow a one-time increase in the price level to become an ongoing inflation problem,” he said.

Markets cheered Powell’s speech, which blessed investor expectations of a September rate cut that had accumulated after disappointing downward revisions to payroll gains earlier this month.

Barron’s

It’s been a tough time for the private equity industry. Three years in the deal desert has firms ginning up new ways to get cash into the hands of investors. They’ve taken out loans against their portfolio of companies. They’ve moved those they couldn’t or didn’t want to sell into so-called continuation vehicles, an asset-shuffling technique that allows them to hold investments for longer. They’ve even rolled over some of those assets into another newfangled vehicle known as CV-squared. The tactics underscore the increasing use of financial engineering by an industry struggling to return cash to investors. And now, they’re getting even craftier.

Firms including Bain Capital and Leonard Green & Partners have started using commitments to continuation funds as collateral, giving them another way to borrow money. Meanwhile, KKR & Co. and Goldman Sachs Group Inc. are pitching complex financings that would allow them to move private equity assets into special funds, without crystallizing losses that typically come from selling such investments at a discount. All of the firms declined to comment. The tactics underscore the increasing use of financial engineering by an industry struggling to return cash to investors. Distributions as a percentage of net asset value tumbled to 11% last year from an average of 29% a decade earlier, according to a Bain & Co. report.

WSJ: In May, Home Depot executives told investors that they plan to hold the line on prices despite tariffs. They even boasted that their ability to do so represented “a great opportunity for us to take share.”

Fast forward three months to their latest quarterly report, and the retailer now says “there will be some modest price movement in some categories.”

What changed? William Bastek, Home Depot executive vice president of merchandising, told analysts: “Now some of the imported goods, obviously, tariff rates are significantly higher today than they were when we spoke in May.”

That actually isn’t obvious. With all the back and forth, threats and last-minute deals, investors could be forgiven for not having a clear picture of what Home Depot’s import bills look like now compared with three months ago.

But this highlights a broader point: With all the uncertainty over tariffs, it has broadly made sense for companies to hold the line on pricing. After all, why upset customers with a price hike over a tariff that could go away in an instant?

Yet companies can’t sit on their hands forever. On Thursday, investors will be looking for more clarity from the big boy of retail, Walmart. Unlike Home Depot, it admitted last quarter that some price hikes were inevitable, but told investors to wait for their second-quarter update for fuller guidance.

Economists at Goldman Sachs, in a widely discussed note this month, shed further light on what’s happening. Looking at the first wave of tariffs against China back in February, they found that U.S. companies initially absorbed the costs, but now are passing on more to consumers. Specifically, they found that “around 36% of tariff costs were passed onto consumer prices after three months of implementation and around 67% were passed on after four months.”

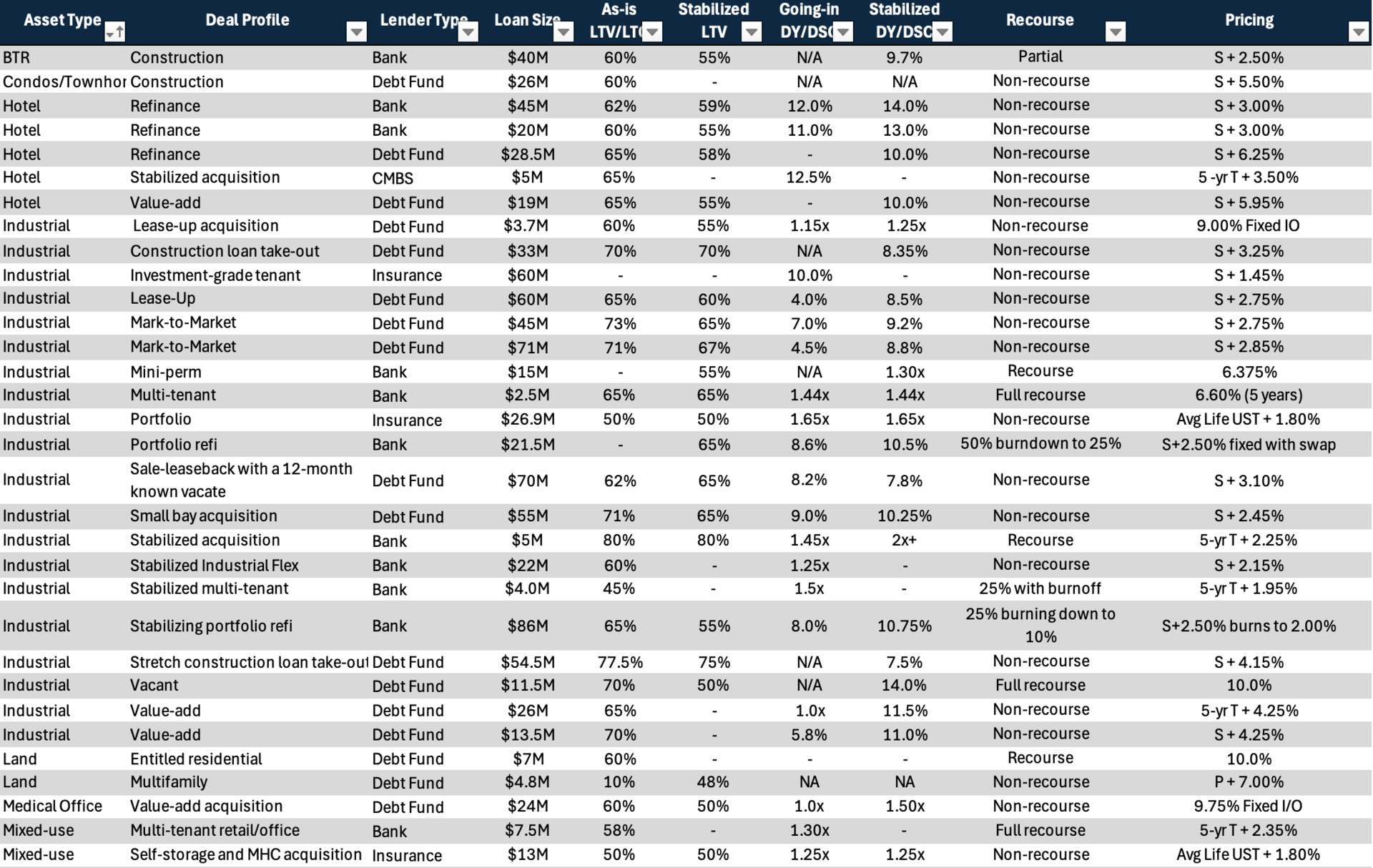

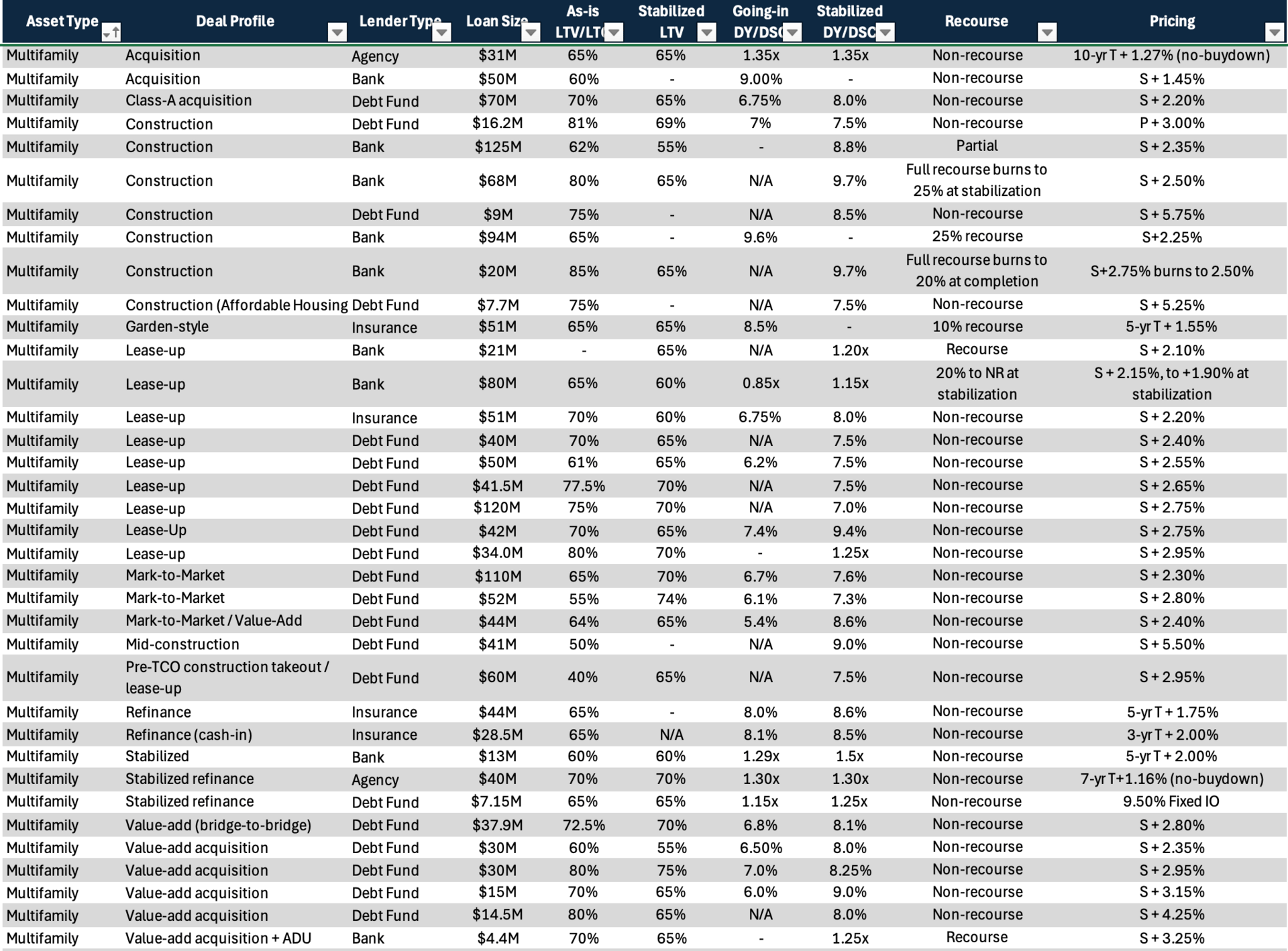

Brandon Roth, IPA: Debt Market Update - lender quotes between August 12-15

Amazon last week announced same-day delivery for fresh groceries in 1,000 U.S. cities, with plans to more than double that number by year-end. The company also significantly lowered the price threshold for free delivery to a $25 minimum order size for members of its Prime shipping service, compared with $100 earlier.

The news shows that Amazon is leaning into two of its competitive strengths—a vast same-day fulfillment network and its popular Prime program—to make a bigger dent in groceries. The latter alone is significant. Consumer Intelligence Research Partners estimated that Amazon Prime had 197 million subscribers in the U.S. at the end of June.

In a report last week, Horowitz estimated that if 5% to 10% of U.S. prime members use the service every other week at an average order size of $45, that could add as much as 3% to Amazon’s revenue growth.

The rub is that expanding its selection will likely require Amazon to invest more in the type of infrastructure needed to handle perishable food. Marc Wulfraat, president of logistics consultant MWPVL International, estimates that Amazon currently has about 1.5 million square feet of refrigerated fulfillment space in its distribution network—a fraction of the 19.6 million square feet that Walmart operates across its own network.

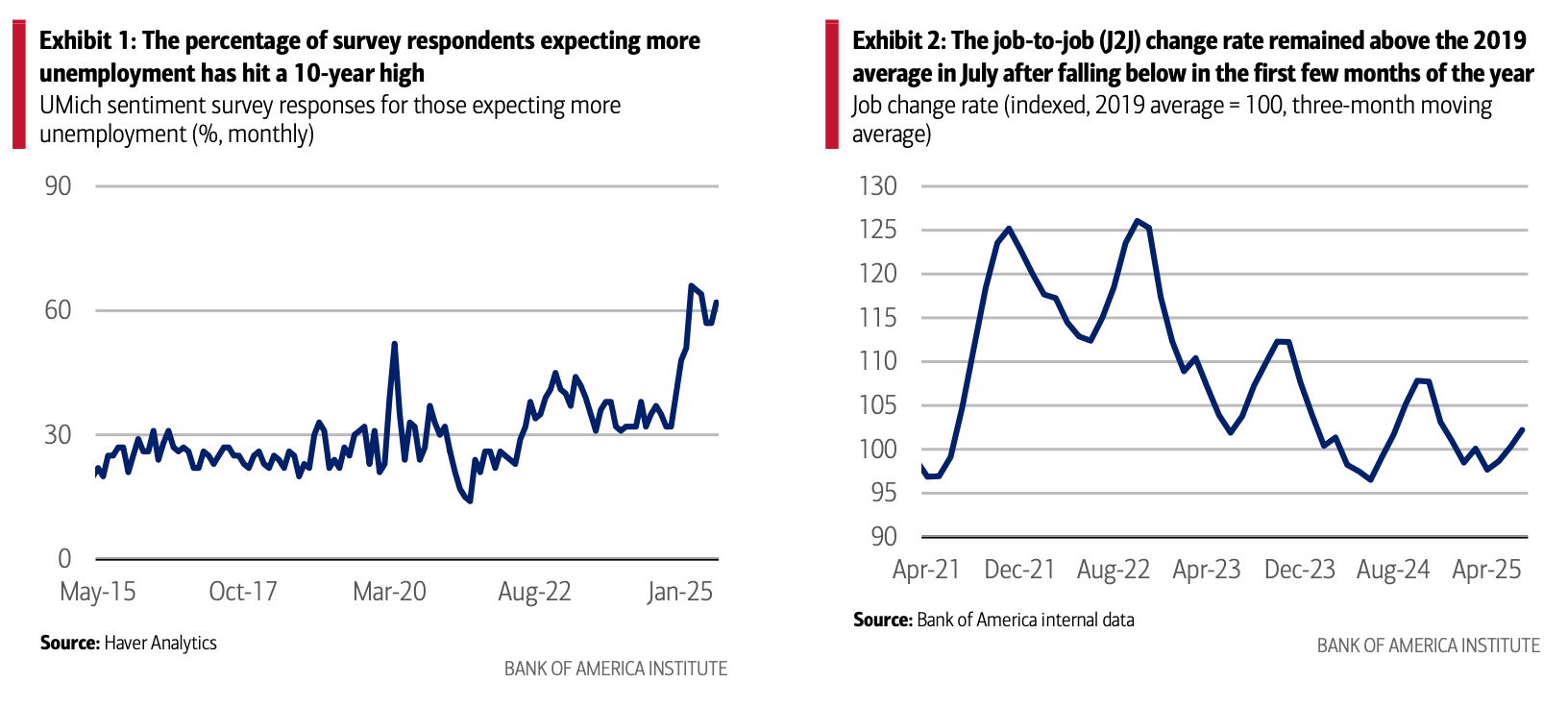

Fears of rising unemployment hit a 10-year high in March and have yet to abate, according to the latest University of Michigan (UMich) Consumer Sentiment survey

And in the current “low-fire, low-hire environment,” the August employment report from the Bureau of Labor Statistics (BLS) underscored that jobs growth slowed significantly in the second quarter. Some areas of the labor market are harder to track than people who are moving between employment and unemployment.

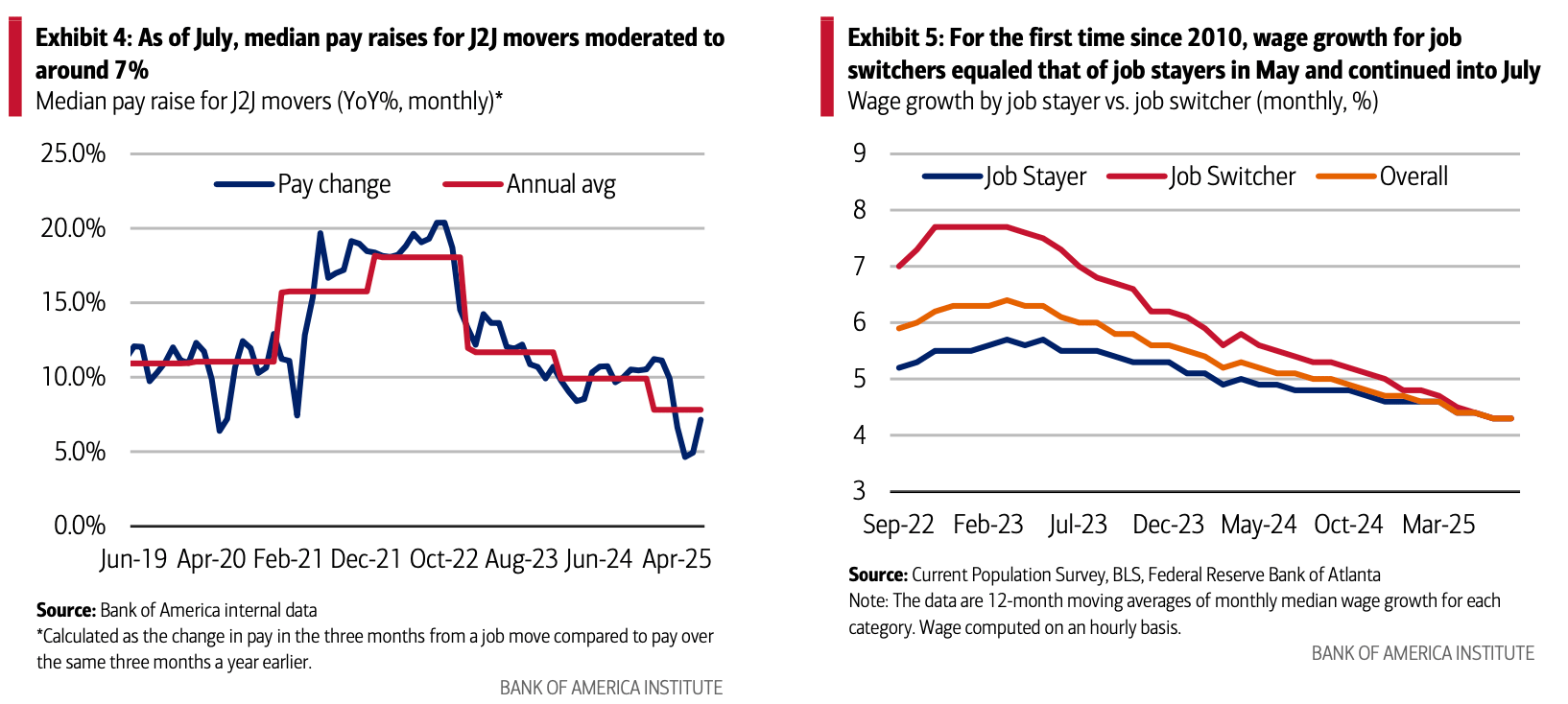

People making job-to-job (J2J) moves and the pay raises they are getting when they make these moves are potentially harder to measure but are an important part of the overall labor market picture.

Bank of America deposit data also shows that wage disparities are widening. In fact, we see that the gap between higher- and lower-income wage growth has now reached the highest since February 2021. Thus, the labor market appears to have deteriorated most significantly for lower-income workers.

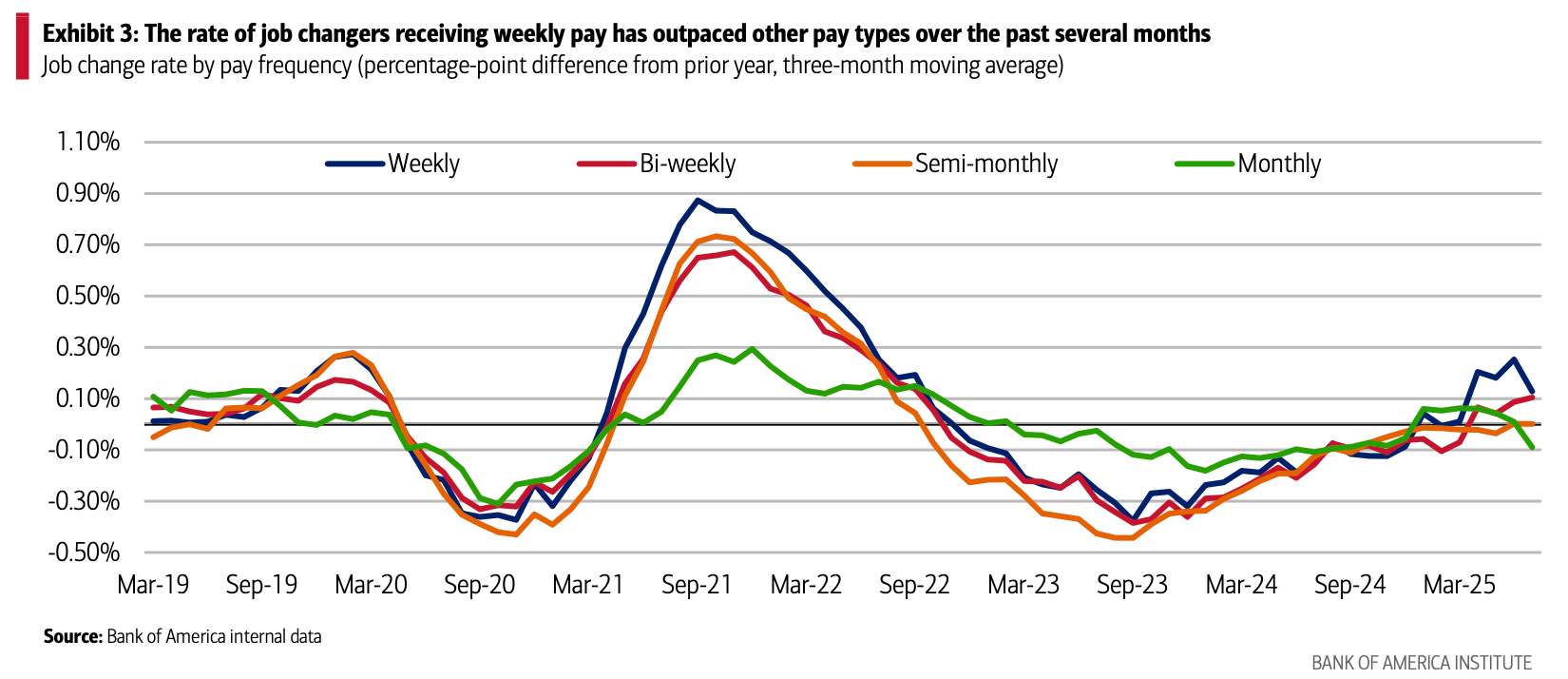

Within the J2J data, we also found that there has been some divergence among job changers by pay frequency type. According to the Bureau of Labor Statistics (BLS), in 2023, biweekly was the most common length of pay period, around 43%, followed by weekly pay periods (27%). Interestingly, job hoppers with monthly pay have been cooling, with the rate down 0.09%, while weekly pay is strongest, up 0.13% in July on a three-month moving average. Industries with the greatest share of monthly pay are financial activities, professional & business services, and information, all of which skew towards higher-income jobs.

This suggests that fewer people are changing jobs in these industries compared to industries such as construction and manufacturing, where weekly pay is more heavily concentrated and labor supply issues are already at play

With signs that J2J moves are gradually moderating, we also find that job hoppers are getting smaller pay increases from their new employers.

Though there has been a bounce-back from June, the increase declined to around 7% in July from more than 20% when the Great Resignation was in full swing in 2022. It is notable that last month’s figure is below 2019 levels and, so far this year, has fallen further from the 2024 annual average. This is in line with data from the Atlanta Fed, which shows that in May, for the first time since 2010, wage growth for job switchers equaled that of those who remained with their employers. This was the case through July.

This trend confirms that the labor market is no longer as tight, and the balance of power between employer and employee is shifting back toward firms that are hiring. It also likely reflects a tariff-related pullback in business investment, which is leading employers to pause hiring altogether

Home-purchase contracts in the US were canceled at a record rate, with about 58,000 agreements falling through last month.

That’s equivalent to 15.3% of homes that went under contract and the highest cancellation rate for a July in data going back to 2017.

This year, the number of major metro area housing markets seeing year-over-year declines has climbed.

31 of the nation’s 300 largest housing markets (i.e., 10% of markets) had a falling year-over-year reading in the January 2024 to January 2025 window.

42 of the nation’s 300 largest housing markets (i.e., 14% of markets) had a falling year-over-year reading in the February 2024 to February 2025 window.

60 of the nation’s 300 largest housing markets (i.e., 20% of markets) had a falling year-over-year reading in the March 2024 to March 2025 window.

80 of the nation’s 300 largest housing markets (i.e., 27% of markets) had a falling year-over-year reading in the April 2024 to April 2025 window.

96 of the nation’s 300 largest housing markets (i.e., 32% of markets) had a falling year-over-year reading in the May 2024 to May 2025 window.

110 of the nation’s 300 largest housing markets (i.e., 36% of markets) had a falling year-over-year reading in the June 2024 to June 2025 window.

105 of the nation’s 300 largest housing markets (i.e., 35% of markets) had a falling year-over-year reading in the July 2024 to July 2025 window.

Through 2025, more housing markets have slipped into year-over-year price declines as the supply-demand balance gradually tilts toward buyers in today’s affordability-constrained, post-boom environment.

But this month, that list of declining markets actually got a little shorter.

Home prices are still climbing in many regions where active inventory remains well below pre-pandemic 2019 levels, such as pockets of the Northeast and Midwest. In contrast, some pockets in states like Arizona, Texas, Florida, Colorado, and Louisiana—where active inventory exceeds pre-pandemic 2019 levels—are seeing modest home price pullbacks.