- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 08.30.2025

Location Strategy Chartbook 08.30.2025

Real Estate Market Insights

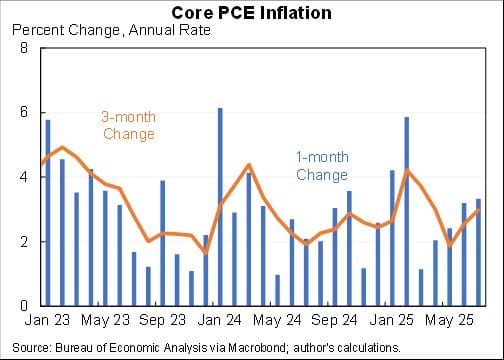

Jason Furman: The core PCE inflation rate increased for the fourth month in a row.

1 month: 3.3% 3 months: 3.0% 6 months: 3.0% 12 months: 2.9%

But two reasons to be less worried than headline: (1) transitory tariffs & (2) some of this is imputed from rising stock market.

Market core is both better predicted by slack and a better predictor of future inflation. It has moved sideways this year. But given that tariffs are (hopefully temporarily) pushing inflation up that suggests that underlying inflation is going down.

A big increase in consumer spending but it is still roughly flat since December with a lot of downs and ups

Parcels entering the country will now be assessed duties based on the country-of-origin tariff rate Trump imposed.

Alternatively, packages shipped via international post could be assessed with a temporary flat fee of $80 to $200 per item, but only for the next six months.

The sale of the retail component at the New York Times' former headquarters shows how distressed properties are still taking a toll.

The $28 million paid to acquire part of 229 W. 43rd St. in Manhattan was the year's largest liquidation loss for lender-owned real estate backed by commercial mortgage-backed securities.

The price was a fraction of its $470 million appraised value in 2016. CMBS investors lost more than $175 million on the original $205 million loan, according to CoStar data. The deal was the latest of 15 CMBS lender-owned properties that have sold in 2025 for a combined total of more than $187.5 million

Investors snapped up these distressed properties at 24% off their most recent appraised values. Meanwhile, CMBS investors absorbed massive losses totaling nearly $353 million from the original loan amounts.

The CMBS market holds billions of dollars more in distressed opportunities that eventually could emerge, according to CoStar and Morningstar DBRS data.

There are 250 individual CMBS-financed properties or business parks where current loan balances exceed recent appraised values. These properties have an average loan-to-value ratio of 192%, indicating severe overleverage.

The numbers reveal the scope: Total current debt of $15.9 billion dwarfs the most recent appraised property values of $9.7 billion. Some properties carry loan-to-value ratios exceeding 300%, signaling a complete erosion of value.

Office buildings comprised 52% of distressed loans, according to the data, with retail properties accounting for another 24%. The data points to loans originated primarily in the mid-2010s now hitting maturity walls, creating urgent refinancing pressure in today's higher-interest-rate environment.

Loan performance has deteriorated sharply: 86% of loans are delinquent, 22% face active foreclosure and 28% have already become lender-owned properties.

LNR Securities leads all special servicers, managing 86 loans backed by $2.4 billion in appraised property values. Rialto Capital Advisors manages 59 loans totaling $1.2 billion in property value, while CWCapital Asset Management handles 24 loans valued at $1.1 billion.

Orange County CA defies multifamily trends and keeps building

Irvine remains the epicenter of Orange County’s apartment boom.

The Irvine Co.’s 1,200-unit Colonnade at The Marketplace redevelopment

1,100-unit Pacific Place at Irvine Spectrum

313-unit 6700 Roosevelt — Avella II.

Over the past decade, 11,000 of Orange County’s 29,000 new units have been developed in Irvine, making it the largest apartment market.

More than 4,000 units are under construction in Irvine. The Irvine Co. dominates, more than 70% of the market-rate apartment stock and two-thirds of the supply underway.

New Jersey-based Garden Homes is also active, developing the 876-unit Volar and the 124-unit Phase 3 of the Elements complex.

Anaheim: El Segundo-based Abacus Capital Group is developing a 269-unit complex called The Invitation at 1122 N. Anaheim Blvd. in North Anaheim, scheduled for completion next year

Lennar is developing a mixed-use master-planned project adjacent to Angels Stadium called A Town, 508 units are underway.

WSJ: Middle and high-income consumers have been flocking to dollar stores this year, helping catapult those retailers’ year-to-date stock gains above Nvidia’s.

Dollar Tree and Dollar General, the latter of which reports earnings today, have each gained close to 50% so far this year, making them the top two brick-and-mortar retail stocks in the S&P 500.

Dollar General said in its June earnings call that it saw the highest percentage of trade-down customers in the past four years. Dollar Tree said it saw a “meaningful traffic increase” from households making more than $100,000.

Is this a warning about consumer health? Another time dollar stores saw a spike in sales from wealthier customers was in 2008 during the Great Recession. But while nationwide retail sales tanked back then, they’re still growing at a healthy clip this year.

Combined, Morgan Stanley estimates retailers selling overlapping items with dollar stores lost about $3 billion of sales in the first quarter compared with a year earlier. The two dollar-store chains collectively gained about $1 billion. The bank forecasts even more declines from competitors ahead, peaking at $5.9 billion in the fourth quarter before moderating in 2026

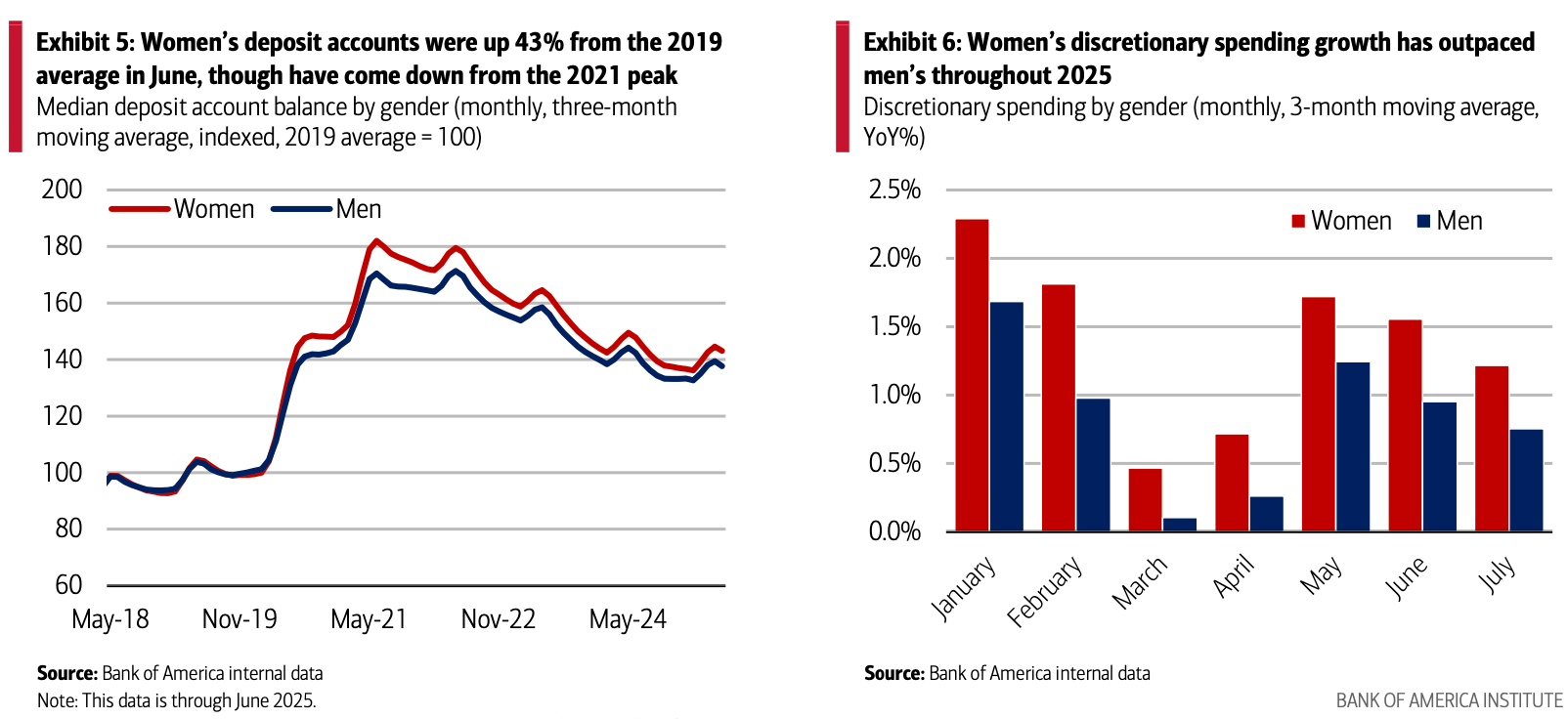

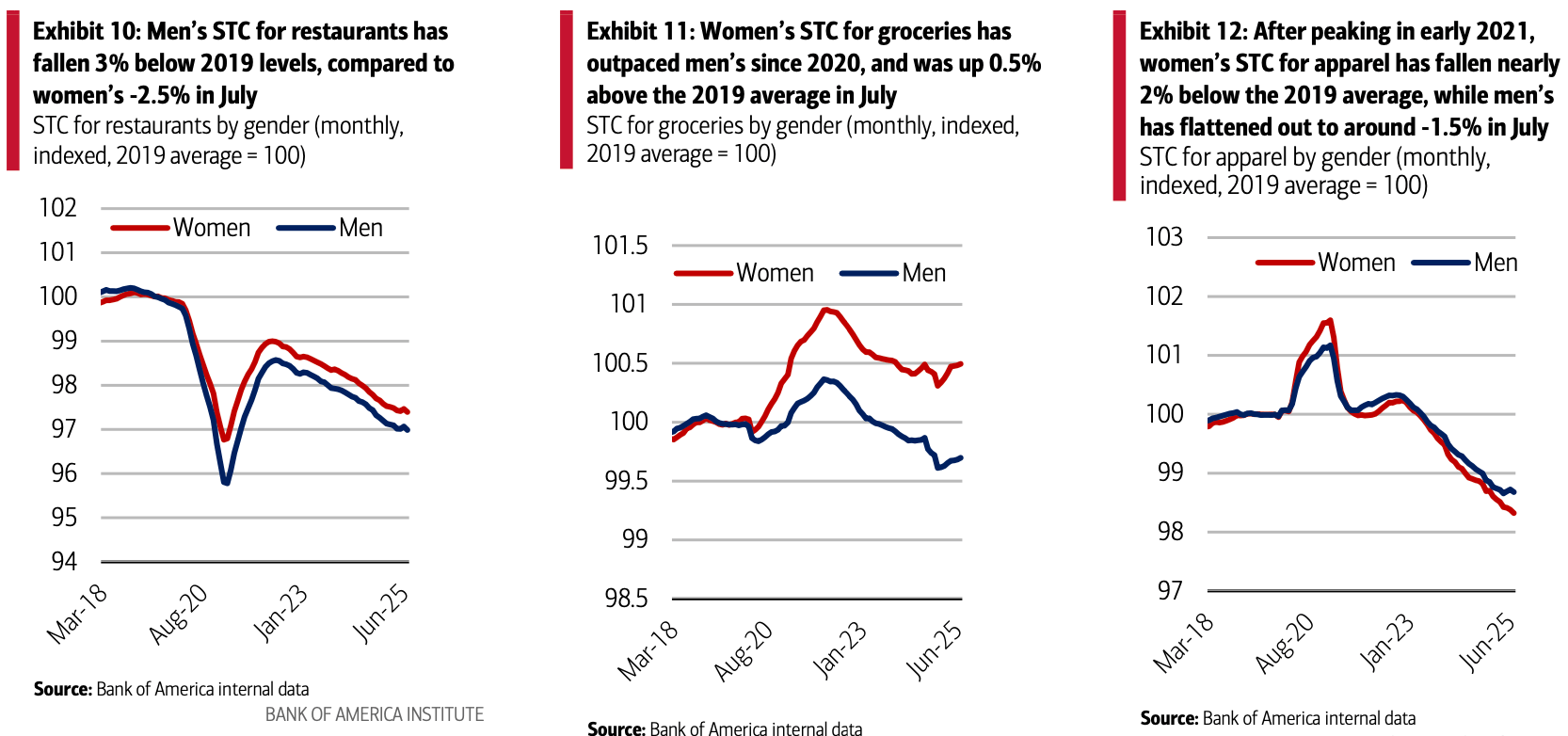

Women's average annual growth in labor force participation rate fell below men's for the first time in six years. But despite a cooling labor market, Bank of America deposit account data indicates both women and men's pay disruption rate remains below the 2024 average level, suggesting an imbalance in trends between the two isn't yet stark.

For both men and women, the median pay raise associated with a job change has fallen below 2019 levels, though the increase in associated rise in pay for women is greater than men's, helping narrow the gender pay gap. And according to Bank of America deposit account data, women's checking and savings account balances were up 43% from the 2019 average in June. This has bolstered women's spending growth, especially on discretionary items.

Stronger wage growth for women – either through job changes or otherwise – drives further financial stability and fuels spending growth. And, in fact, Bank of America deposit account data found that women’s checking and savings account balances were up approximately 43% from the 2019 average, compared to 37% above the 2019 average for men in June

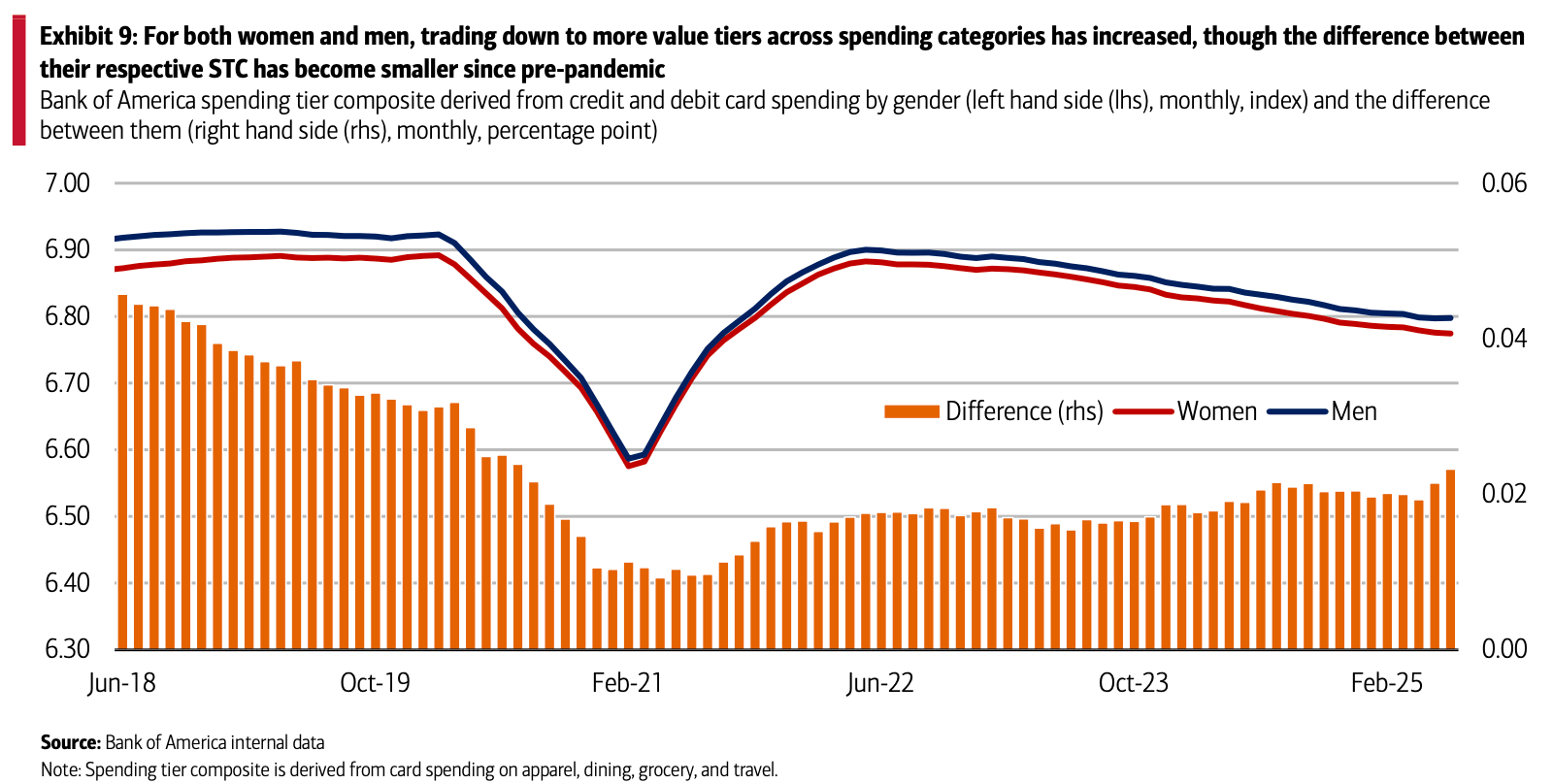

Trading down remains a key theme for spending, and we see evidence of that in a proprietary gauge that ranks spending across “premium,” “standard” or “value” tiers, which we call the spending tier composite (STC). To create the composite, we first ranked spending into tiers (see Methodology) and came up with a score for each spending category, of which there are four. For example, if a customer spends most of their money at premium stores, that equals a score of “3,” while standard is a “2” and value equals “1.” Based on our analysis, “value” is gaining appeal among consumers overall. And though the difference between STC by gender has come down since pre-pandemic, it is starting to marginally increase once again, with women still seeking value when they shop slightly more than men.

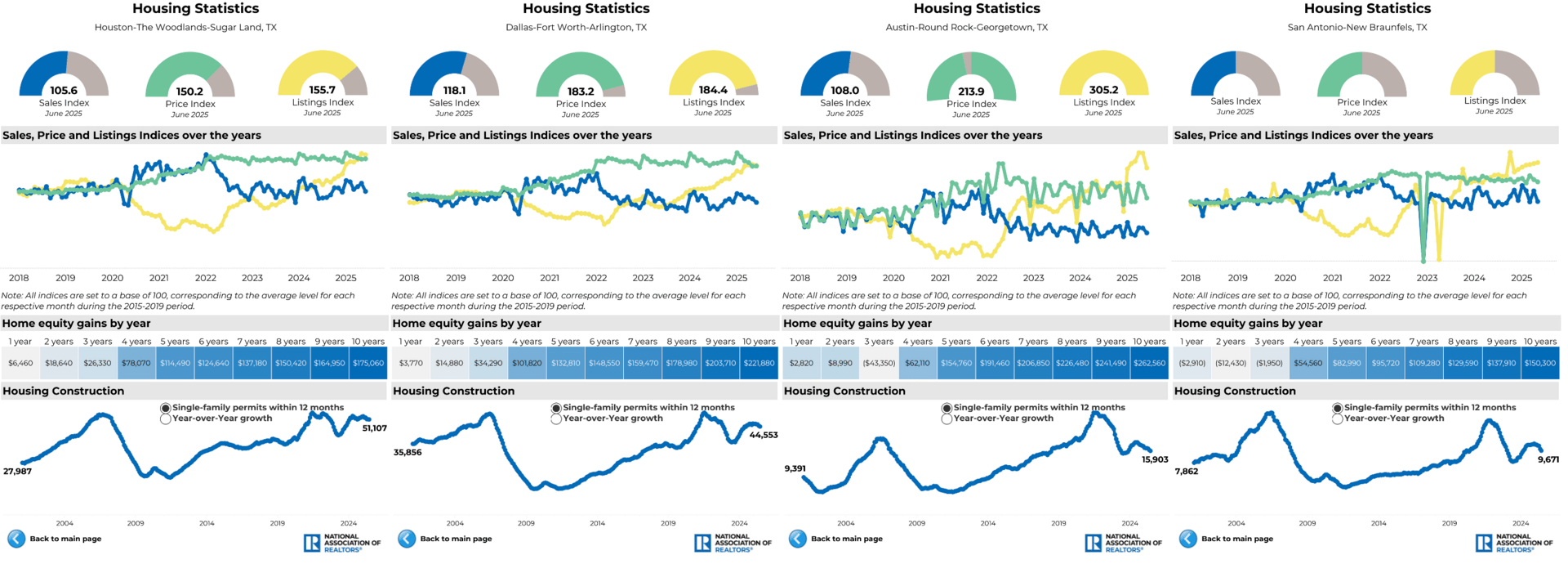

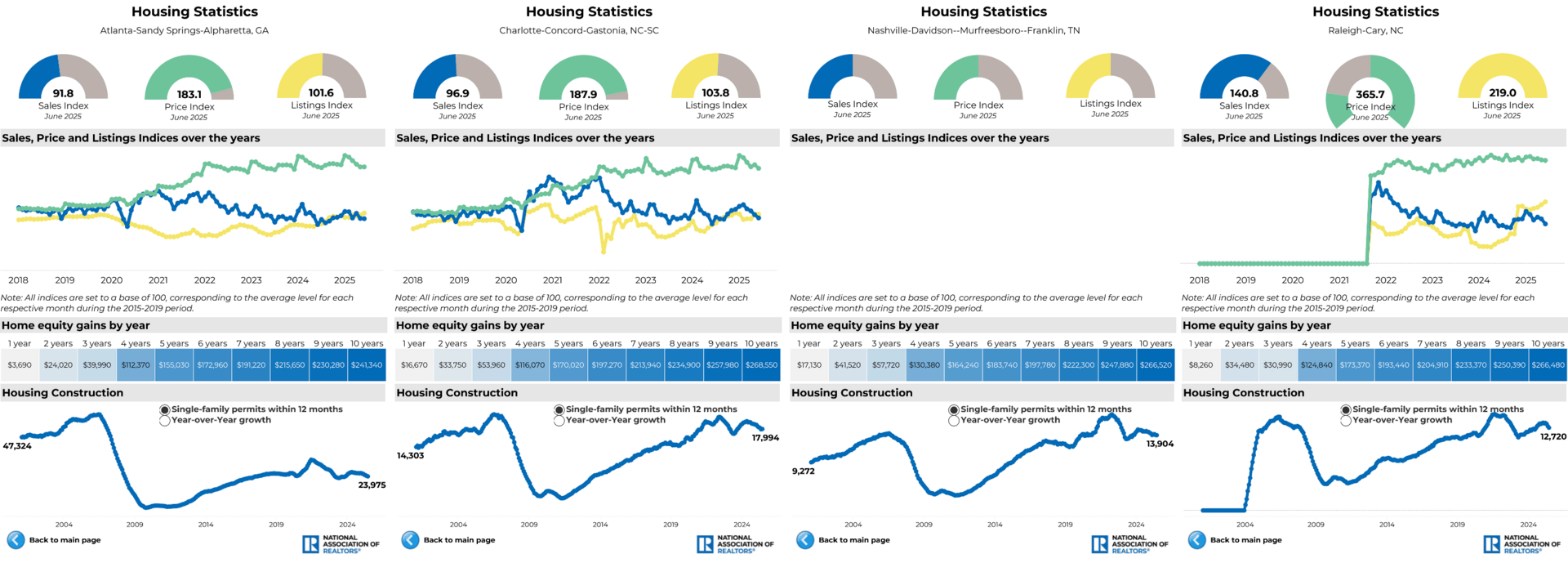

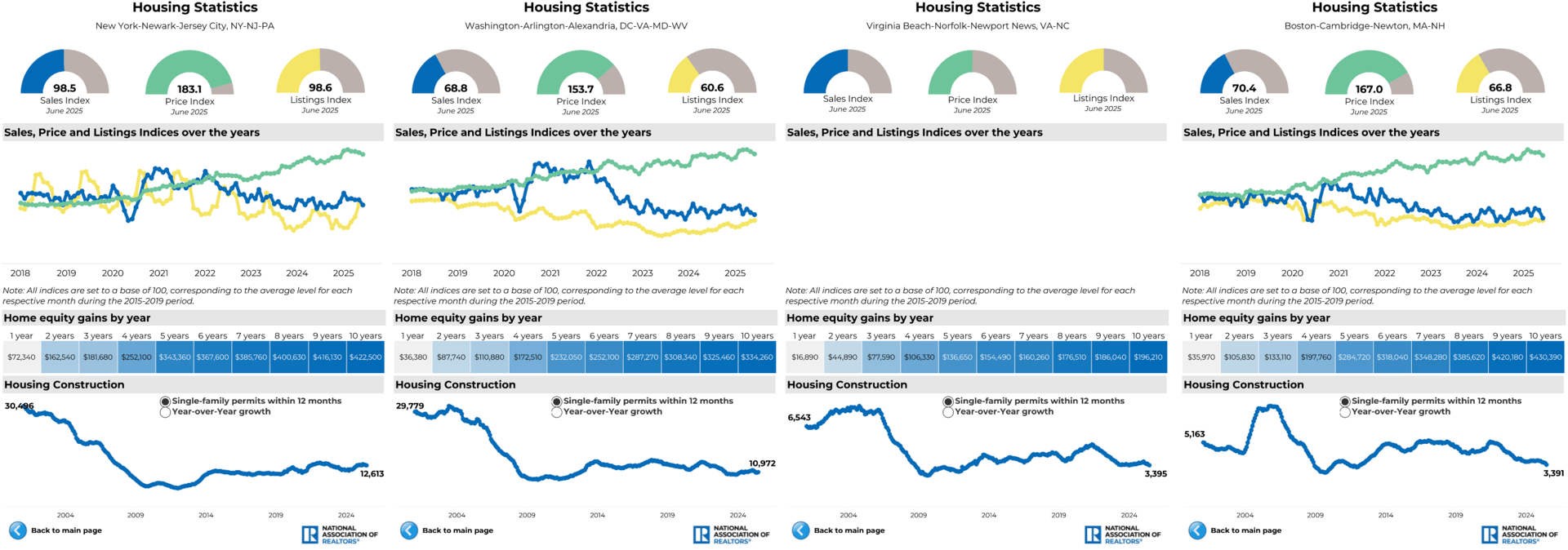

Texas leads the nation in new single family home permits in the past 12 months

The desert West is building the most housing in the West, with CA and the PNW adding an anemic amount of new SFR

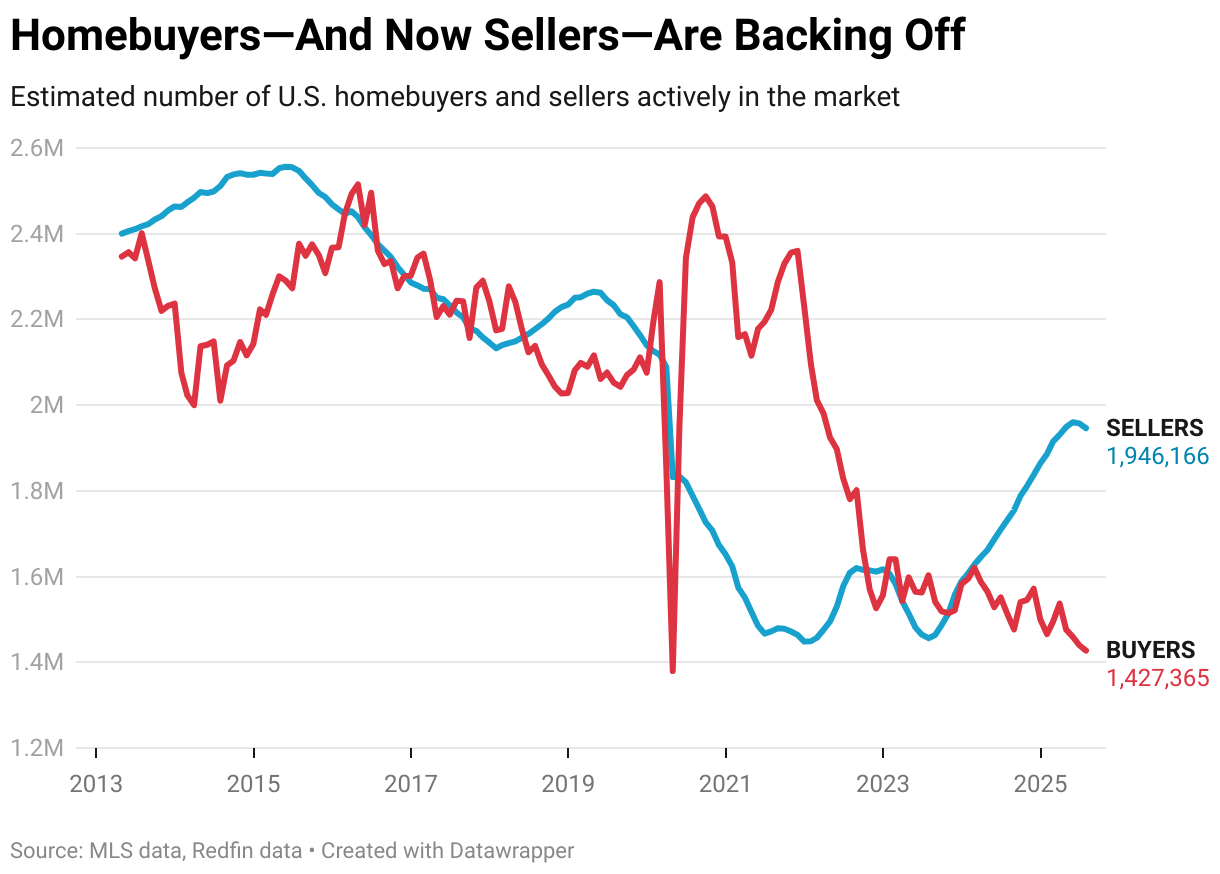

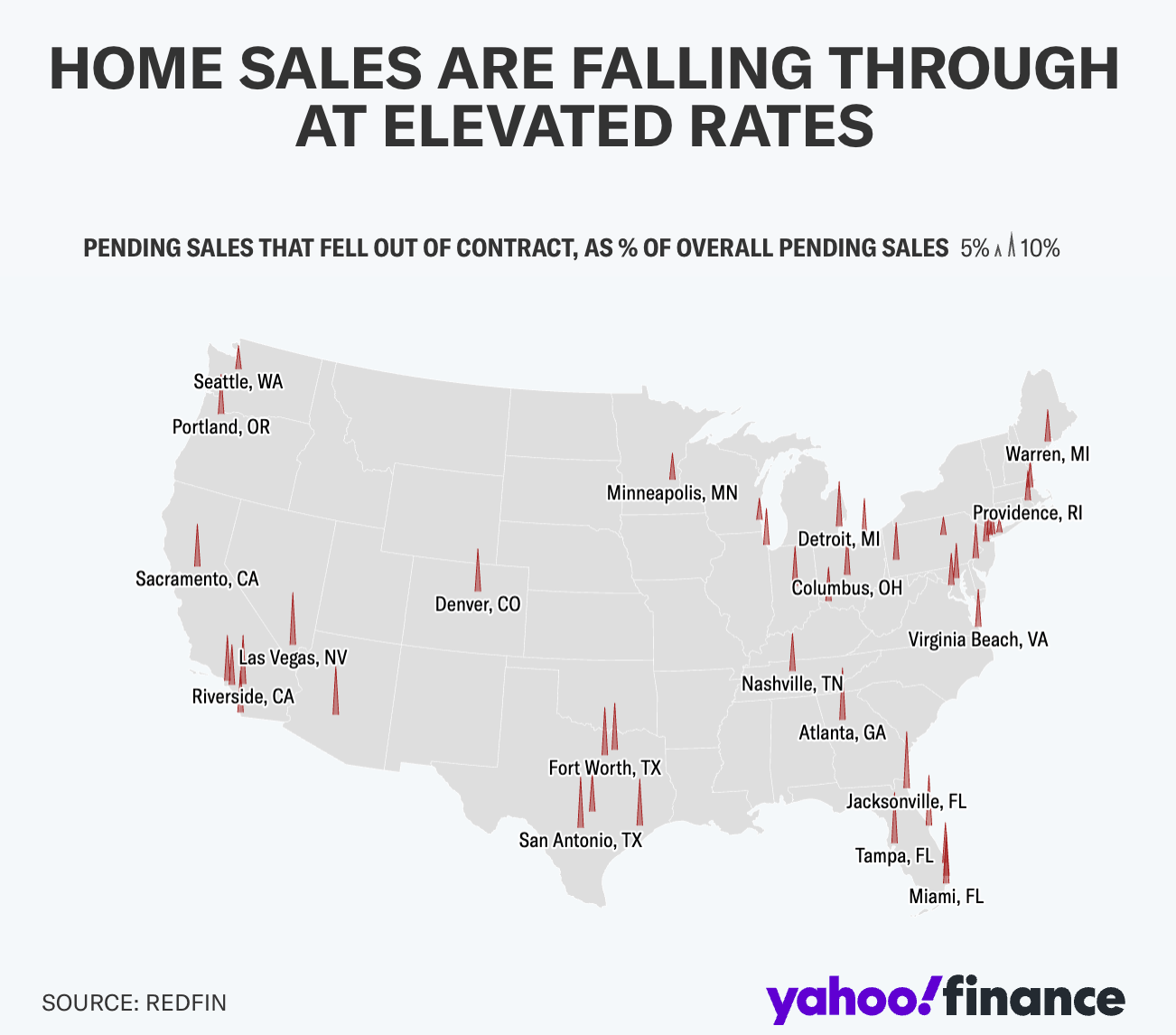

Last month, 57,000 deals — 15% of all homes that went under contract — fell through, the highest share of canceled deals in June going back to 2017, according to Redfin. The brokerage cited factors like financially stretched buyers and ongoing economic uncertainty for the spike.

Delistings, where sellers take their homes off the market without a sale, are also on the rise. They jumped 47% in May from a year ago, outpacing recent inventory gains, according to Realtor.com. This move suggests that many sellers would rather stay put than adjust to current market dynamics.

The U.S. housing market has lost about 14,000 home sellers over the past two months, with the total number of sellers falling to 1.95 million in July from a peak of 1.96 million in May. This marks the first decline since July 2023, when the supply of homes for sale bottomed out near a historic low as rising mortgage rates made homeowners reluctant to sell.

Still, sellers outnumber buyers by the widest margin in records dating back to 2013; there were an estimated 1.43 million homebuyers in the housing market in July—the lowest level on record aside from the onset of the pandemic, when the housing market ground to a halt.