- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 09.06.2025

Location Strategy Chartbook 09.06.2025

Real Estate Market Insights

This week will be a departure from the usual round up of charts and focus on 2 topics: data centers and utilities and their constraints. The availability and cost of water and power impacts all real estate types as everyone is competing for the same infrastructure and supply. The industry is seeing growing impact fees to price hikes and higher downstream costs to the end user.

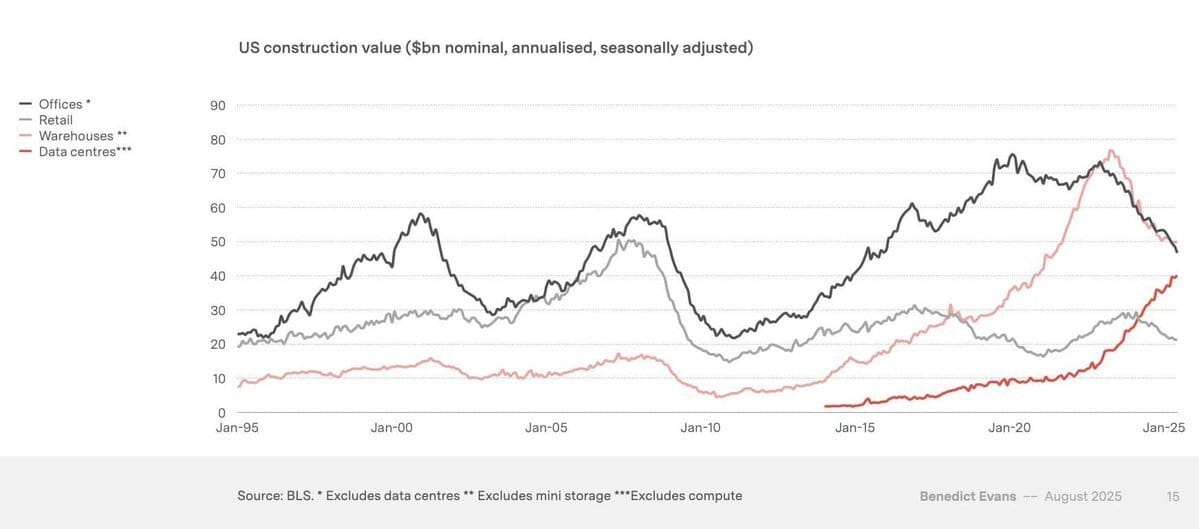

Data center construction is set to outpace office and warehouse/industrial

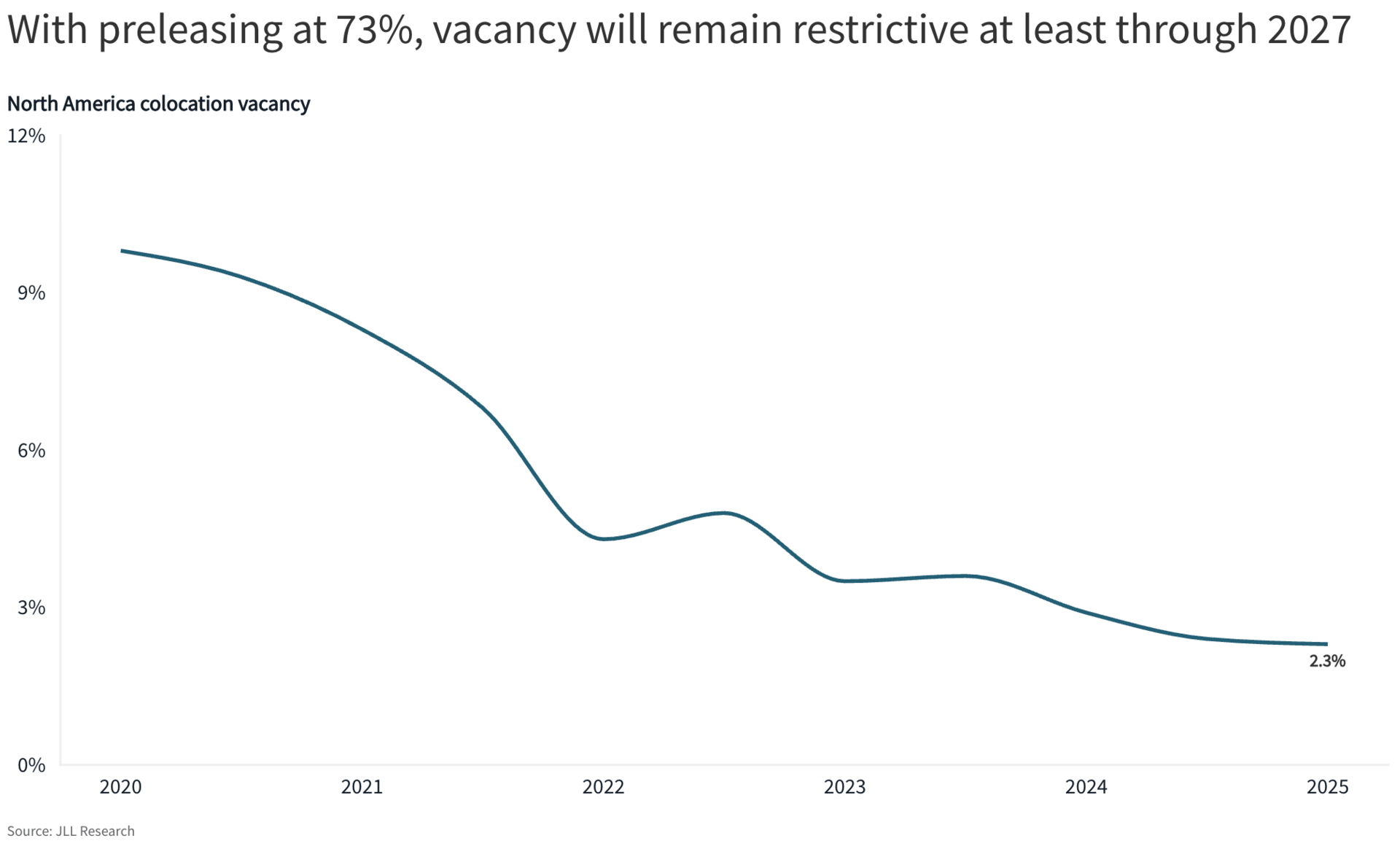

JLL: Vacancy declines to a new record low, constraining sector growth

Colocation vacancy is nearing 0%, which is constraining economic growth and undermining national security. Data centers are critical infrastructure and restrictive market conditions are counterproductive over the long-term.

The construction pipeline of 8 GW is 73% preleased, signaling that any meaningful loosening of market conditions remains a few years away at minimum. Even if preleasing activity slows significantly in the near-term, vacancy would likely remain below 5% through 2027. A more likely scenario is that vacancy holds in the 2% range through 2027.

Companies looking to expand their data center operations may be limited to preleasing in new developments. This could be followed by a year or more of waiting for construction to be completed before taking occupancy.

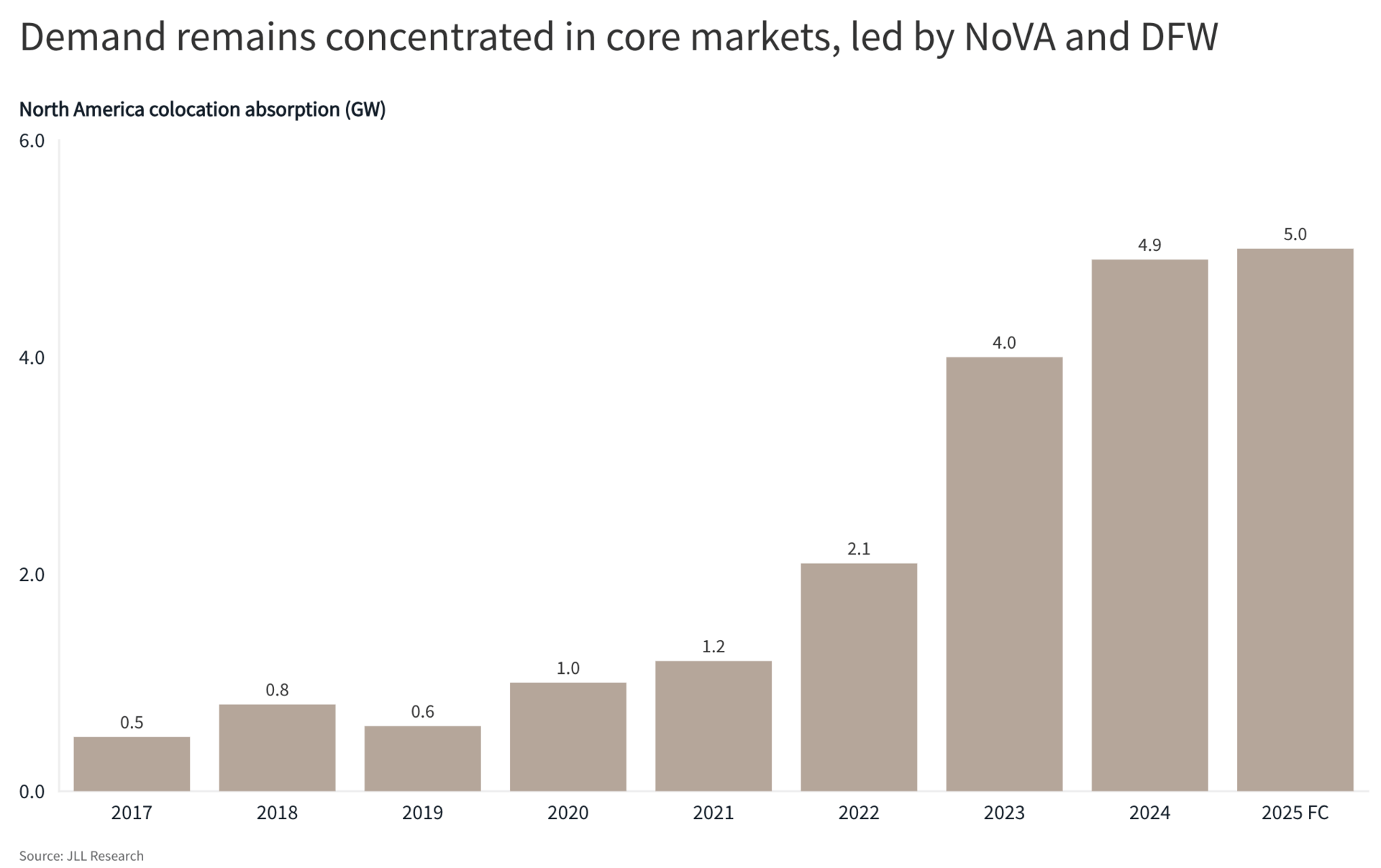

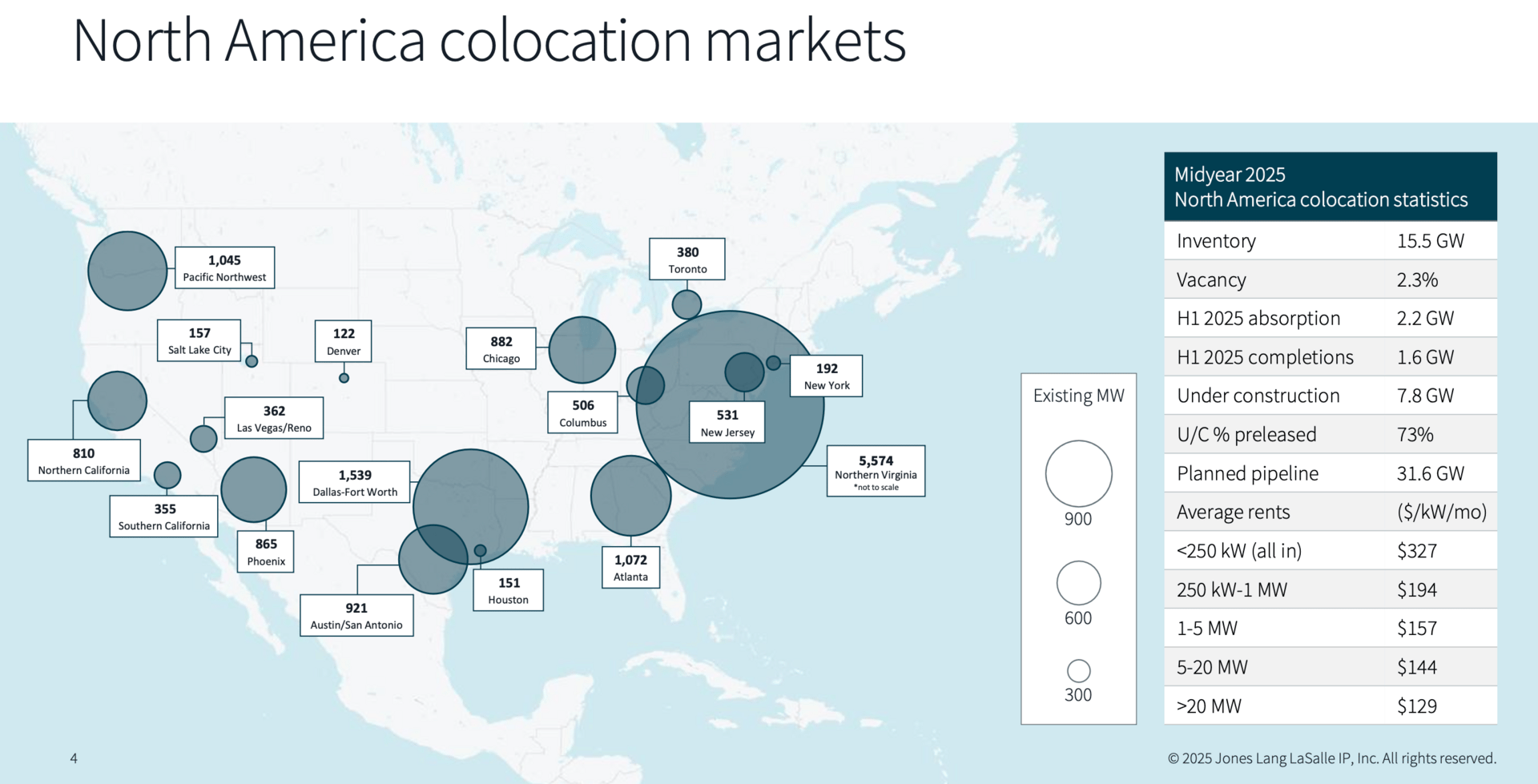

Some data center development has been moving into secondary and tertiary markets in search of power, lower costs and speed to market. This is particularly true for hyperscale projects. However, emerging markets are only capturing a fraction of colocation demand. JLL’s market data continues to demonstrate that colocation demand is concentrated in core markets.

In the first half of 2025, 50% of absorption was recorded in two markets: Northern Virginia (647 MW) and Dallas (575 MW). Rounding out the top 5 markets for absorption in H1 were Chicago (368 MW), Austin/San Antonio (291 MW) and Atlanta (150 MW).

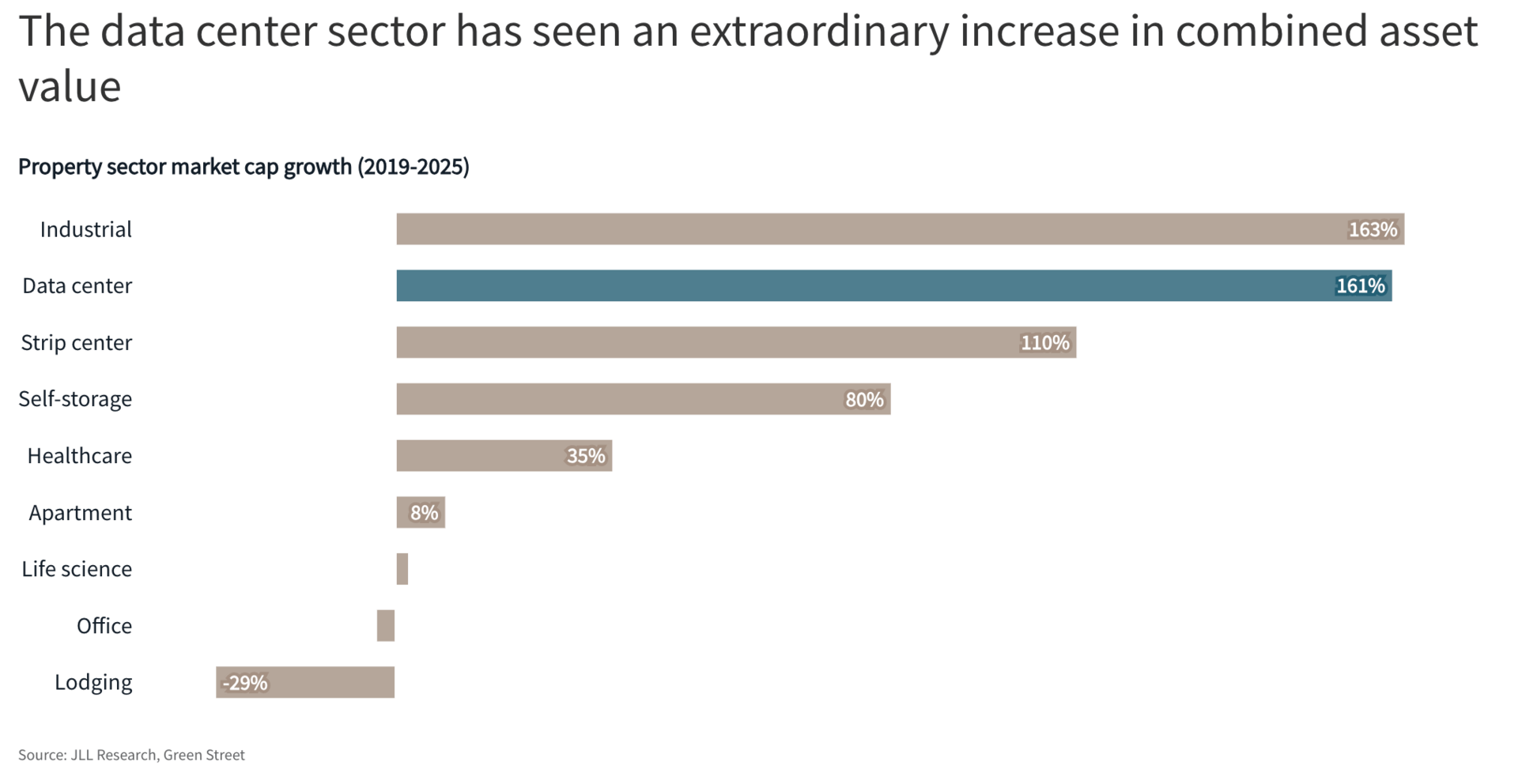

The data center sector remains among the most favored real estate asset classes due to insatiable tenant demand, limited supply and rising rents.

Preleasing demand continues to bode well for all phases of data center financing including construction loans, transitional loans, and stabilized loans. The lender pool depth continues to expand, inclusive of commercial real estate banks, project finance lenders, life companies, and debt funds.

Horizontal development financing needs have been in higher demand as utility companies are requiring hard deposits earlier in the power procurement process. There are also increased capital needs by development groups utilizing behind-the-meter solutions or bridging alternatives.

Driven by AI adoption and increasing data usage across sectors, the industry is experiencing record levels of demand, with expectations of doubling all data center capacity within the next five years. There is also a shift in what projects are considered large – from 20 MW a few years ago to 100 MW+ transactions now becoming more common.

Between 7 and 10 gigawatts are expected to be absorbed this year, though some experts expressed slight concerns about AI assumptions and potential hyperscaler leasing slowdowns in 2025. Companies are now starting to speculatively buy and develop onsite generation due to lead time issues with grid delivery.

Strong investor interest continues despite some increased risk perception.

“There is a record setting number of data center developments under construction, which is driving the need for more creative debt and equity solutions,” said Carl Beardsley, Senior Managing Director, Data Center Leader, JLL Capital Markets. “Data Center REITs have outperformed all other real estate asset classes since the tariffs were announced, and the debt markets remain liquid despite some macro volatility. There are also more investors coming into the data center sector, as development deals are requiring heavier capital commitments earlier on in the process based on new utility procurement processes.”

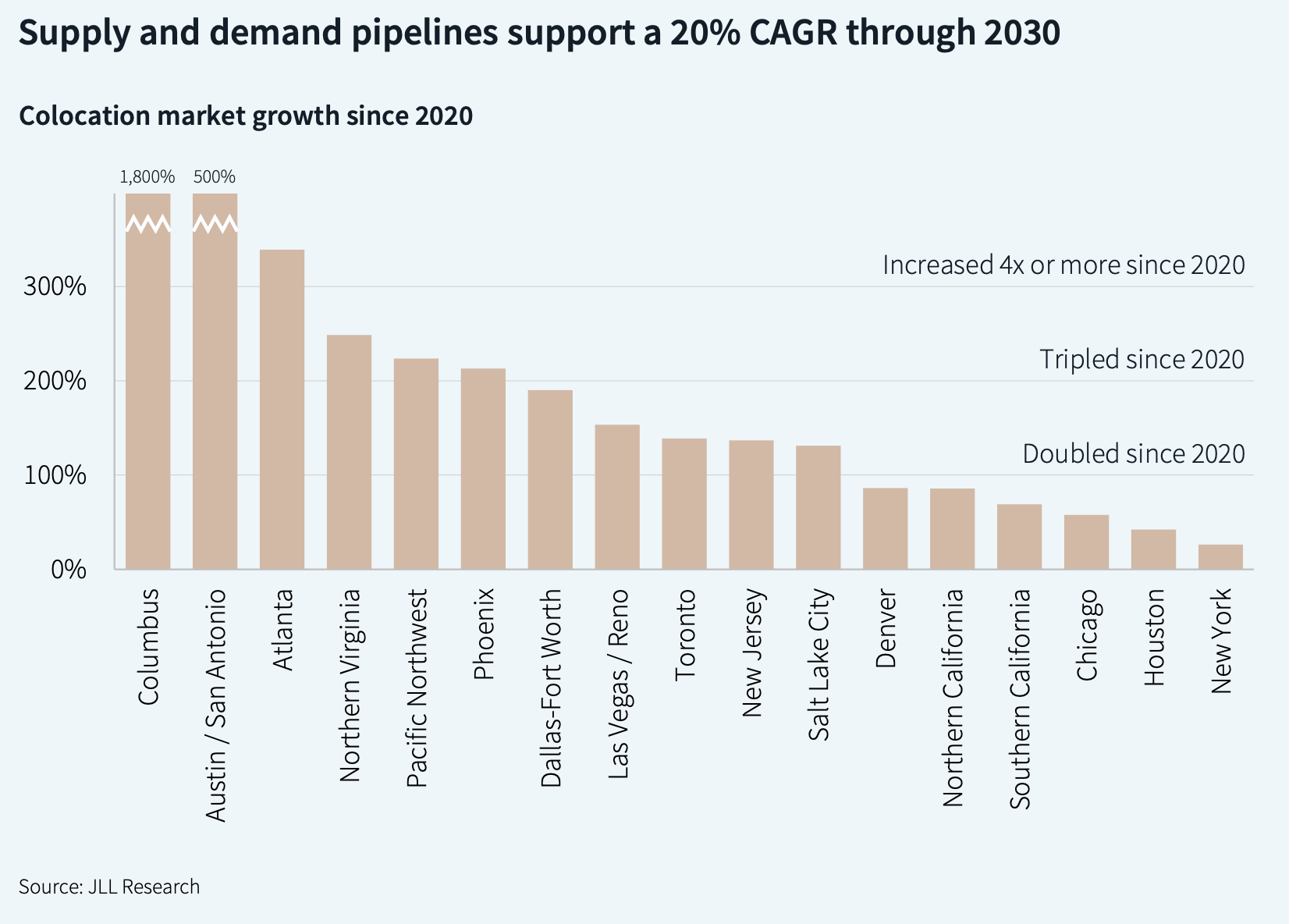

The data center sector in North America has been growing at a 20% CAGR since 2017. Over that time, most markets have doubled or tripled in size. On a percentage basis, the leading growth markets have been Columbus and Austin/San Antonio. However, they started from a small base in 2020. In absolute terms, Northern Virginia (+3,975 MW), Dallas (+1,008 MW) and Atlanta (+828 MW) have seen the largest increase in capacity. The development pipeline and demand signals support continued sector growth at a 20% CAGR through 2030, at which point the North America colocation market could total more than 42 GW. The markets with the largest development pipelines including under construction and planned projects are Northern Virginia (7 GW), Phoenix (5 GW), Dallas (5 GW), Chicago (4 GW) and Las Vegas/Reno (4 GW).

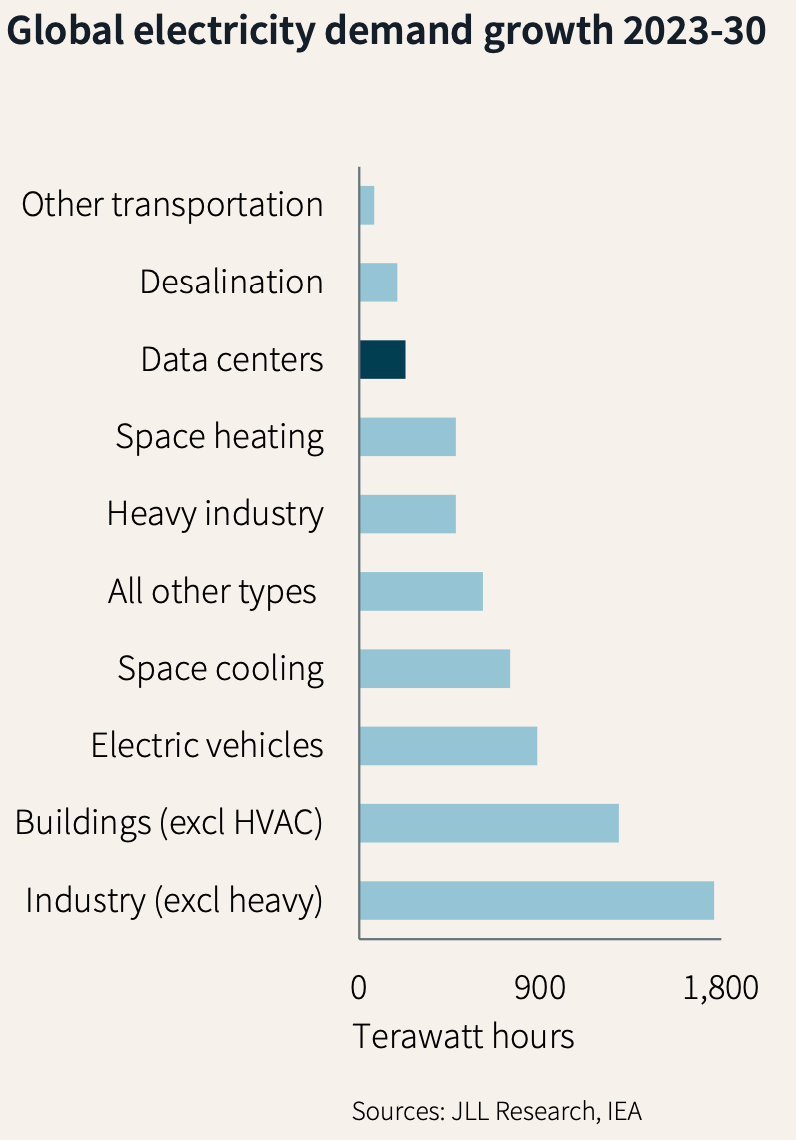

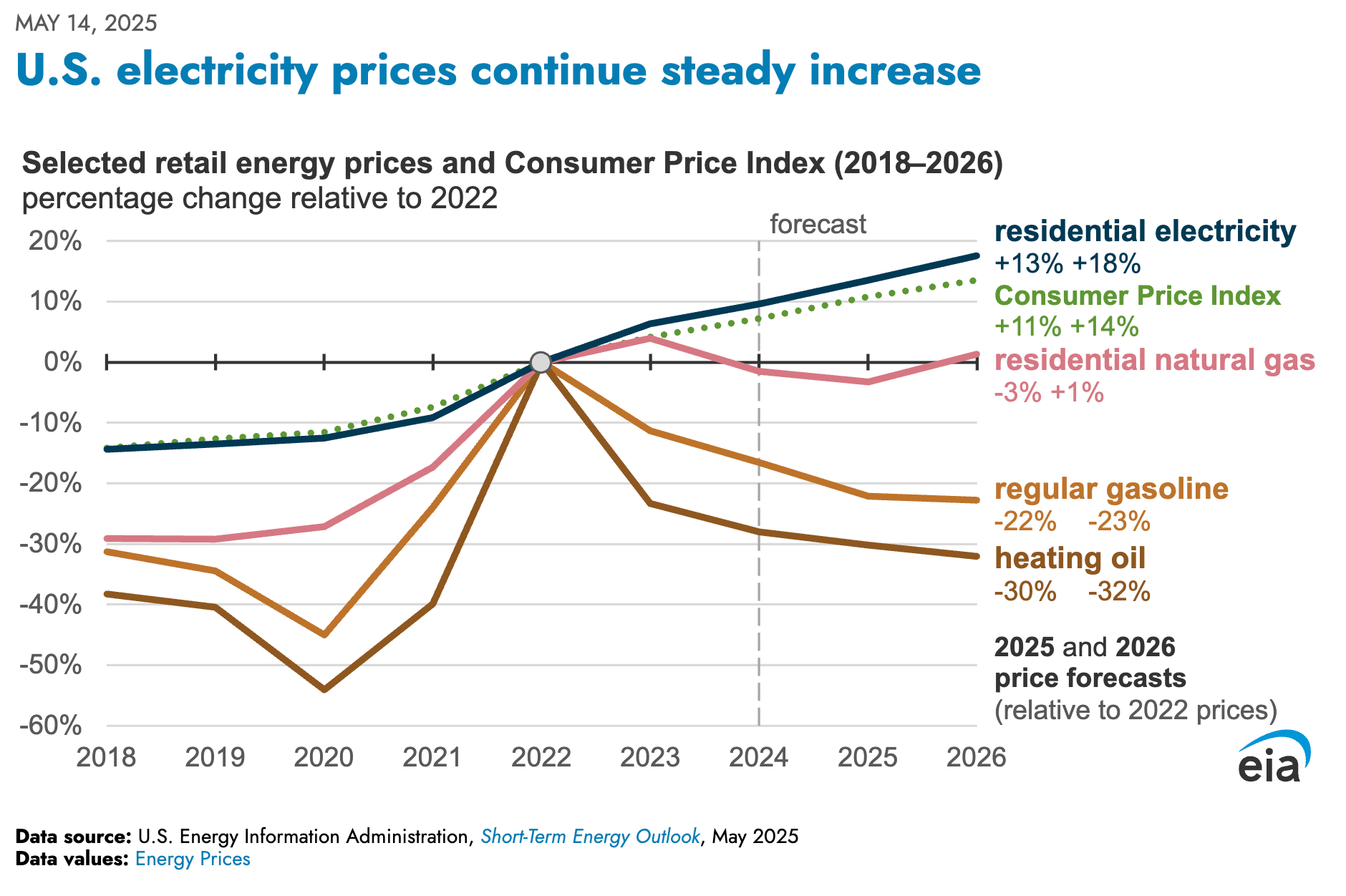

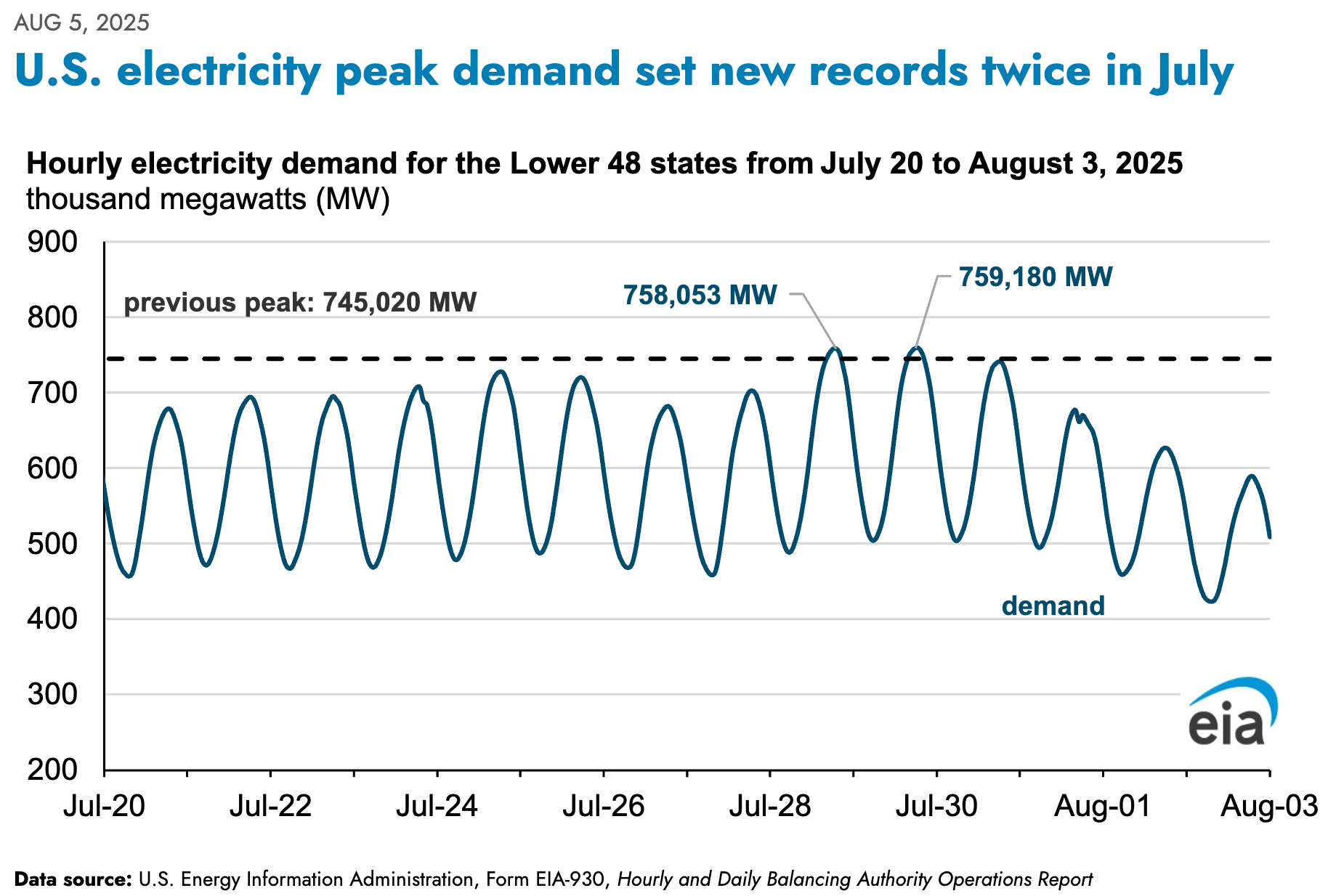

U.S. commercial electricity rates were stable from 2010 through 2020, but over the last five years, rates have increased nearly 30% as utilities address aging infrastructure and record electricity demand. The average wait time for a grid connection across the U.S. is now four years. Power delays remain a significant hurdle in alleviating supply constraints. However, there is a silver lining: this obstacle is also preventing a bubble from forming in the sector. Utilities have been increasing the requirements for power requests, including larger deposits and minimum contract payments. These are positive actions that will help remove speculation from the queue and accelerate legitimate projects. Behind-the-meter solutions leveraging natural gas turbines are seeing increasing implementation. Looking farther ahead, small modular reactors present significant opportunity for clean energy.

Data centers are one component of a complex global power dilemma. Increasing adoption of EVs, the electrification of machinery, rising power consumption in developing countries and a myriad of other factors are all contributing to increased global power consumption.

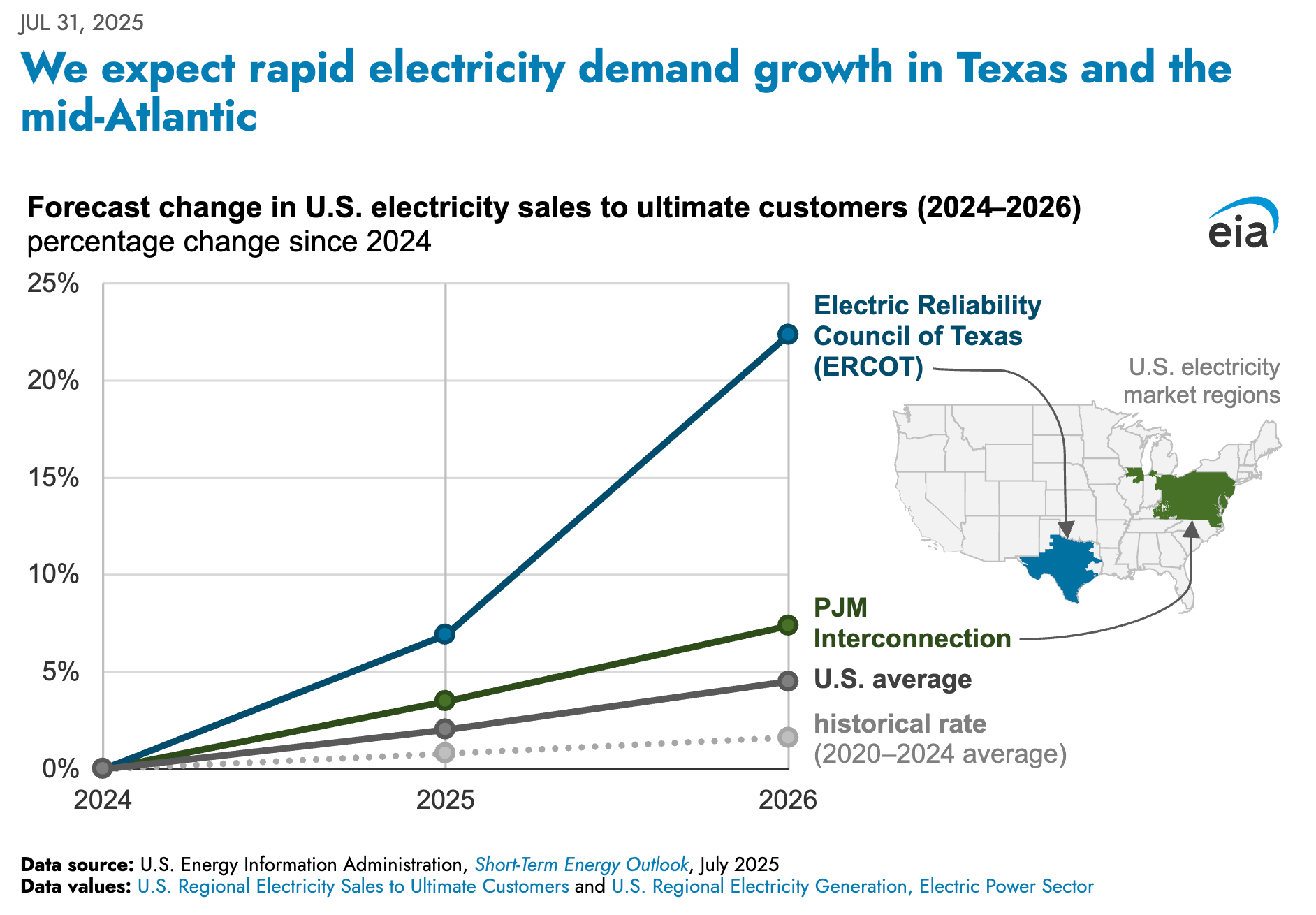

EIA: We forecast nationwide U.S. retail electricity sales to ultimate customers will grow at an annual rate of 2.2% in both 2025 and 2026, compared with average growth of 0.8% between 2020 and 2024. The forecast reflects rapid electricity demand growth in Texas and several mid-Atlantic states, where the grid is managed by the Electric Reliability Council of Texas (ERCOT) and the PJM Interconnection, respectively. We expect electricity demand in ERCOT to grow at an average rate of 11% in 2025 and 2026 while the PJM region grows by 4%.

After relatively little change in U.S. electricity demand between 2005 and 2020, retail sales of electricity have begun growing again, driven by rising demand in the commercial and industrial sectors. Developers have proposed numerous data centers and large manufacturing facilities that could consume significant amounts of electricity, and many of these projects are concentrated in the ERCOT and PJM regions. But, the timing of these facilities’ initial operations remains uncertain.

We publish short-term forecasts for electricity sales to ultimate customers for each of the nine census divisions and for the entire United States. We directly incorporate ERCOT’s and PJM‘s monthly projections for power demand into our sales forecasts for the relevant regions. The portion of the power grid that ERCOT operates is located within the West South Central Census Division, which consists of Texas and three neighboring states: Oklahoma, Louisiana, and Arkansas. In Texas, electricity is delivered to end-use customers by four large investor-owned utilities and several municipal utilities.

Business Insider: Amid the scramble to capitalize on the economic transformation promised by AI, cities and states give away millions in tax breaks to build data centers, with relatively few full-time jobs promised in return. In Ohio, tax breaks given to developers can amount over time to more than $2 million in tax savings for every permanent, full-time job at an operational data center, Business Insider's analysis found. And new local ordinances allow data centers to be built cheek-by-jowl with residential neighborhoods, leaving locals to live next to industrial complexes that operate 24/7.

This unprecedented build-out comes at an extreme cost. The 322 data centers in Business Insider's count that are among the very largest data centers can consume as much power as a city and up to several million gallons of water a day.

Unlike farmers or golf courses that have learned to make do with recycled water, data centers that do use water for cooling overwhelmingly rely on fresh supplies.

Collectively, Business Insider estimates that US data centers could soon consume more electricity than Poland, with a population of 36.6 million, used in 2023.

Texas Tribune: Large data centers can require 100 MW or more each, consuming the same amount of power per year as 350,000 to 400,000 electric cars, according to the International Energy Agency. Put another way, a larger facility can use as much electricity as a medium-sized power plant, the U.S. Energy Information Administration estimates.

Texas has seen a rapid increase in data capacity thanks to the state’s relatively cheap energy prices, the ease with which facilities can connect to the grid and its overall business-friendly tax and regulatory environment.

Companies generally employ around 50 to 150 or more employees in each data center, in addition to an array of building and maintenance contractors, according to the Data Center Coalition, which estimates that each job in a data center supported six jobs elsewhere in the economy.

The state had 279 data centers as of September 2024, according to the Texas Comptroller. The Dallas-Fort Worth area has about 141 of those.

That translated to 591 MW of power leased by data centers in Dallas and Fort Worth last year — the second most in the country — and nearly 190 MW in Austin and San Antonio, according to a CBRE report.

The Electric Reliability Council of Texas, the state’s primary grid operator, estimates that 1 MW of electricity can power roughly 200 homes.

Texas LSG: ERCOT’s peak demand will nearly double by 2030. Worst case scenario: demand could outpace supply as soon as 2027. Without proactive infrastructure planning, the state’s ability to reliably power homes and businesses could be in jeopardy. Peak demands once seen as emergencies—like those during Winter Storm Uri or last summer’s record-breaking heat—pale compared to anticipated demand.

Texas.gov

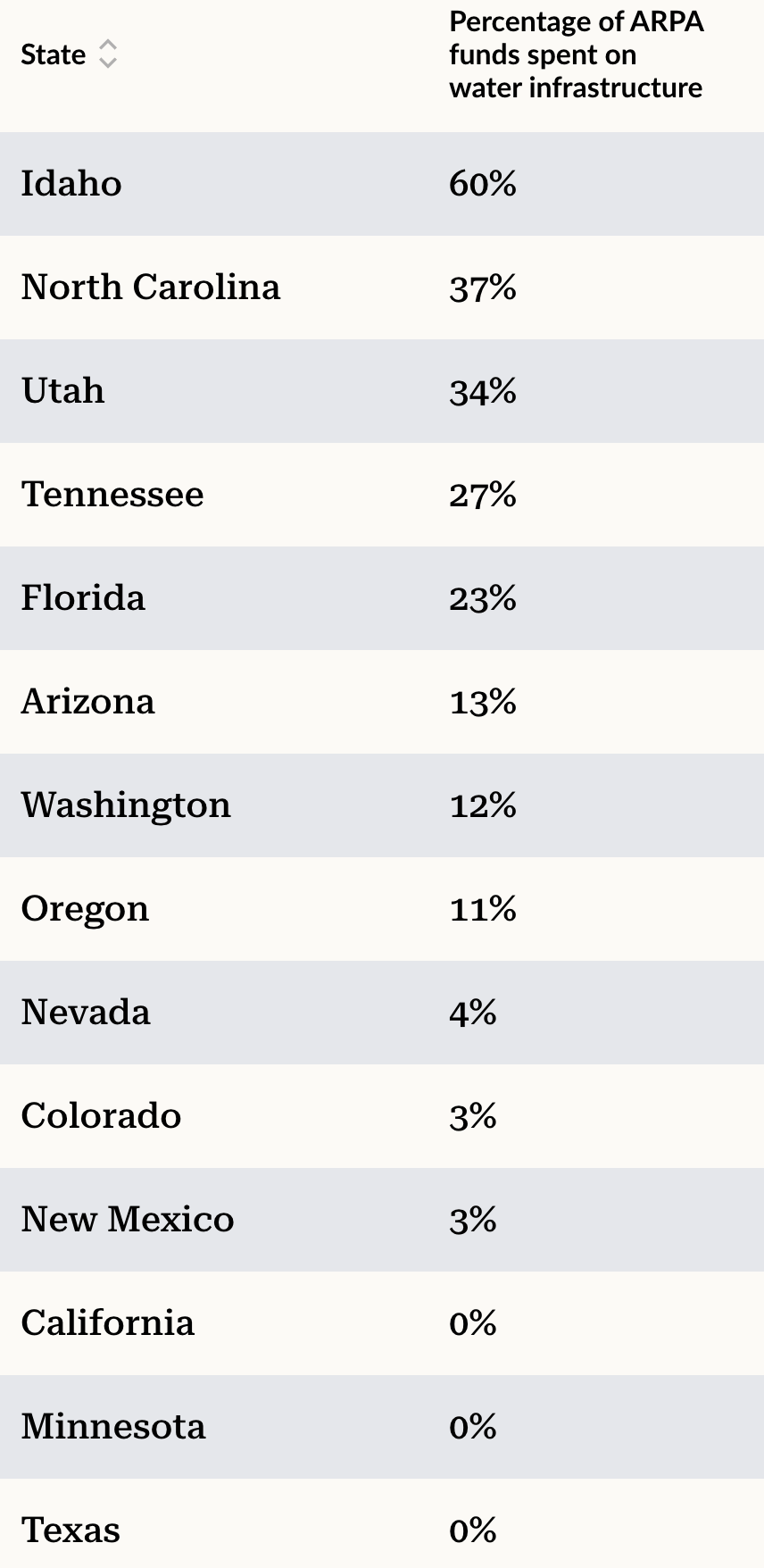

The United States’ water utilities have been underfunded for decades, leaving state and local governments with significant capital needs in the years ahead to repair and replace aging drinking water, wastewater, and stormwater systems. For some states, the American Rescue Plan Act’s (ARPA’s) State and Local Fiscal Recovery Funds (FRF) program is helping to provide a critical down payment toward upgrading their water infrastructure.

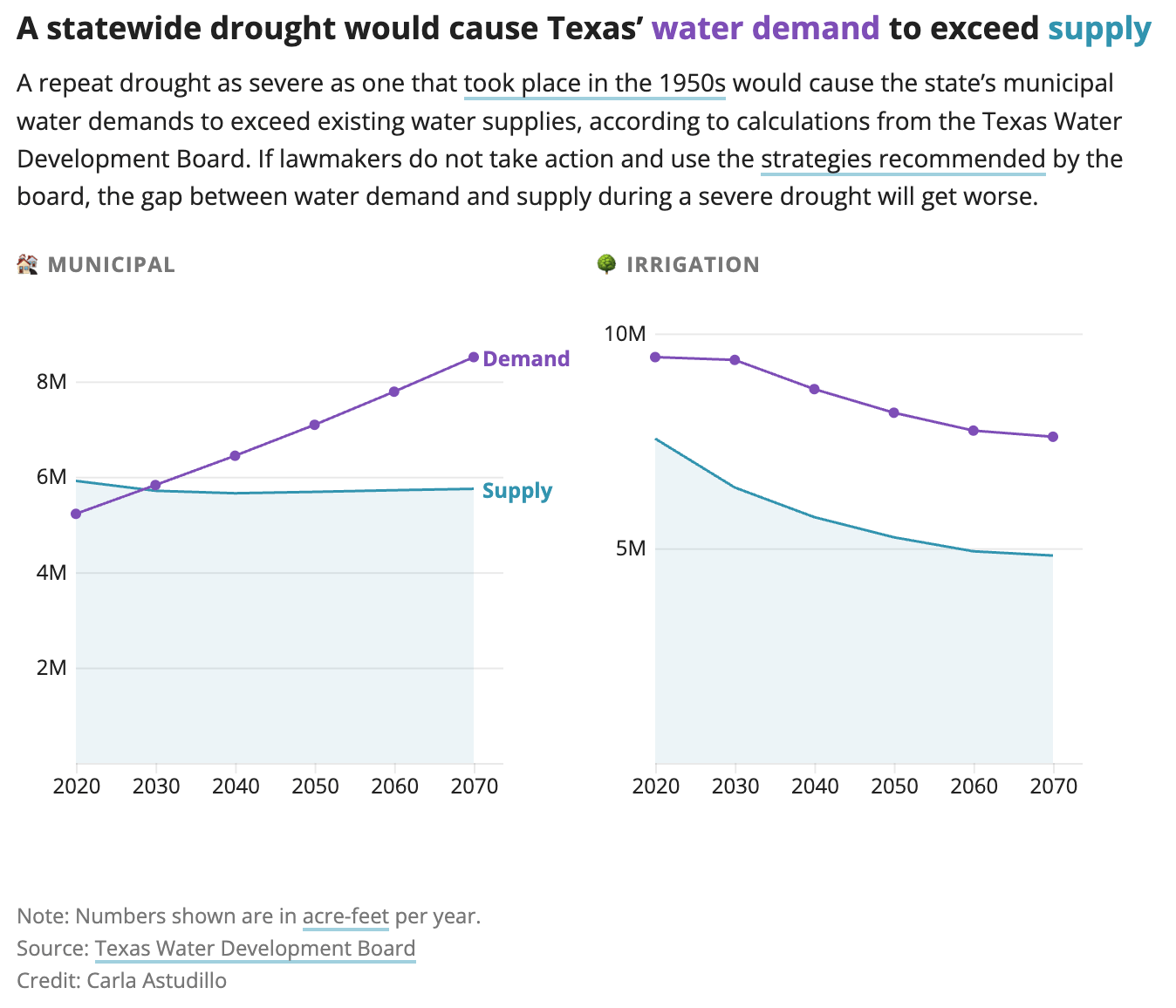

Texas Tribune: Texas officials fear the state is gravely close to running out of water.

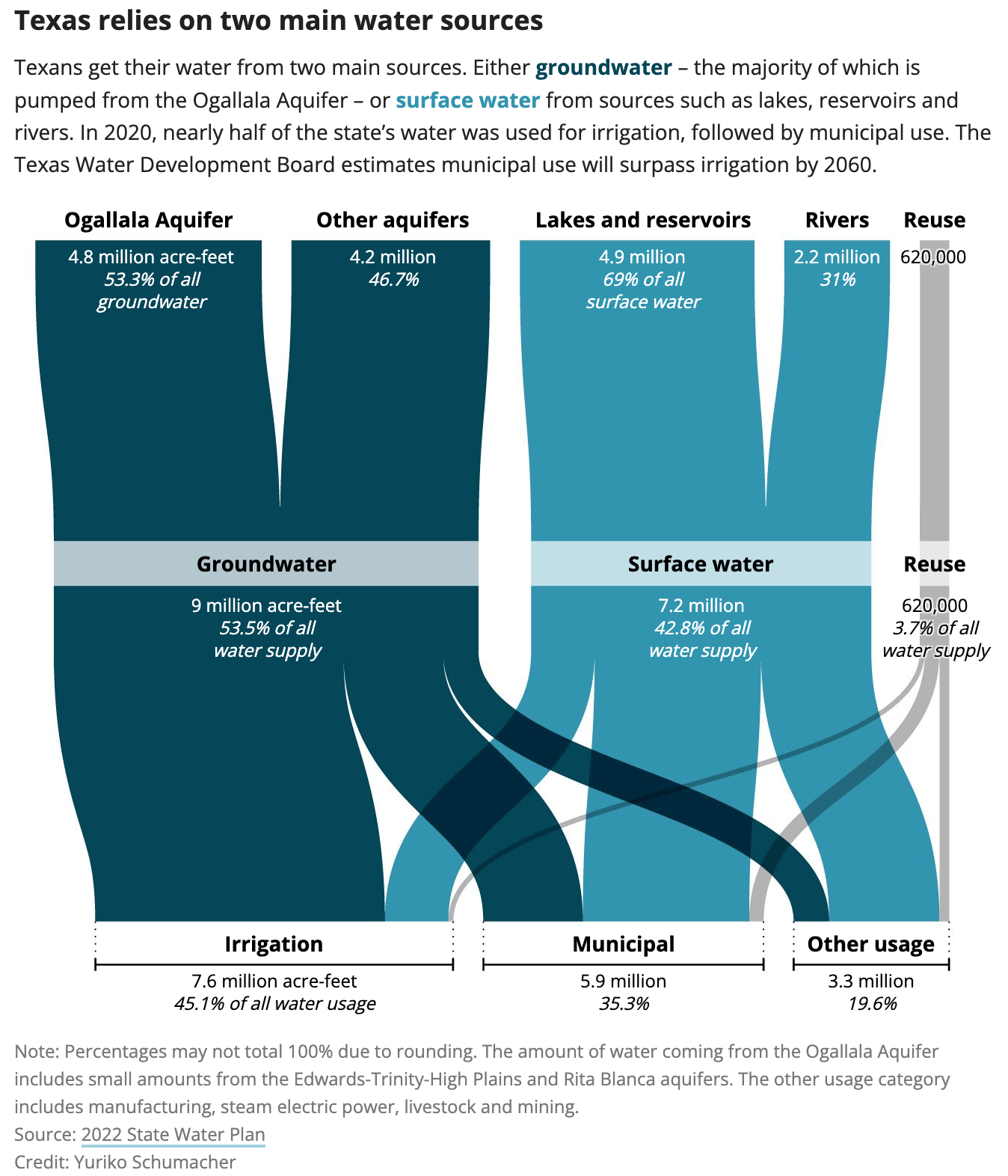

Towns and cities could be on a path toward a severe shortage of water by 2030, data compiled in the state's 2022 water plan by the Texas Water Development Board indicates. This would happen if there is recurring, record-breaking drought conditions across the state, and if water entities and state leaders fail to put in place key strategies to secure water supplies.

At risk is the water Texans use every day for cooking, cleaning — and drinking.

Unlike groundwater, surface water belongs to the state. To use it — whether it’s for cities, farms, or businesses — you need a permit from the state’s environmental agency, the Texas Commission on Environmental Quality.

Texas follows a “first in time, first in right” system, meaning older water rights take priority. In a drought, those with senior rights get water first, and newer users might be cut off entirely.

“Think of it like a sold-out concert,” said Rubinstein, a former chair of the Texas Water Development Board. “There are no more tickets. The only way to get more water is to build new storage, but that’s easier said than done.”

Texas’ two separate legal systems for water — one for groundwater and one for surface water — makes management tricky. Dupnik, the water board administrator, said Texas is unique in having the system divided this way. Just nine states, including Texas, have this two-tiered system.

The 2022 Texas Water Plan estimates the state’s population will increase to 51.5 million people by 2070 — an increase of 73%. At the same time, water supply is projected to decrease approximately 18%. The biggest reduction is in groundwater, which is projected to decline 32% by 2070.

This shortfall will be felt most in two major aquifers: The Ogallala Aquifer, as a result of its managed depletion over time, and the Gulf Coast Aquifer, which faces mandatory pumping reductions to prevent land sinking from over-extraction.

Texas is not only losing water to overuse. The state’s aging water pipes are deteriorating, contributing to massive losses from leaks and breaks.

A 2022 report by Texas Living Waters Project, a coalition of environmental groups, estimated that Texas water systems lose at least 572,000 acre-feet per year — about 51 gallons of water per home or business connection every day — enough water to meet the total annual municipal needs of Austin, El Paso, Fort Worth, Laredo and Lubbock combined.