- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 10.04.2025

Location Strategy Chartbook 10.04.2025

Real Estate Market Insights

For each week of a shutdown, the direct effect of furloughed federal workers would reduce fourth-quarter annualized real GDP growth (quarter-on-quarter) by about 0.15 percentage points, according to Goldman Sachs Research. Reopening would result in an equally sized positive effect on growth in the first quarter, assuming the shutdown ends before then.

That estimate assumes the shutdown affects around 900,000 federal employees and generally follows the same pattern as prior shutdowns. If the Defense Department or other agencies can fund some operations from other sources, the effect on growth would be slightly smaller, Goldman Sachs Research economists Alec Phillips and Ronnie Walker write in a report.

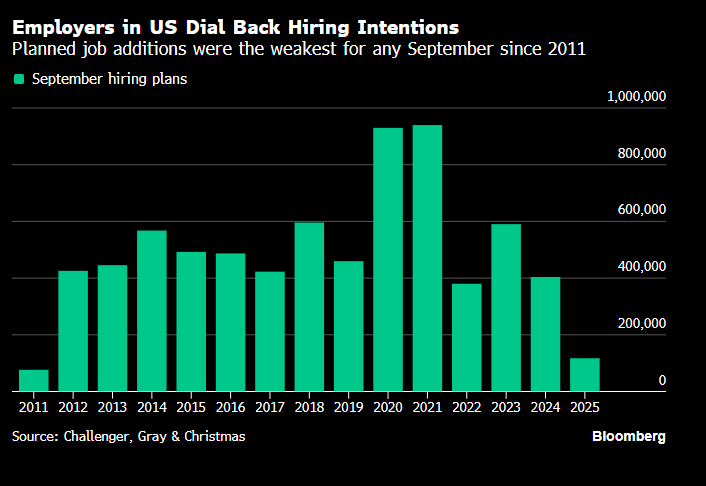

US employers dialed back hiring plans in September and announced fewer job cuts, according to data from outplacement firm Challenger, Gray & Christmas. Companies last month announced plans to add 117,313 jobs, down 71% from a year earlier and marking the weakest September for hiring intentions since 2011.

The report released Thursday noted a significant slowdown in seasonal hiring plans compared to years past. From January through September, US-based employers announced plans to add nearly 205,000 jobs, the weakest year-to-date stretch since 2009.

Meanwhile, firms announced plans last month to cut 54,064 jobs, down almost 26% from a year ago and fewer than the 85,979 announced in August. Planned cuts don’t necessary translate into immediate layoffs. The report shows a labor market in which there is both limited hiring and firing. Economists and policymakers will be relying more on private reports such as the Challenger data for clues about the labor market and broader economy in the absence of official data because of the US government shutdown.

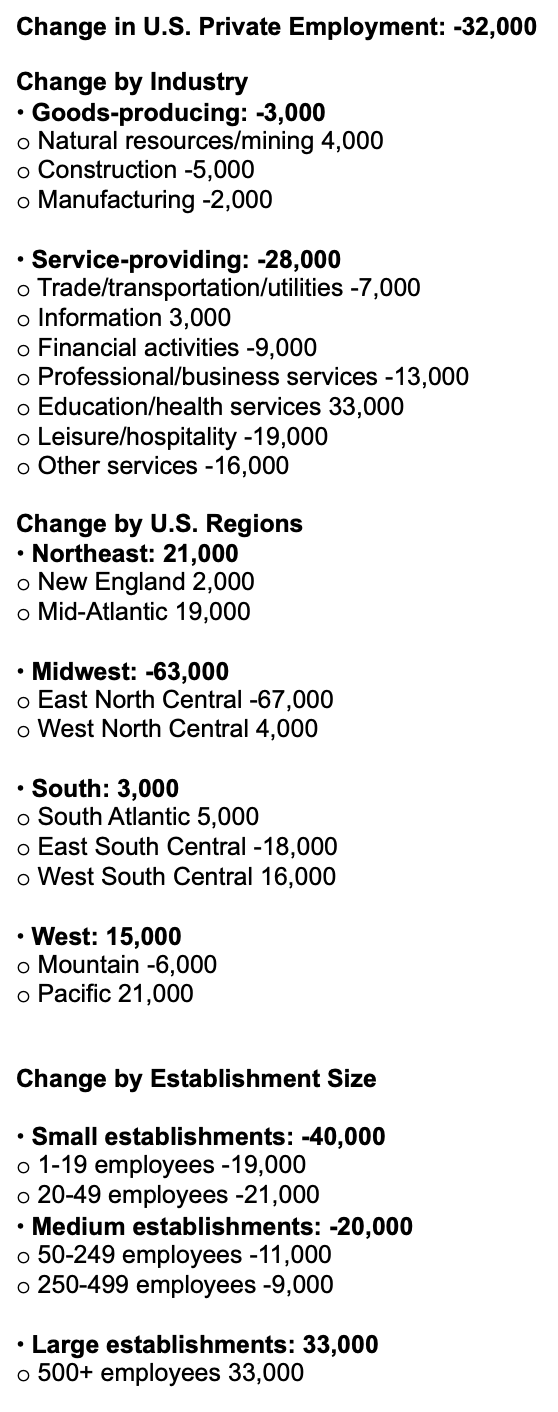

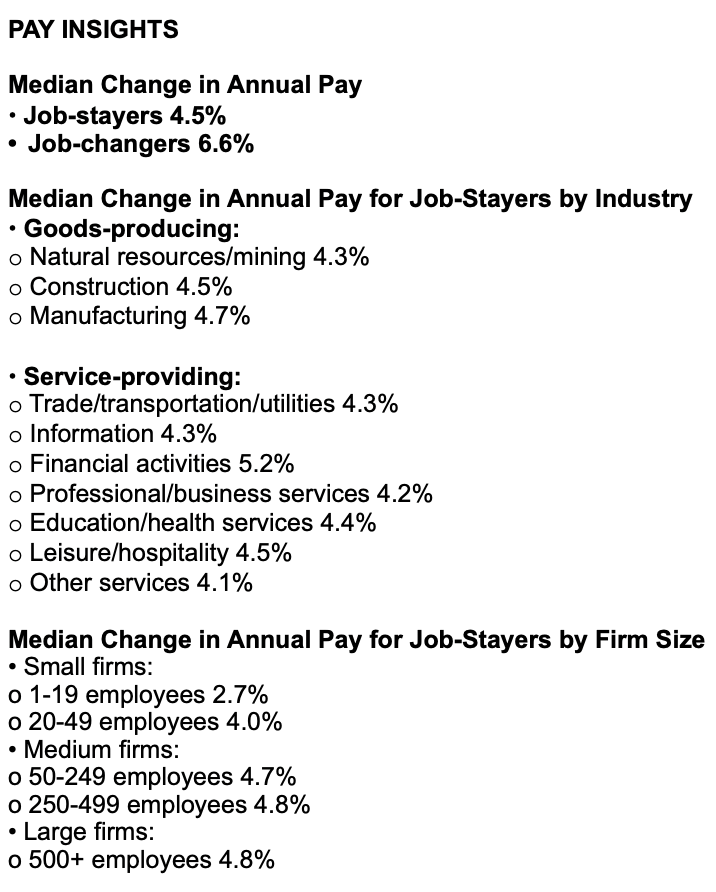

ADP: Private sector employment shed 32,000 jobs in September and pay was up 4.5 percent year-over-year according to the September ADP National Employment Report® produced by ADP Research in collaboration with the Stanford Digital Economy Lab (“Stanford Lab”). The ADP National Employment Report is an independent measure of the labor market based on the anonymized weekly payroll data of more than 26 million private-sector employees in the United States. ADP’s Pay Insights captures nearly 14.8 million individual pay change observations each month. Together, the jobs report and pay insights use ADP’s fine-grained data to provide a representative and high-frequency picture of the private-sector labor market. “Despite the strong economic growth we saw in the second quarter, this month's release further validates what we've been seeing in the labor market, that U.S. employers have been cautious with hiring,” said Dr. Nela Richardson, chief economist, ADP

American consumers have shaken off the uncertainty of the year's first half with a summer spending spree that has left many economists revising earlier projections upward.

Consumer spending in August posted its third consecutive, monthly inflation-adjusted increase, with particular strength coming from discretionary and recreational spending. This was bolstered by high-income households enjoying the wealth effect of higher equity and home prices, which has allowed them to up their spending.

Consumer spending advanced 0.35% on an inflation-adjusted basis over August, after an upwardly revised 0.38% gain in July and a 0.26% rise in June, according to the U.S. Bureau of Economic Analysis’ high-profile monthly Personal Consumption Expenditures data release.

WSJ: Federal Reserve rate cuts aren't great for the biggest banks, which tend to lose out on revenue from cheaper loans. But they actually help regional banks—such as Ally, Comerica, Fifth Third—that typically have higher funding costs and hold more fixed-rate credit, like auto or commercial real estate loans. That could prompt a shift to smaller lenders after significant outperformance by bigger banks this year.

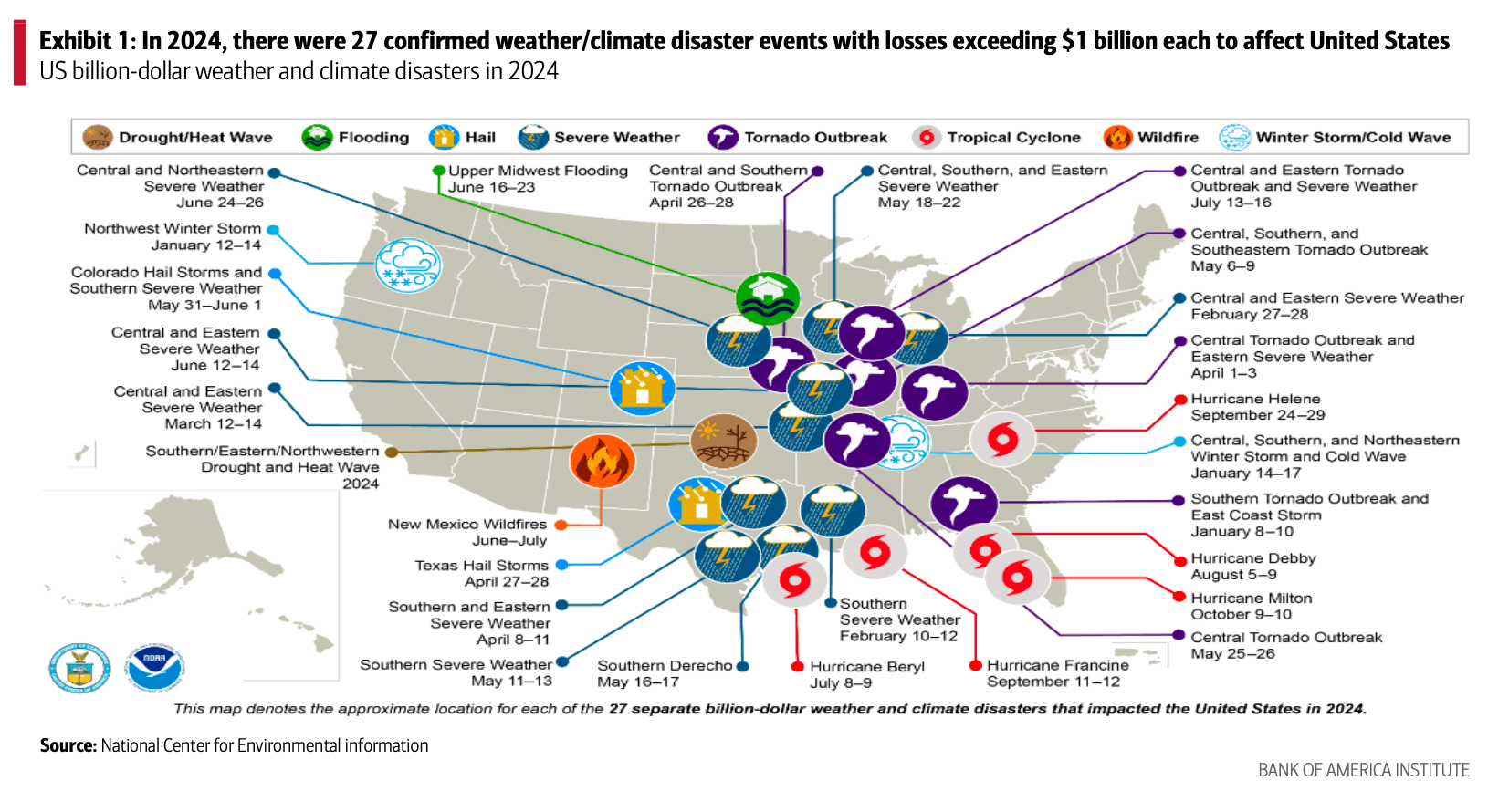

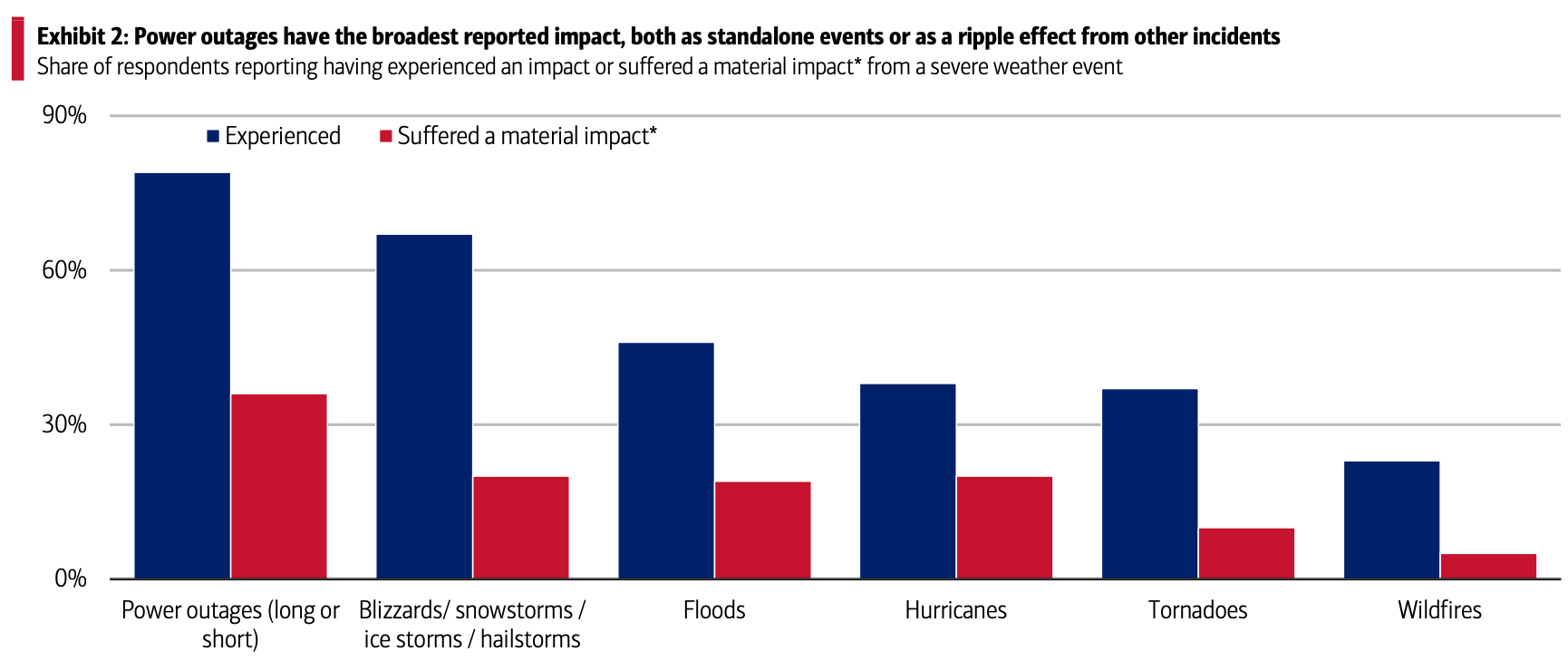

A major climate disaster in the US was declared every four days in 2024.

Climate-driven disasters in the United States are becoming more common and more costly. According to the National Center for Environmental Information, the US sustained 27 natural disasters where overall damages/costs reached or exceeded $1 billion in 2024. And roughly 137 million people – or around 41% of the US population – were living under a major disaster or emergency declaration at some point in the year.

In 2024, the US saw 90 major disaster declarations from the Federal Emergency Management Agency (FEMA) - nearly double the 30-year average of 55. These events affected roughly 41% of the population and have caused over $2.9 trillion in damages since 1980.

According to a Bank of America proprietary survey, insurance premiums rose by an average of $921 annually for those affected by natural disasters. The associated increase in insurance costs could change which areas homebuyers consider affordable or desirable.

Natural disasters can accelerate financial instability as well as impede economic recovery, particularly for small businesses and households in more vulnerable communities. Following Hurricane Helene and the LA wildfires, spending on home improvement and lodging rose sharply in affected areas, according to Bank of America aggregated card data, forcing people to spend on rebuilding and therefore constraining household budgets.

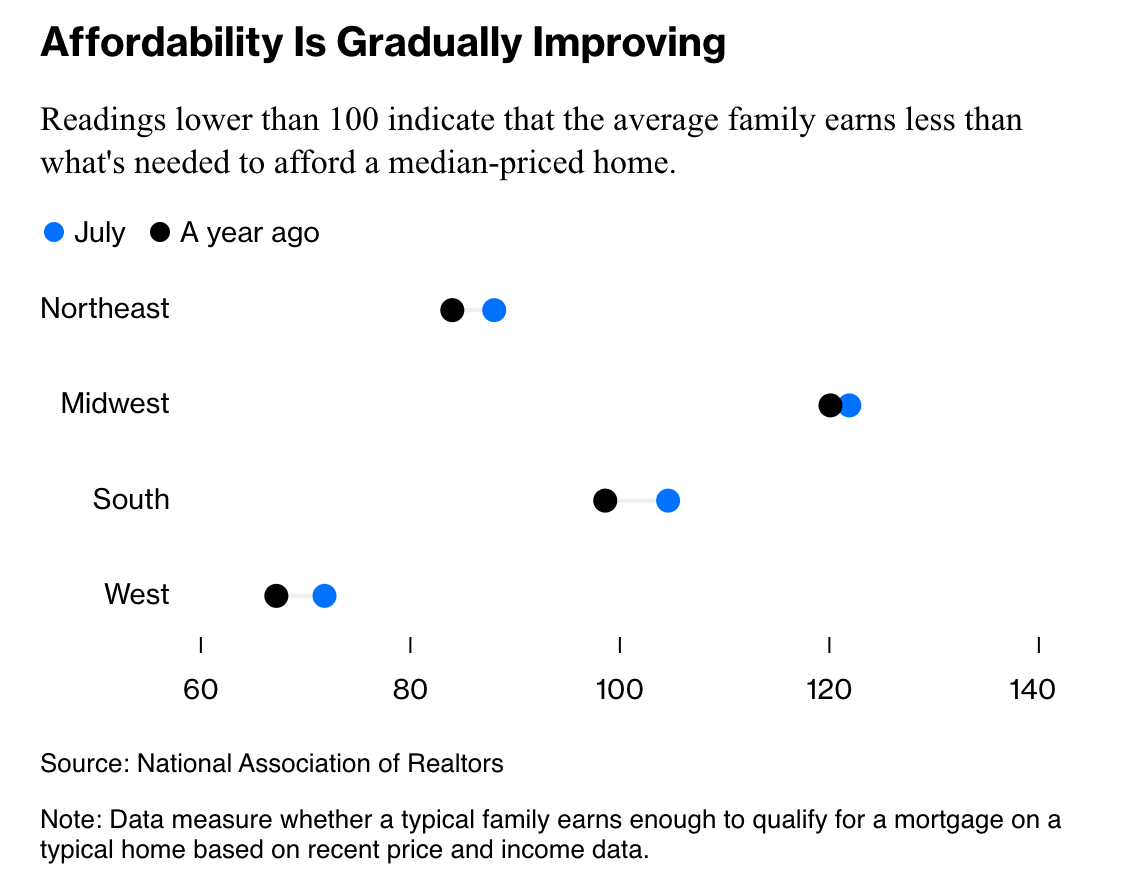

The buyers' strike of the past three years is finally working, but the path to better affordability looks painful for many of those trying to sell a home, the construction industry and the US economy.

California, Texas, and New Jersey are notable states where homebuyers face increased insurance costs.

Climate risks are also likely impacting homebuying decisions, and a 2024 analysis from Redfin found that low-risk homes across three major climate categories—heat, fire and flood—gained value faster than high-risk homes for the first time in 14 years. And with insurance costs skyrocketing, many risky areas that were once affordable have become expensive.

For example, homeowners who experienced a severe weather or natural disaster event saw their insurance premiums increase an average of $921 per year, according to the Bank of America survey. Furthermore, more than 10% of households in California, Texas, New Jersey and Georgia saw their insurance payments increase >$2000 in 2025, according to Bank of America payments data. And notably Georgia has seen insurance payments as a percentage of income rise to 6% this year. That is not only one percentage point (pp) higher than the US median but also more than Florida, South Carolina, Nevada and Texas. The severity and frequency of natural disasters – and ever rising insurance costs – could change which areas homebuyers consider affordable or desirable.

Beyond households, small businesses are also severely impacted by natural disasters. According to Small Business Administration disaster loan data for FY2022, the average total approved loan was only just over about half the average business total verified loss. Furthermore, FEMA estimates that 40% of small businesses never reopen after a natural disaster, and the SBA finds that figure is closer to 90%. 2 According to the Bank of America proprietary survey (same as previously mentioned), small business owners were significantly more likely than the general population to report negative financial and economic impacts from a severe weather event or natural disaster. In fact, Bank of America small business account data found deposits for those small businesses directly impacted were at their lowest point of 2024 following Hurricane Helene, down 7% from the annual average. Still, of the 96% of western North Carolina small businesses impacted by Hurricane Helene, a local survey found 93% of small businesses are now open. Only about 7% have yet to reopen in 2025

According to the Government Accountability Office, the concurrent nature of disasters, limited disaster workforce capacity, and undertrained surge responders pose challenges to federal agencies responding to environmental emergencies. For example, following Hurricanes Helene and Milton, only 4% of FEMA’s incident management workforce was available to deploy as of November 1, 2024.

BofA Global Research noted additional cuts to FEMA proposed by the current administration could affect state governments whose budget costs would rise to pay for emergency and disaster response jobs previously held by federal employees. Plus, recent FEMA workforce reductions could determine how effective the federal response is to future high-impact disasters. At the same time, cuts at the National Weather Service could further impair emergency managers’ ability to respond to fast-moving disasters. For small businesses and consumers alike, the growing force and economic fallout from the increasing frequency and nature of natural disasters will continue to shift economic outcomes

Bloomberg: There are now more completed new homes on the market than at any time in the past 16 years, and active housing inventory for sale is above 2019 levels in 14 states.

The normalization back toward 2019 levels of affordability will continue as pricing responds to supply, and how much house prices fall will determine the stress in the construction industry.

Progress has been much slower when it comes to increased buying power, based on a mix of income growth, borrowing costs and home prices. Nationally, there’s been a 10% improvement in affordability from 2023’s low point, according to figures from First American Data & Analytics. But the company’s Real House Price index is still 74% above the five-year, pre-pandemic average. The level of relief families are seeing depends on where they live, though.

A Florida law taking effect this week that repeals a decades-old sales tax on commercial leases is expected to save tenants across the state $900 million annually and pave the way for new deals and business expansions.

The new law, which was officially signed by Gov. Ron DeSantis in June and went into effect Oct. 1, eliminates the state’s business rent tax and county surtaxes on commercial leases. That means Florida has finally joined the rest of the country after decades of being the only state to levy a tax of this kind since the 1960s, said Mike Griffin, co-head of the Florida region and Tampa-based vice chairman for Savills, in an interview with CoStar News.

“We've had this bogey out there as being this outlier that we don't want to be, which is charging sales tax on commercial leases … this is just a bad tax," Griffin said.

The tax didn’t just apply to base rent but included additional charges that were passed onto the tenant, such as fees for common area maintenance, utilities, insurance, real estate taxes and property management.

Further complicating the issue were county surtaxes. While Florida’s commercial lease sales tax was 6% in 2017, and gradually lowered to 2%, counties were able to levy their own taxes on commercial leases over the state’s.

Momentum in Houston's office investment market continued to build through the first three quarters of 2025, following a steady recovery throughout 2024.

The third quarter of 2025 saw the second-highest number of transactions on record, suggesting that investor activity is holding firm despite uncertainty for the broader economy and the future of office demand. Roughly 307 office properties were sold during the quarter, according to CoStar data, the highest quarterly figure behind only the fourth quarter of 2021, when 334 properties traded.

Institutional investors have been net sellers of office since 2021. Traditionally, they accounted for roughly 40% of annual acquisition activity but represented just 5% of activity in the past year.

Private buyers and owner-users continue to dominate the buyer pool as they capitalize on deep discounts. Often, these groups are able to buy properties well below replacement. For example, in August, a private local investor purchased a 220,000-square-foot building at 801 Travis in downtown Houston for $12.1 million, or $54 per square foot. The 1981-built property was last renovated in 2014 and was 43% leased at the time of sale.

Price per pound is often a key driver for non-medical office transactions, but in the few cases where in-place income is primary, capitalization rates are typically between 8% and 9% for deals above $10 million, up 200 basis points from their peak valuations in 2021. For example, in August, the Dhannani Private Equity Group bought a 180,000-square-foot building on 2401 Fountain View Drive at a 9% cap rate. The 1981-built property was last renovated in 1999 and 81% leased at the time of sale.

Still, local brokers note that some five-star buildings in premier locations may prove to be exceptions to this range and can trade below 7%.

Medical office properties, favored due to their perception of reliable cash flow, according to market participants, have seen cap rates expand less in recent years. They are now in the 7% to 8% range, up about 100 to 150 basis points above their 2022 lows, and in some cases, can fall below 7%.