- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 10.18.2025

Location Strategy Chartbook 10.18.2025

Real Estate Market Insights

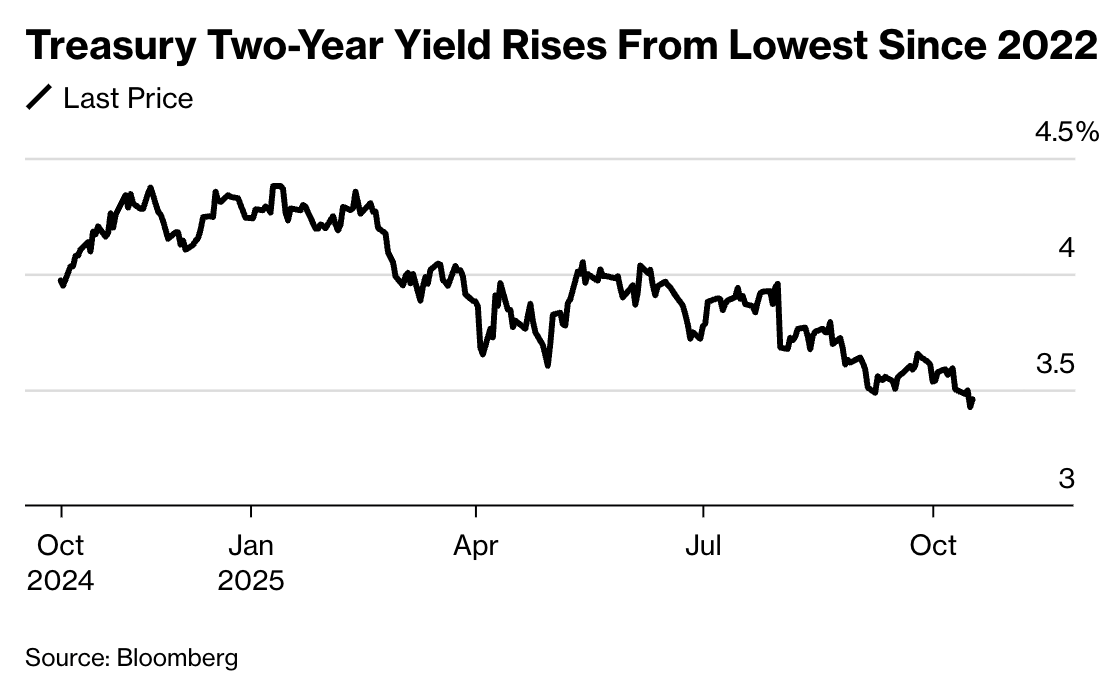

Even with little sign of resolution on the shutdown front, recent commentary from Federal Reserve speakers has spurred investors to add dovish exposure. “The lack of economic data does not seem to be a problem for the Fed and we expect another 25-basis-point rate reduction at the October meeting,” Morgan Stanley economists led by Michael Gapen said in a note.

The Current Activity Indicator, which measures present economic performance, fell to 1.6% in September based on preliminary data—down from 2.2% in August. The indicator, which contains a range of factors, has fallen for two consecutive months.

US consumer demand slowed last month. After assessing a broad array of high-frequency spending data such as credit-card borrowing and same-store sales, economists say shoppers dialed back purchases after retail activity. Bloomberg Second Measure, which analyzes credit and debit card data, showed there was less appetite last month for discretionary items such as furniture, electronics and appliances. Credit-card data from Bank of America also shows cooler demand.

A CNBC/National Retail Federation Retail Monitor showed that sales slowed on a monthly basis in September but year-over-year increases remain strong, and the Johnson Redbook Same-store Sales Index was up 5.7% in September from a year ago, compared with a 6.3% gain in August.

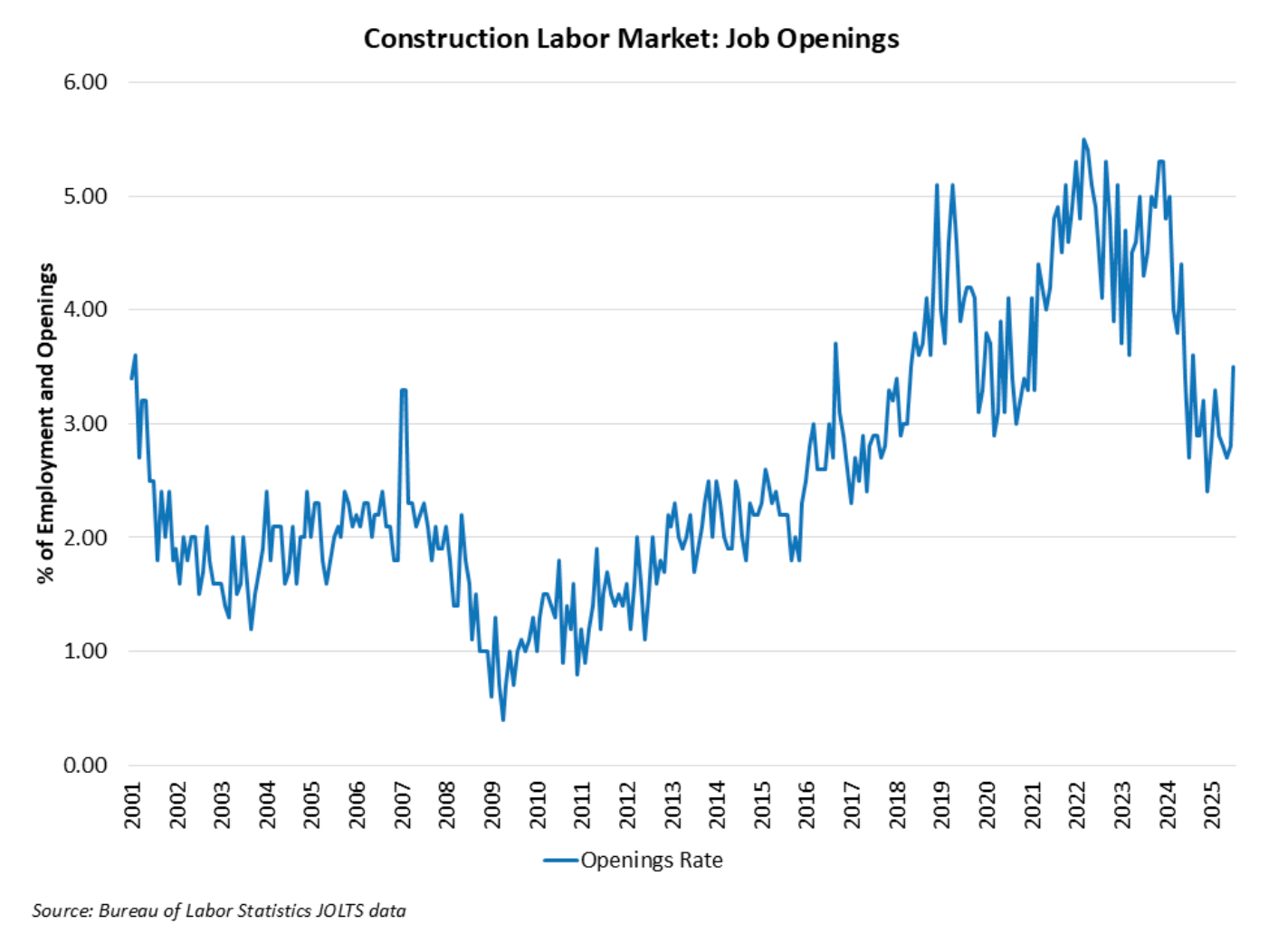

NAHB’s economics team found that the aggregate annual impact of the skilled labor shortage in the home building sector is $2.663 billion in terms of higher carrying costs and $8.143 billion in terms of lost single-family home building (19,000 homes). This represents a combined aggregate economic effect of $10.806 billion because of longer construction times associated with scarce skilled labor.

There are currently 3.3 million payroll residential construction workers.

Amid a dramatic slowdown in the job market, home builders and remodelers lost 26,100 jobs over the last 12 months.

Home building non-supervisory workers’ wages trended higher, rising 9.2% in July, substantially outpacing inflation and wage growth for the overall sector.

Women make up a growing share of the construction employment, reaching a 20-year high of 11.2% in 2024. This is a noticeable increase from 9.1% in 2017.

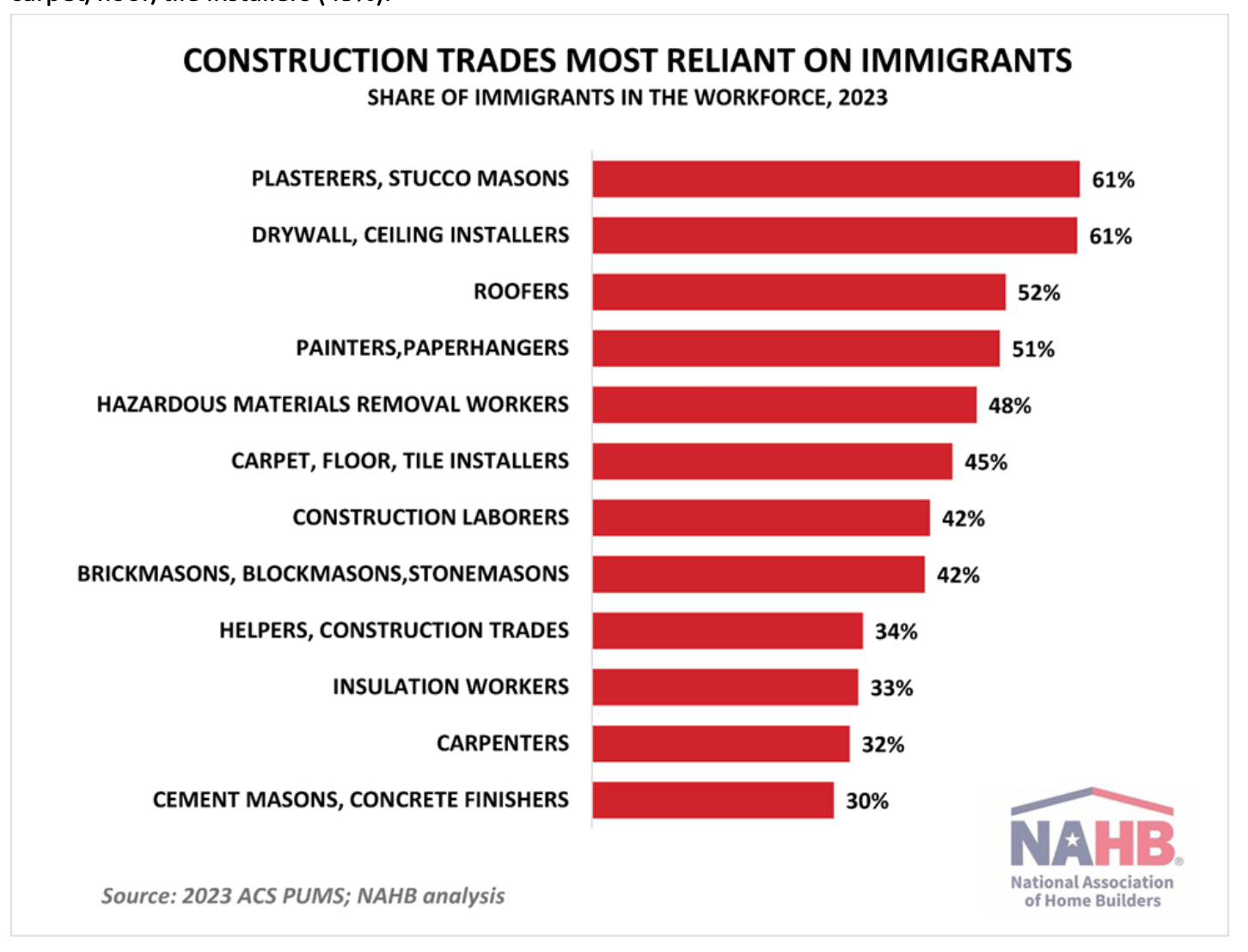

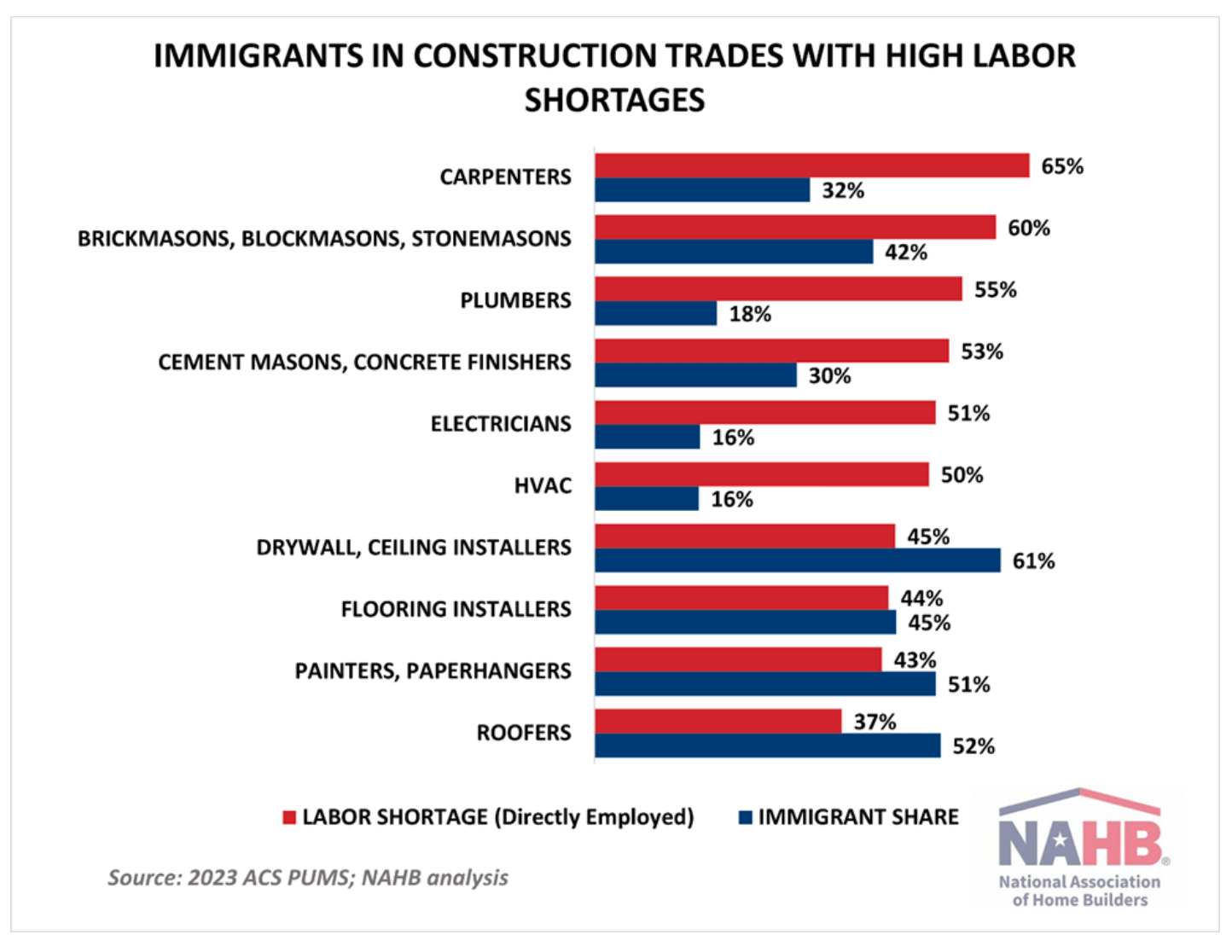

Immigrant workers now account for 25.5% of the construction workforce, a new historic high.

In construction trades, the share of immigrants is even higher, with one in three craftsmen coming from outside the United States.

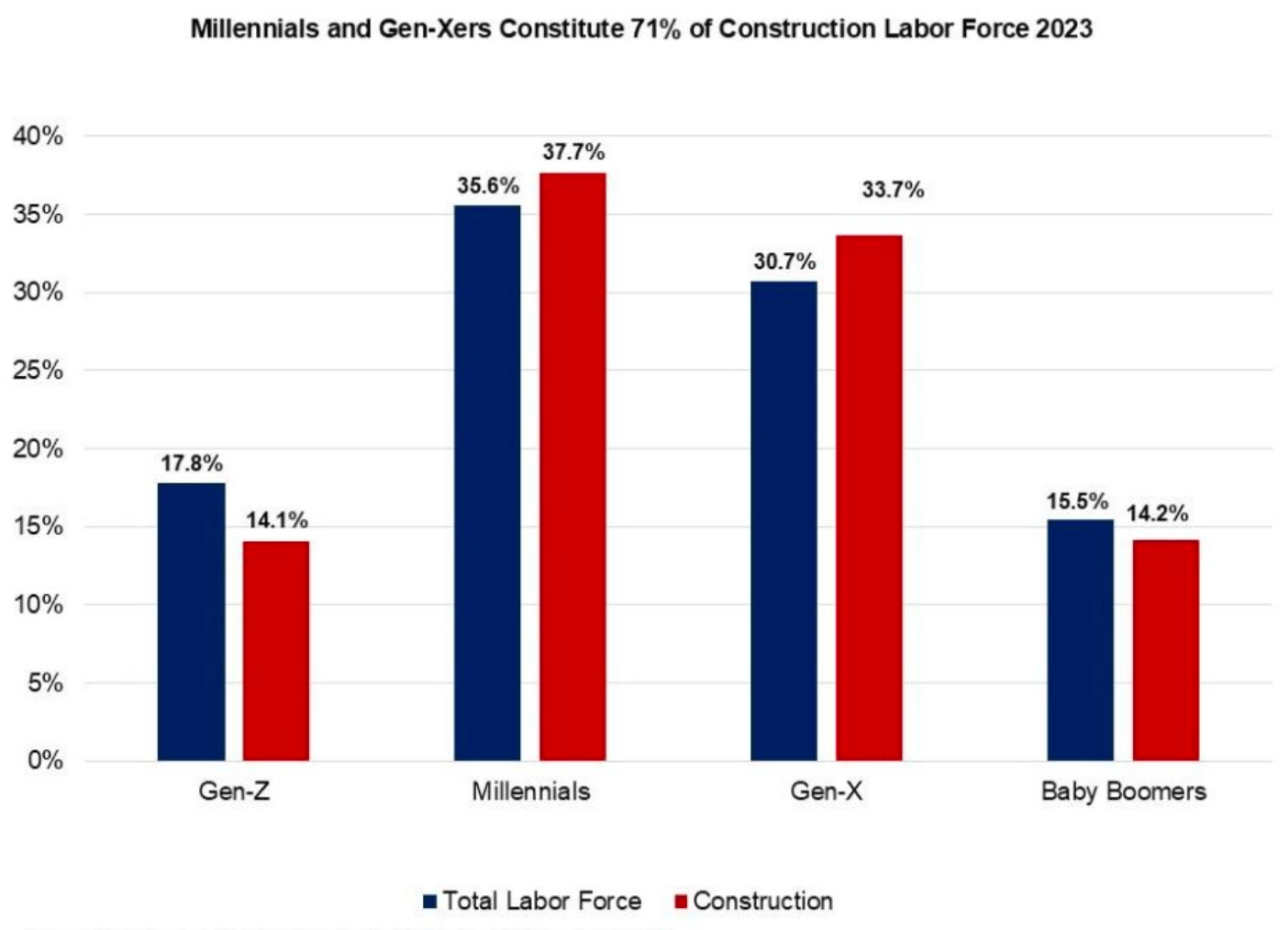

The percentage of Gen Z (those born between 1997 and 2012) individuals participating in the construction labor workforce has more than doubled, increasing from 6.4% in 2019 to 14.1% in 2023.

For the time being, the impact of AI on the home building industry is limited but is likely to evolve in the coming years.

Industrial tenants remain active in Houston, but like national trends, net absorption, or the difference between move-outs and move-ins, has slowed from the record post-pandemic demand surge.

Houston recorded 11.9 million square feet of net absorption over the past 12 months, now at its lowest annual mark in more than five years, and almost one-third of the average of 33 million square feet per year seen in 2021 and 2022.

Year to date, newer properties are overwhelmingly driving absorption. During the first three quarters of the year, properties 100,000 square feet or larger built since 2020 totaled roughly 8 million square feet of absorption.

In October, Pepsi moved into 1.1 million square feet at a 2023-built facility in I-10 West Trade Center. In September, Tesla moved into 1 million square feet at a 2022-built facility in Empire West Business Park. Both of these parks are in Brookshire, a city 40 miles west of the city of Houston. Its easy access to main highways makes it ideal for tenants looking to distribute regionally. More locally focused firms benefit from the area's proximity to fast-growing suburbs such as Katy, Cinco Ranch and Fulshear.

Large logistics users have shown a preference for newer buildings, often at the expense of older ones. These modern facilities often have the ceiling heights and power capacities that many large users need.

Net absorption has softened, as evidenced by the rise in years of supply for properties built in the past five years. As of the third quarter of 2025, Houston had six-and-a-half years of supply, the highest mark in five years.

Larger properties in Houston show the highest supply risk. Brokers note that demand remains strong for the smaller big-box properties, while larger ones are sitting on the market longer. CoStar's data echo this: Boxes larger than 250,000 square feet are now taking about 10 months to lease, almost double the time it took just two years ago. Meanwhile, properties between 100,000 square feet and 200,000 square feet are now taking roughly six months to lease, compared to four months, two years ago.

WARN notices reported to the Texas Workforce Commission point toward some looming risk for industrial-using employment: In one example, Accelore, a major contractor for Amazon, announced layoffs of over 200 workers.

The single-largest layoff occurred when e-commerce pet food giant Chewy announced in early March that it would be letting go nearly 700 employees at its fulfillment center in the Mountain Creek business park as part of an automation-oriented pivot. As of right now, the company has retained all of the 663,000 square feet of space within the park, with a lease expiration set for January 2027.

HelloFresh announced in March that it would be closing one of its local distribution centers in the second quarter, resulting in layoffs of nearly 275 workers. Earlier this year, the 138,000-square-foot cold storage space in the Tri-Temp Production Facility, leased by the company, was put back on the market as sublet space.

FedEx has seen over 400 layoffs across multiple sites. The largest of these occurred at its Fort Worth operation in the Alliance Gateway 19, where it occupies the entire 414,000-square-foot facility. Two additional layoffs on the other side of the Metroplex in Plano and Garland, totaling just over 130 jobs.

UPS announced earlier in the third quarter that it would be cutting roughly 60 jobs at its Dallas facility in the East Hines North industrial area.

Smurfit Westrock, announced that it would be discontinuing production at its containerboard mill located in Forney.

TT Electronics, which operated a facility in Plano Commerce Park, issued a notice that it would be laying off all 75 employees by the end of August. The company originally moved into this space in late 2022, with just over two-and-a-half years in the location.

Trophy hotels in prime destinations still command premium pricing over the past 18 months

The Ritz-Carlton Oahu, Turtle Bay | $680 Million

Residence Inn at Anaheim Resort | $179 Million

Hilton La Jolla Torrey Pines | $165 Million

The Stanley Hotel, Estes Park | $163 Million

Marriott Seattle Waterfront | $145 Million

The Clancy San Francisco | $115M set to close in November

New CA hotels in the pipeline

Hard Rock Hotel & Casino Tejon — Bakersfield | 400 rooms

Kimpton Garden Grove Anaheim — Orange County | 371 rooms

LaTerra Select Hotel — Burbank | 307 rooms

Autograph Collection Inglewood SoFi — Inglewood | 300 rooms

“Reflecting on 2024 performance, only the highest scales [of hotels] are seeing positive revenue per available room,” STR's William Anns said at the 2025 Hotel Data Conference

Luxury and upper-upscale hotels across the U.S. continue to outperform the lower segments.

“At the top end, recovery now is quicker than during the Great Financial Crisis, in which independent [hotels] took 27 months to recover, upper midscale, 35 months, and luxury, nine,” he said. “Demand again is aligned to consumer price index, but the ultra-wealthy are spending more on high-end hotels than on high-end retail.”

The American middle class has been most affected by inflation, tariffs and rising costs. This has led to slightly lowered or flat hotel performance in those mid-tier segments, Anns said.

Business travel is also down across U.S. hotels.

“Occupancy has fallen across all days of the week, not by a great amount, between 0% and low 1%. The Monday-to-Thursday conference has been shortened by a day, and there is a little less bleisure travel because of this,” he said.

Shopping centers anchored by Whole Foods are selling for as much as four times the rate of properties anchored by mass-market rivals, according to new CoStar data.

Properties featuring the upscale grocery chain sold for an average of $415 per square foot through September 2025, representing a 41% increase from the prior year and solidifying Whole Foods' position at the top of the grocery-anchored retail sales price list. The sale of Whole Foods-anchored centers significantly outpaced the industry average of $199 per square foot for other grocery-anchored properties.

Following Whole Foods, Safeway-anchored centers averaged $265 per square foot, while Trader Joe's properties fetched $253 per square foot. The Fresh Market rounded out the top tier at $243 per square foot.

On the other end of the spectrum, centers anchored by value-oriented retailers traded at significantly lower prices. Kroger-anchored properties averaged $97 per square foot, while Walmart and Food Lion both came in at $102 per square foot.

Overall, the grocery-anchored sector has shown robust growth, with average prices climbing 18% year over year.

Some notable chains bucked the upward trend. Target-anchored centers saw the steepest decline, falling 35% to $122 per square foot. Kroger properties dropped 22%, while Trader Joe's centers declined 8% despite the chain's cult following among consumers.

The strongest performer in percentage terms was BJ's Wholesale Club, which saw prices surge 54% to reach $149 per square foot. Aldi also posted strong gains, rising 23% to $151 per square foot as the discount grocer continues its aggressive expansion across the United States.

Regional grocers showed mixed results, with ShopRite properties climbing 10% to $237 per square foot. Hy-Vee centers declined 10% to $151 per square foot, while Publix, the dominant southeastern grocer, saw a modest 4% decline to $207 per square foot.