- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 10.25.2025

Location Strategy Chartbook 10.25.2025

Real Estate Market Insights

The market-implied odds of a quarter-point rate cut next week are 99%.

It’s safe to say that the main reason U.S. jobs and inflation data have been watched so closely is because they helped investors everywhere guess the moves of the world’s most powerful central bank. Weak jobs reports have sometimes sent stocks higher, and vice versa. But inflation, including a separate price gauge the Fed prefers, worries rate-setters less than it used to.

Economists polled by The Wall Street Journal think September’s report will bring the year-over-year price change to 3.1%, which is well above the Fed’s 2% target. Since unemployment is still low, cutting rates again seems inconsistent.

That target was officially announced in 2012 but first discussed in the 1990s. Then Fed Chair Alan Greenspan wanted to keep it quiet, according to notes from a 1996 meeting:

"I will tell you that if the 2% inflation figure gets out of this room, it is going to create more problems for us than I think any of you might anticipate."

The price of oil jumped after the US announced sanctions on Russia’s biggest oil producers, as Donald Trump intensifies pressure on Vladimir Putin to end the war in Ukraine. He’s also seeking to squeeze Russia’s key crude buyers—India and China. Flows of Russian oil to major Indian refiners are expected to fall to near zero, executives said.

"The proportion of US companies beating earnings expectations this quarter is the highest in more than four year..."

The delinquency rate on subprime loans (loans to borrowers with below a 660 Vantage score) jumped to 8.3% in September. This is the highest delinquency rate in September since 2010 in the immediate wake of the Global Financial Crisis. And the direction of travel is disconcerting. It is just more evidence of how hard-pressed lower and middle-income Americans are.

Subprime loans outstanding as of this September total $2.63 trillion, equal to 15.3% of all household debt outstanding. At their peak in 2007, they totaled $3.38 trillion, equal to 28.2% of outstanding debt.

Between October 2025 and December 2028, loans on roughly 1,900 hotels with 315,000 rooms will come due, with nearly $60 billion in outstanding debt. The average interest rate across these loans is 6.5%, reflecting a lower-rate origination environment that will be difficult to replicate in today’s more restrictive lending climate.

With today’s higher-rate environment and tighter lending standards, many borrowers will confront a steep repricing of capital. The challenge will be particularly acute for properties with softer cash flow recovery or those in secondary locations with limited refinancing options.

Select-service and extended-stay brands dominate the maturing pipeline, reflecting the role of CMBS as a financing channel for repeatable, standardized hotel formats, especially in suburban and roadside markets.

US housing supply growth has been in a prolonged slump, and affordability has become a growing challenge, according to Goldman Sachs Research. Rental and homeowner vacancy rates today are below those seen in the two decades preceding the 2007-09 recession and the housing market downturn that triggered it. The home price-to-income ratio, meanwhile, has surpassed the peak it reached in the 2000s housing boom, according to Goldman Sachs Research.

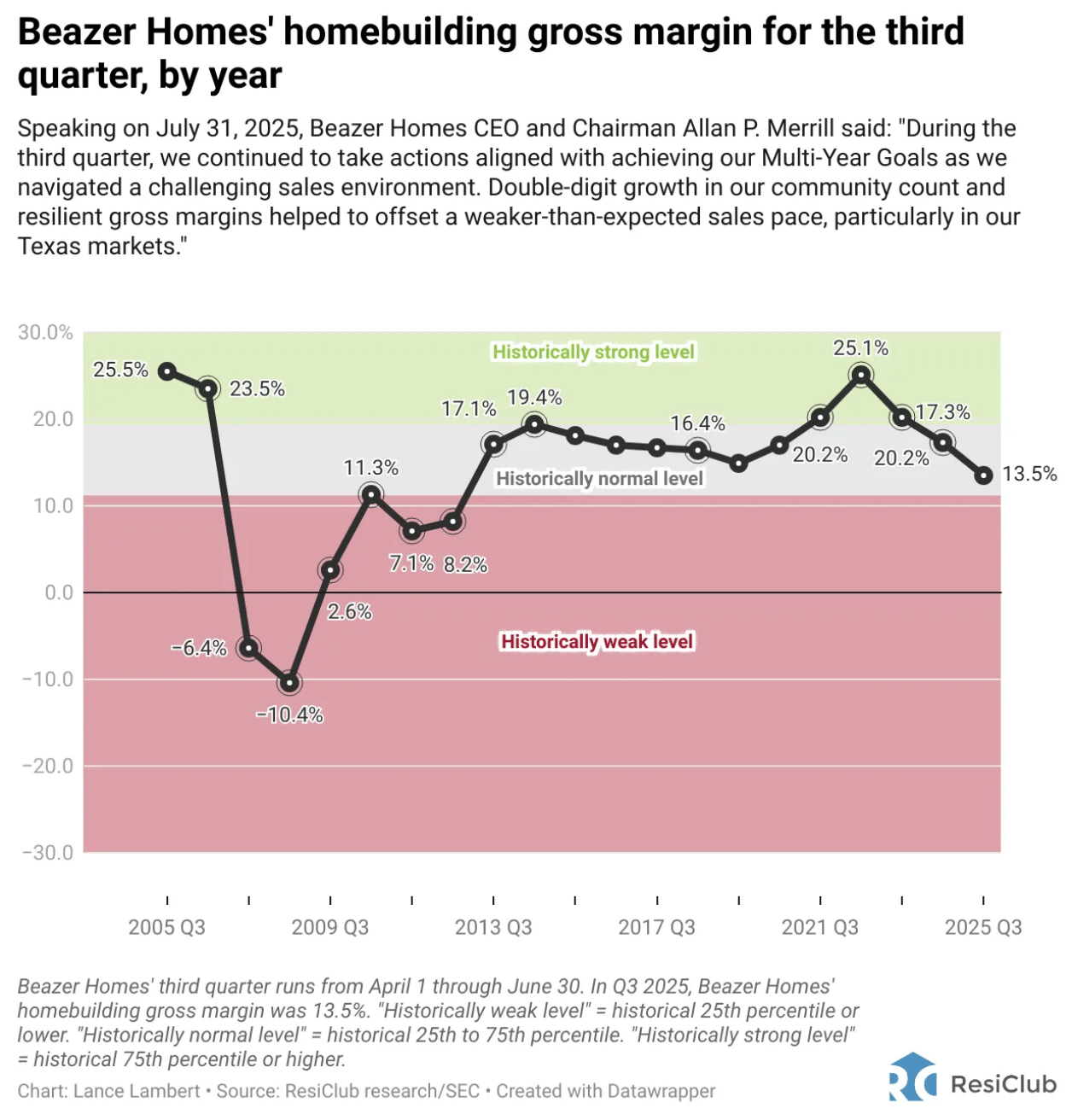

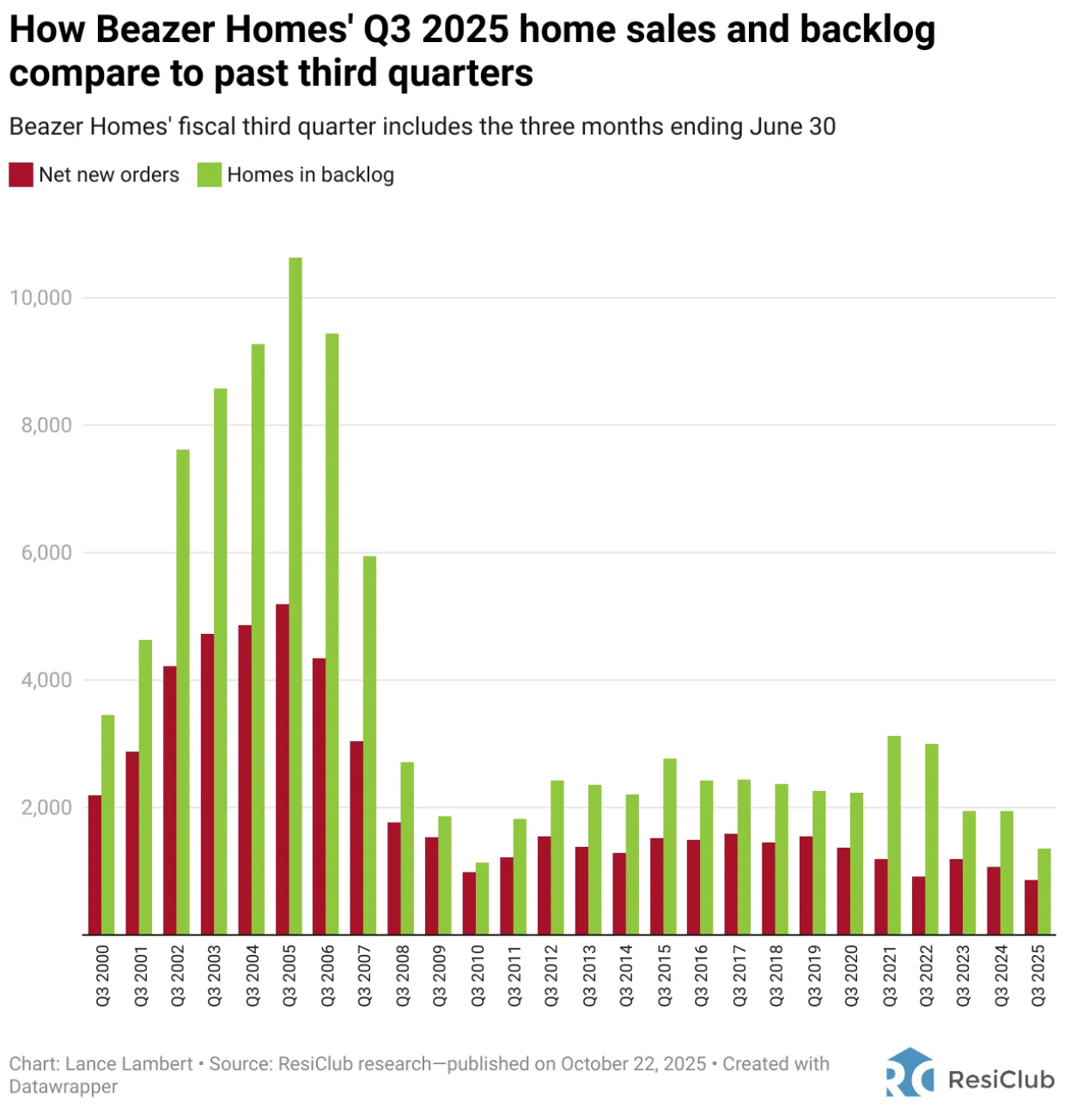

Since mortgage rates spiked in 2022, many large homebuilders have tried to make homes more affordable by shrinking them, stripping them down, or pushing buyers farther out. Allan Merrill, CEO of Atlanta-based Beazer Homes—a publicly traded builder with a $710 million market capitalization and the 23rd-largest single-family homebuilder last year—believes that’s the wrong approach.

“The way I think about it is, I don’t want to sell you a cheaper home,” Merrill told ResiClub last week. “I want to sell you a home that costs you less every month to live in—and one that will still hold its value five or ten years from now.”

Beazer’s plan focuses on three key areas: lowering the cost to power, insure, and finance a home.

The centerpiece of Beazer’s affordability push is its energy efficiency standard. Every Beazer home is built to the Energy Rated Value—a benchmark that exceeds building codes and emphasizes insulation, air filtration, and low humidity levels.

The second affordability lever comes not from the home itself, but from the insurance that protects it. Some builders outsource the closing process to third parties and collect referral fees. Beazer, by contrast, created its own insurance agency—and then decided to give away the profits.

Beazer wanted to have an agency to organize the proposals from the different firms, Merrill explains, adding: “But that entity distributes its profits to our charitable foundation—and that’s actually what we do with title insurance as well.”

The third pillar of Beazer’s affordability strategy is the company’s in-house mortgage platform, which hosts a marketplace of competing lenders. “In mortgage, there are literally no economics to us,” Merrill says. “We are not lenders, we are not brokers, we are in no way in the mortgage business. We have a platform where the banks can compete effectively, directly for the buyers.”

Unlike some other builders, Beazer doesn’t have a captive finance arm that earns interest or fees, he says. Instead, the company uses its internal system to connect buyers directly to multiple banks—and takes no profit from the transaction. That competition, Merrill says, often drives rates below what buyers would find on their own.

“Today, you’ll see permanent buydowns in the 4.99% range [in many markets], down from the low sixes,” he explains. “Every 25 basis points costs about a point—but we’re not adding a margin on top of that.” By building both the insurance and mortgage processes in-house—but running them as service models, not profit centers-Beazer is says it’s able to lower monthly payments for its homebuyers.

In September, sales in these markets were up 8.2% YoY. Last month, in August, these same markets were down 2.5% year-over-year Not Seasonally Adjusted (NSA).

Sales in all of these markets are down sharply compared to September 2019.

This graph shows existing home sales by month for 2024 and 2025, on a Seasonally Adjusted Annual Rate (SAAR) basis. Last year, the NAR reported sales in September 2024 were at 3.90 million SAAR, the low for the year.