- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 11.08.2025

Location Strategy Chartbook 11.08.2025

Real Estate Market Insights

Federal Reserve Chair Jerome Powell was more hawkish than many expected during the central bank’s press conference last week. However Goldman Sachs Research still expects the US central bank to cut rates next month, writes Chief US Economist David Mericle.

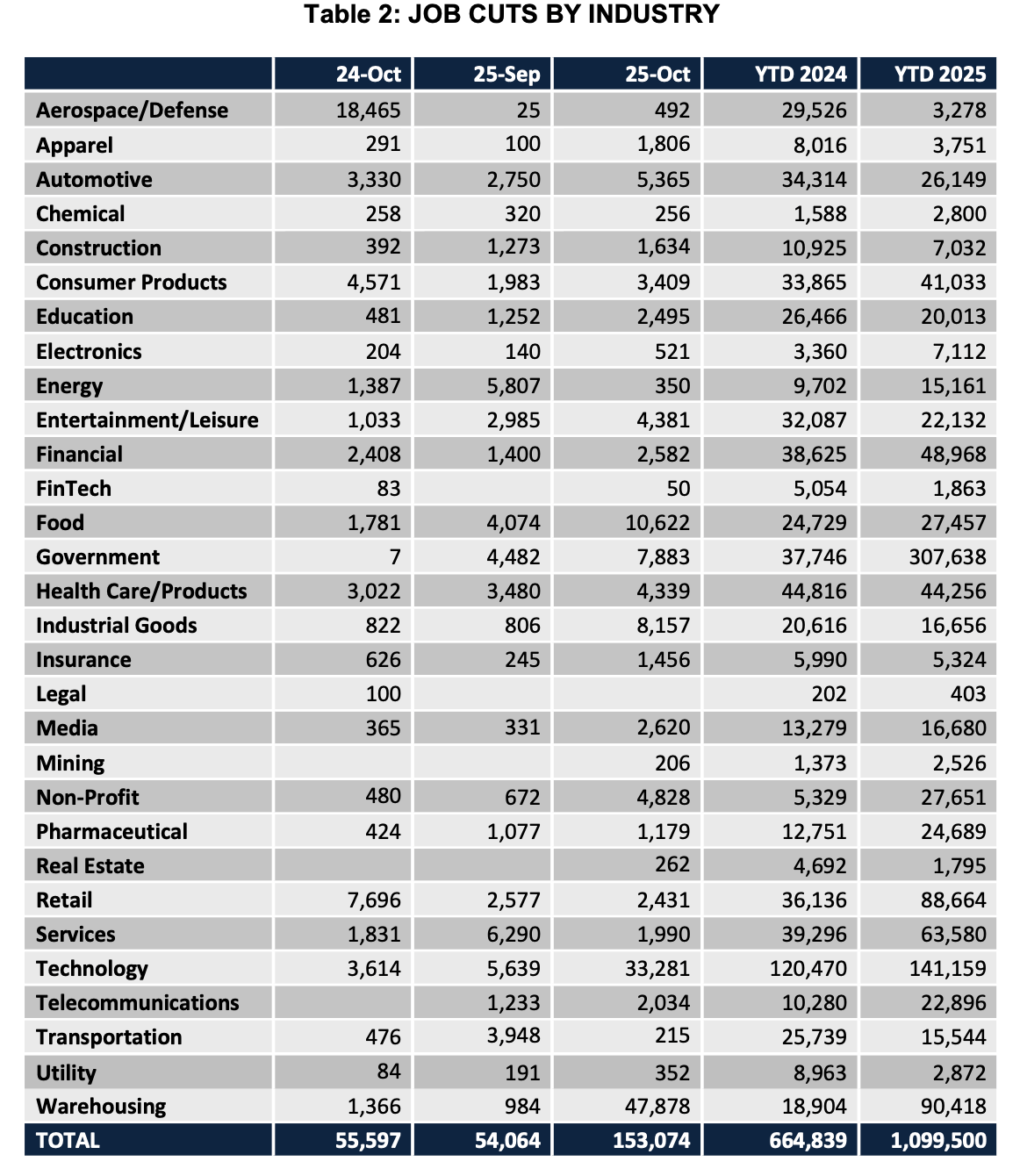

Challenger: U.S.-based employers announced 153,074 job cuts in October, up 175% from the 55,597 cuts announced in October 2024. It is up 183% from the 54,064 job cuts announced one month prior, according to a report released Thursday from global outplacement and executive coaching firm Challenger, Gray & Christmas.

“October’s pace of job cutting was much higher than average for the month. Some industries are correcting after the hiring boom of the pandemic, but this comes as AI adoption, softening consumer and corporate spending, and rising costs drive belt-tightening and hiring freezes. Those laid off now are finding it harder to quickly secure new roles, which could further loosen the labor market,” said Andy Challenger, workplace expert and chief revenue officer for Challenger, Gray & Christmas.

Through October, employers have announced 1,099,500 job cuts, an increase of 65% from the 664,839 announced in the first ten months of last year. It is up 44% from the 761,358 cuts announced in all of 2024. Year-to-date job cuts are at the highest level since 2020 when 2,304,755 cuts were announced through October.

American consumers are not happy campers. Sentiment across the country is close to the lowest it has ever been as rising inflation, rising unemployment, mass firings, a global trade war and now a record-breaking government shutdown have combined to make people less than cheery as the holidays approach.

The preliminary November sentiment index dropped 3.3 points to 50.3, just above a June 2022 reading of 50 that was the weakest in University of Michigan data back to 1978. The gauge was lower than all but one estimate in a Bloomberg survey of economists. A measure of current economic conditions slumped 6.3 points to a record low of 52.3 as anxiety mounted about the impact from the standoff in Washington.

The US economy is becoming a Jenga tower, one economist told Bloomberg, increasingly fueled by the profligate spending of the rich while a growing number of people must choose between car payments and dinner. This dichotomy isn’t new, but recent months are witnessing an even starker divide, one that some experts say makes the economy more susceptible to recession.

The data are sobering: The richest 10% of households are fueling almost half of total US spending thanks in part to the aforementioned stock market frenzy. Meanwhile, lower-income and middle class families are pulling back in the face of tight budgets, higher costs of living and a grim, rising tide of mass firings.

WSJ: This past week also should have been a decent one for bond prices amid selloffs in speculative stocks—a classic “risk-off” rally. Instead, the 10-year Treasury yield hit its highest in nearly a month Wednesday. Some think tariffs contributed to that move too, but for a completely different reason.

The probability of the administration prevailing in a Supreme Court case challenging lower-court rulings that Trump’s tariffs are illegal was as high as 43% last Thursday, according to betting site Polymarket. The odds began to wobble as this Wednesday’s hearing drew nearer and sank as low as 25% that afternoon.

More than $100 billion will have been collected from the specific tariffs being debated by the time a decision is reached. The prospect of at least some being refunded is enough to affect federal borrowing needs. Even without rebates, collections could drop sharply while the White House finds legal workarounds to impose new levies.

It’s ironic: Tariffs initially spooked the bond market. Now that they’re helping to plug revenue lost to tax cuts, their potential absence worries investors.

Tariffs are only the trigger, though. What’s really changed is that budget deficits are unsustainably high and foreigners’ willingness to hold dollar assets no longer seems unlimited.

Bond investors need a new instruction manual.

A succession of high-profile defaults connected to bankruptcies and fraud allegations have raised questions about the health of credit markets. Concerns are centered around the rapid growth of the $1.1 trillion private credit market. In particular, direct lending to small- and medium-sized businesses has grown significantly in the last decade.

The defaults of car parts manufacturer First Brands and auto loans company Tricolor, and concerns linked to commercial real estate firm Cantor Group, have prompted investors to take a closer look at the vulnerabilities of credit markets. Nonetheless, “at this stage, we would still very much come down on the side of these being idiosyncratic events and not credit-type events,” says Spencer Rogers, a credit strategist at Goldman Sachs Research.

In the Seattle metropolitan area, employment fell by 15,000 jobs between August 2024 and August 2025. That amounts to a 0.7% decline over the year. This employment downturn could signal a shift in a region that was starting to see signs of recovery.

Some subsectors have experienced substantial losses. Warehousing employment dropped by 23.5%, or 11,900 jobs, reflecting a sharp pullback in logistics activity. As tech company layoffs have continued throughout 2025, software publishing firms trimmed their workforce by 12%, or 8,200 jobs.

Employment services declined by 11.5%, a loss of 2,800 jobs. Recruiters and contingent workers are often among the first let go when companies tighten their budgets, making this sector a leading indicator of economic stress.

Not all sectors saw declines, though. Healthcare saw the largest numerical gain among subsectors, with 5,200 new jobs, a 3.1% increase. Accommodation and food services grew by 2,800 jobs, representing a 2.4% increase in employment. Private education services gained 2,300 jobs, representing a 7.4% increase in employment. Arts, entertainment and recreation also posted a gain of 2,300 jobs, a 6.6% increase for that subsector.

These shifts carry implications for commercial real estate. Job losses in sectors that heavily rely on offices could weigh on office demand, even as companies implement strong return-to-office mandates. Meanwhile, the steep decline in warehousing employment suggests a slowdown in logistics activity, which could temper absorption in industrial properties.

Cold storage space remains in high demand nationwide, but steep costs and complex development requirements have slowed new projects in most markets. Dallas-Fort Worth has been an exception, thanks to steady population growth and rising consumer demand for food and perishables.

Over the past decade, North Texas added about 6.6 million square feet of cold storage space. For perspective, the entire United States added 49.8 million square feet during that time, making the region responsible for nearly 13% of national growth.

Despite this surge, the region’s share of the overall cold storage market remains modest. With 19.1 million square feet of total space, Dallas-Fort Worth accounts for just 5.9% of the U.S. market, roughly in line with its share of the broader industrial sector.

New projects are clustering along major trade routes, typically just outside the urban core where land is more affordable yet still close to population centers. Most construction has concentrated in Dallas and Fort Worth proper, with additional activity in Denton and other outlying areas. One key hotspot is the point where Interstate 35 splits into its eastern and western sections before reconnecting farther south in Hillsboro.

Among the notable developments is Chill Development DFW, a 302,000-square-foot facility designed for freezer capability featuring 50-foot clear heights and convenient highway access. Walmart has also made a significant investment with its 735,000-square-foot distribution center for perishables in Lancaster, part of the retailer’s broader effort to expand and streamline its frozen goods supply chain. Another major project, Cold Summit Dallas II, brought 365,000 square feet of cold storage space to the region and stands as one of the last large-scale industrial construction projects in Southeast Dallas in 2025. Rounding out recent activity is Performance Food Group’s 343,000-square-foot building at GSW Logistics Crossing, which wrapped up construction in May.

WSJ: America’s biggest builders are struggling to sell homes even when they offer buyers a 4% mortgage. Their experience suggests rate cuts alone won’t be enough to boost weak sales in the wider housing market.

The number of completed but unsold new homes has reached levels last seen in the summer of 2009, data from the Federal Reserve Bank of St. Louis shows. At the end of last year, builders were confident that sales would recover in 2025 and built tens of thousands of units to have enough supply for the spring-buying season. But demand didn’t pick up, and more homes sat unsold. They have tried to use sweeteners to shift inventory.

D.R. Horton, which builds roughly one in every seven new homes in the U.S. and has its own financing arm, is offering 3.99% mortgages to buyers. The company has also knocked 3% off its average selling price over the past 12 months and expects to cut prices further in its 2026 fiscal year, which runs through September. America’s second-largest builder, Lennar, said it offered buyers incentives worth $64,000 on its average home sale last quarter to meet its sales target. A combination of subsidized mortgages and price cuts on offer from Lennar was equivalent to a 14.3% price reduction. The last time it had to offer home buyers such a deep discount was during the global financial crisis.

Profit margins have taken a hit from the rising cost of these incentives, so builders have decided to slow construction and wait for demand to recover. D.R. Horton only started building 14,600 homes over the three months through September, down 21% from its pace a year ago. Sales of new homes are roughly a fifth of all U.S. housing transactions, so they aren’t the full picture. But they can give a more revealing read of underlying demand than the resale market in parts of the country. Builders have to price homes in line with demand if they want to sell finished inventory.