- Location Strategy Chartbook

- Posts

- Location Strategy Chartbook 11.15.2025

Location Strategy Chartbook 11.15.2025

Real Estate Market Insights

Inflation has been rising, sitting now at 3%, and Fed policymakers are stepping up warnings that another cut in December could be a damaging move. Officials broadly agree the labor market has cooled, but are split over whether the slowdown will intensify. And while one group is sanguine about price pressures, others are warning further cuts put years of progress on inflation at risk.

“I do not think further cuts in interest rates will do much to patch over any cracks in the labor market—stresses that more likely than not arise from structural changes in technology and immigration policy,” said Jeffrey Schmid, president and chief executive of the Federal Reserve Bank of Kansas City. “However, cuts could have longer-lasting effects on inflation as our commitment to our 2% objective increasingly comes into question.”

Cass Freight Index slid 2% in October, a sign of an ongoing freight recession. This index includes all domestic freight modes and is derived from $25 billion in freight transactions processed by Cass annually on behalf of its client base of hundreds of large shippers.

Older generations - Baby Boomers and Traditionalists - have shown faster credit and debit card spending growth per household than overall households since 2022, according to Bank of America aggregated card data.

In 2023, the cost-of-living adjustment (COLA) to Social Security retirement benefit incomes was large compared to wage growth, likely helping boost retirees' spending relative to other cohorts.

But COLA increases have been smaller since then and the 2026 COLA announced adjustment of 2.8% is also relatively close to current wage growth. Positive wealth effects from rising equity markets may also be boosting older generations' spending currently. •

Strong growth in older generations' spending is "good news" as they are becoming an ever-larger proportion of the US population. And 2026 is likely to see a wave of retirees as Baby Boomers reach "Peak 65."

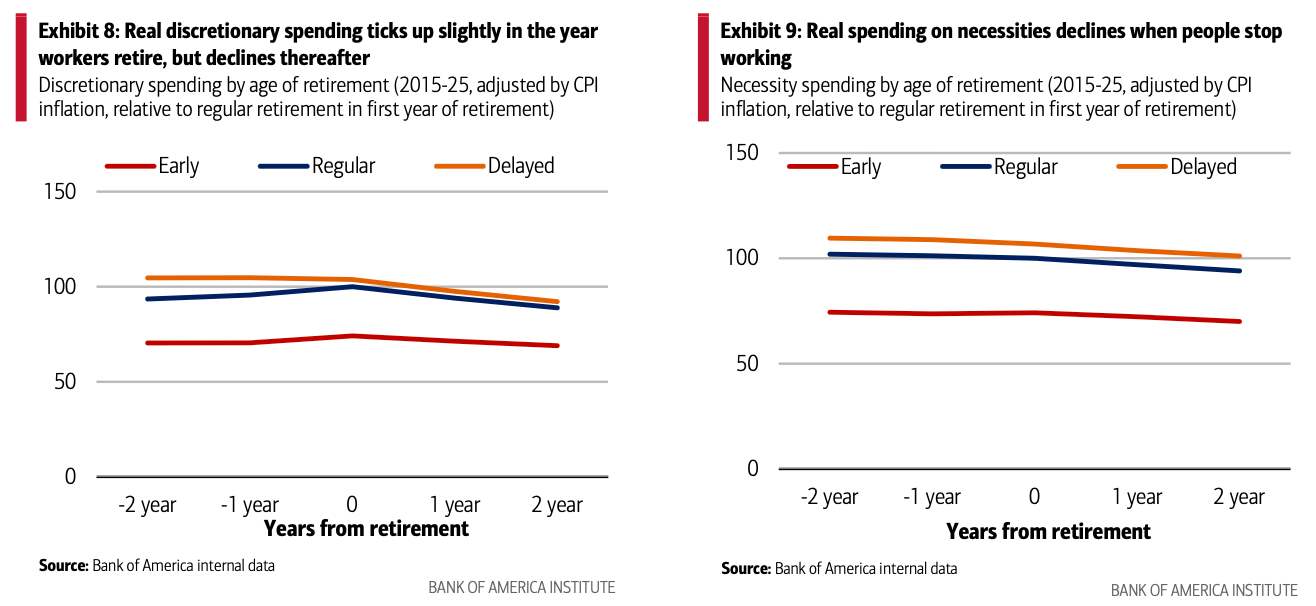

Looking at households before and after retirement, we find that "early retirees" have significantly lower deposits and spending than those who retire later. So while we expect that booming equity markets may help provide support to older generations' spending for some time yet, it appears people are increasingly expecting to need to retire later.

As we have noted in the past, older generation spending growth (defined here as Baby Boomers and Traditionalists) per household has been stronger than the overall pace across all generations since 2022, according to Bank of America aggregated credit and debit card data

The divergent spending trends across generations are especially important because the US is experiencing a big demographic shift, as a wave of retirees reshapes the economic landscape. According to Census Bureau population projections, the number of resident Americans (those living, both civilian and Armed Forces, in the United States) turning 65 will peak in 2026, a phenomenon sometimes referred to as “Peak 65”. Between 2025 and 2027, over 4.1 million residents per year are expected to reach this milestone. Moreover, the proportion of US residents aged 65 and older is expected to rise from 17.3% in 2022 to 20.6% by 2030, according to data from the Census Bureau

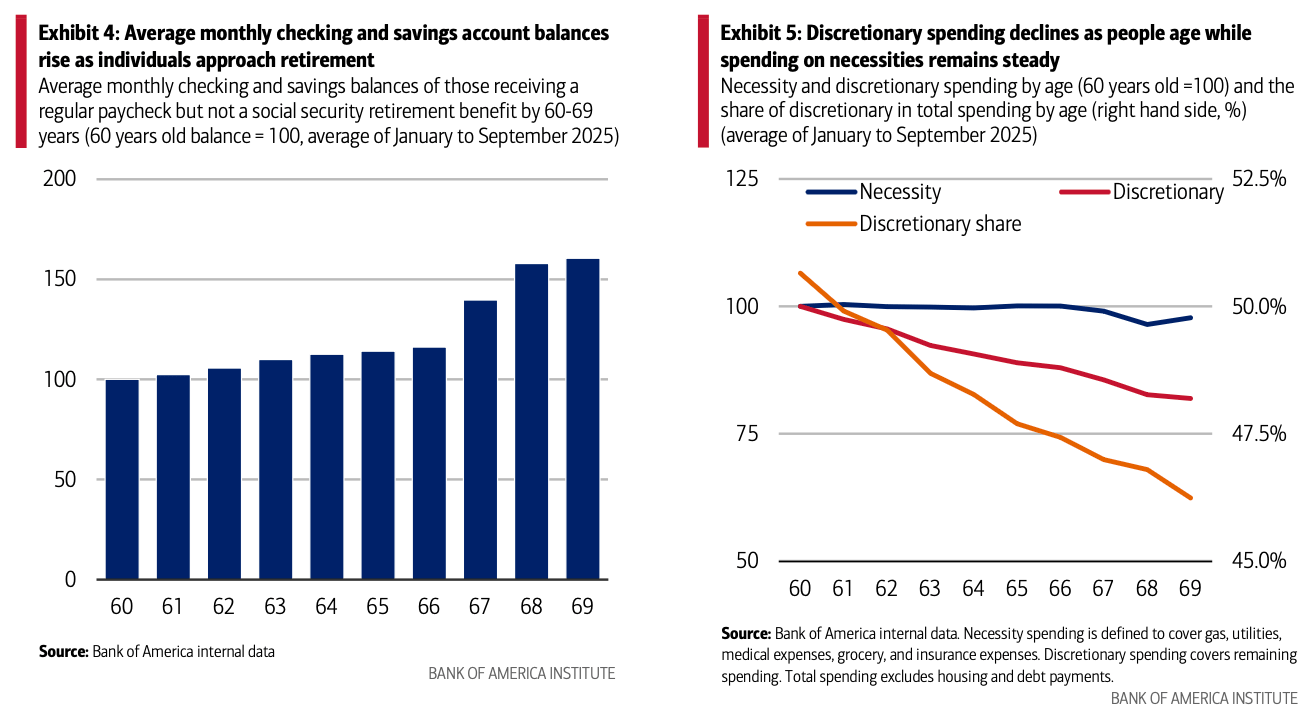

As this large share of the population transitions from earning income to relying on retirement savings and benefits, how will its spending evolve? This question is increasingly important for both policymakers and businesses adapting their strategies to an aging population. To understand how spending evolves with age, we first analyze the saving and spending patterns of Bank of America households aged 60 to 69 years who receive a regular paycheck deposit into their account but are not yet receiving Social Security retirement benefits. This helps to give us a baseline for how spending changes with age before retirement. Our data reveals a clear trend: as 60+ workers age, their average monthly checking and savings account balances typically rise steadily, while their spending declines. Notably, there is a marked step-up in deposit balances at age 67. In our view, this probably reflects a shift towards more liquid cash savings in anticipation of reduced earnings in retirement as well as lower spending

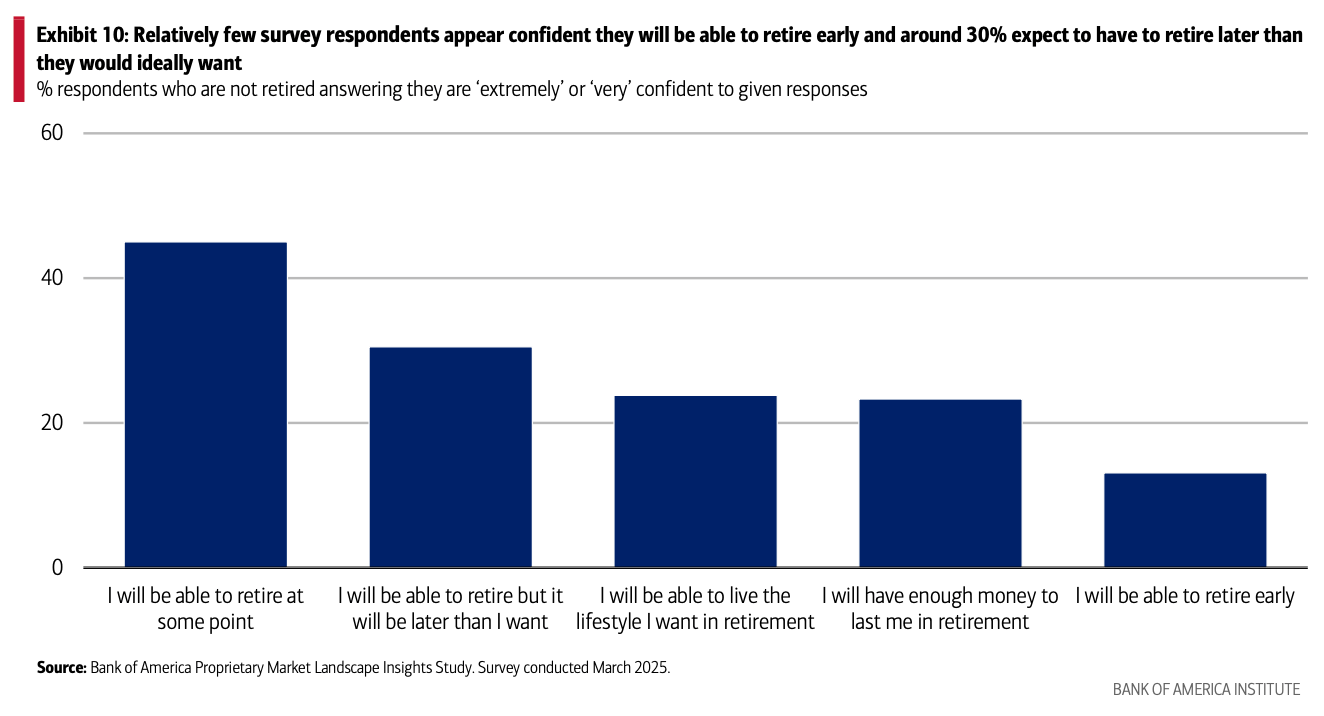

These findings suggest that as Baby Boomer and Traditionalists age, their spending will tend to decline. This implies that their strong Bank of America card spending relative to other cohorts may gradually slow, unless broader “macro factors, ” such as wealth effects can offset the trend. In our view, the possibility of lower total and discretionary spending and reduced savings in retirement is becoming a key reason why those of retirement age may keep working. According to a Bank of America Proprietary Market Landscape Insights Study, only around 10% of pre-retirement respondents felt confident they would be able to retire early. And around 30% thought they would need to retire later than they would like

The Chicago Fed estimates the unemployment rate increased to 4.36% in October, the highest since October 2021.

The increase reflects slower hiring as well as a higher rate of layoffs, quits, and retirements.

It was also influenced by the government shutdown.

As a result, the unemployment rate has now risen by a full percentage point since May

Americans have started to increasingly worry about their jobs, with some 55% of employed Americans saying they’re concerned. This follows a drumbeat of recent layoffs at big names like Amazon, Target, and Starbucks and the most layoff announcements for any October in more than two decades.

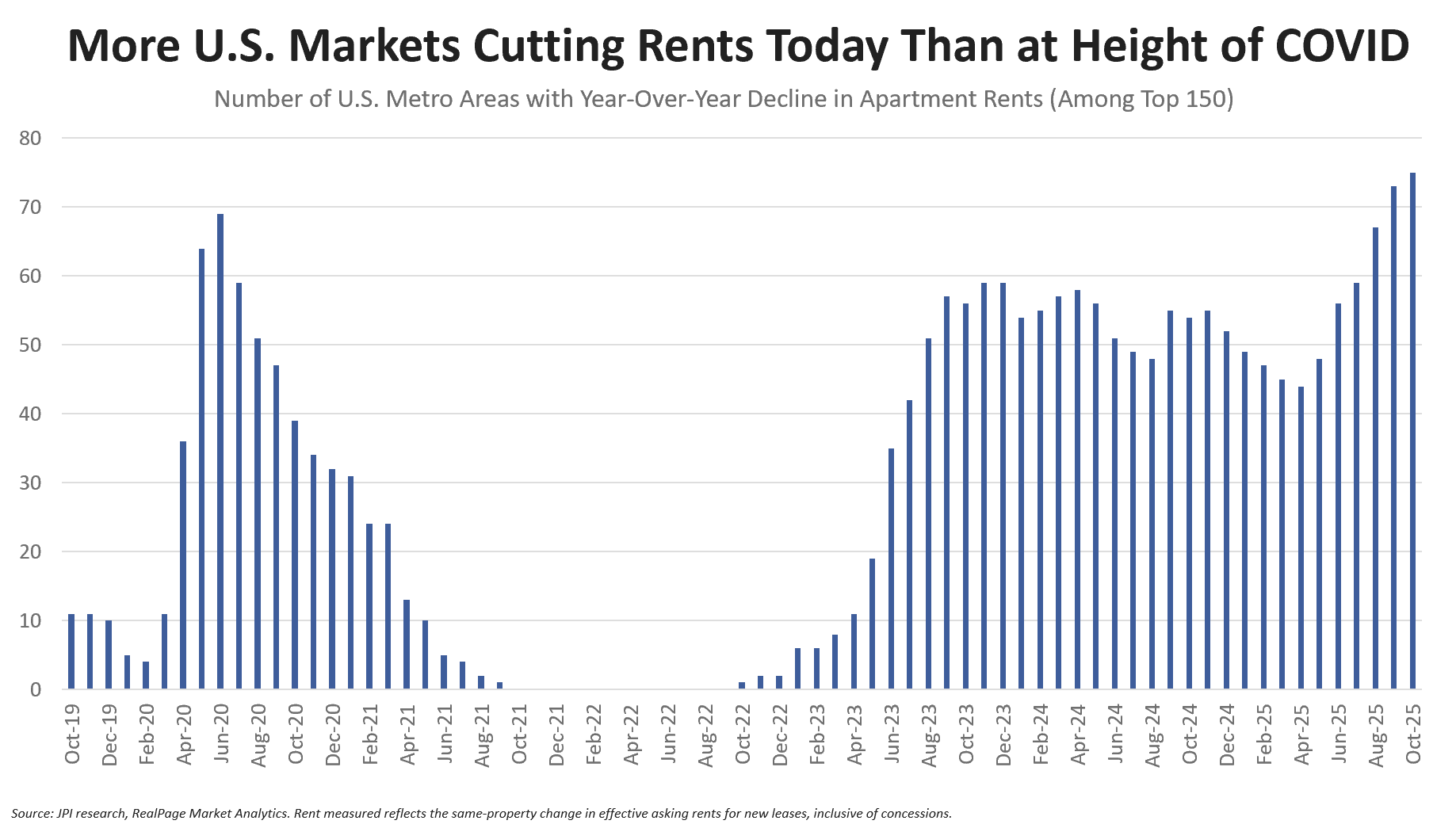

Jay Parsons: Half of the nation's 150 largest metro areas cut rents year-over-year through October.

Most of those are high-supplied markets dealing with the biggest supply wave in a half-century (led by Denver, Austin, Phoenix), but that's not the only factor. We're also seeing rents fall in lower-supplied markets like Washington DC, Los Angeles, Las Vegas and Sacramento, among others.

In those markets, a soft job market and weak consumer confidence are likely culprits. Apartment execs are saying that CURRENT renters are still in good shape (paying rent, renewing leases, maintaining low rent-to-income ratios, etc.) but PROSPECTIVE renters seem to be frozen, in wait-and-see mode.

Worth noting: The slowdown is not universal.

Rents are still rising in half the country, led by low-supply markets like San Francisco (+7.4%), San Jose, New York and Chicago.

And rent momentum did accelerate in a number of MSAs between September and October -- including high-supplied markets like Atlanta, Orlando, San Antonio, Austin and Denver ... where rents are still falling, but to a lesser degree than previously.

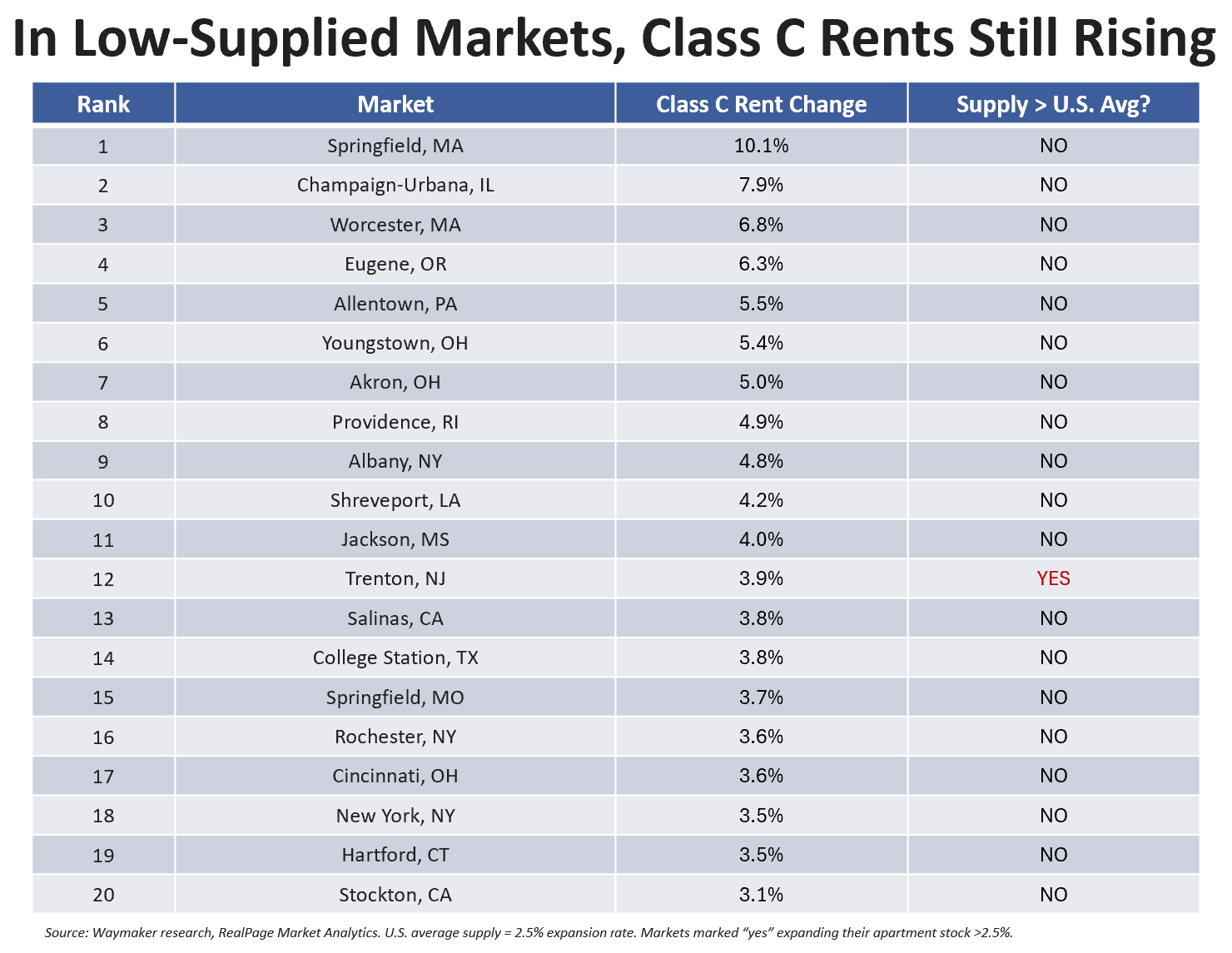

In 19 of the 20 MSAs where Class C rents growing >3%, new apartment supply TRAILS the U.S. average.

In 16 of the 17 MSAs where Class C rents FALLING >6%, new apartment SUPPLY exceeds the U.S. average.

Vacancy rates have climbed to 20-year highs in Houston

Luxury properties lead absorption

Rebound in three-star properties & developers scaled back on upscale amenities to improve affordability.

Since 2023, more than 61,000 units have come online

Aggressive concessions to fill units

Rent growth turned negative in the second quarter of 2025 for the first time in 15 years and remains in decline

Asking rents have dropped in high-growth submarkets north and west of Houston, including Bear Creek-Copperfield and Cinco Ranch. Extended the tour-to-lease timeline, with four to six weeks of free rent now common in newly completed complexes.

Affordable submarkets with limited new supply — such as Alief and Baytown — have emerged as top performers over the past year.

For the first time in modern housing market history, U.S. single-family new construction, in aggregate, is no longer selling at a premium to existing homes. The median sales price of new single-family homes in August 2025 was -0.2% lower than the median sales price of existing single-family homes—an all-time low. That’s a dramatic shift from January 2013, when the typical new home sold for +38.4% more than a comparable existing home, marking the highest premium ever recorded.

This reversal underscores how the post-pandemic housing cycle has reshaped market dynamics. While home prices have experienced some downward pressure—particularly in pandemic-era boomtowns—since mortgage rates peaked in 2022, existing homeowners have largely resisted those declines. That coupled with lock-in has seen existing home turnover fall to multidecade lows. Meanwhile, new-home prices have adjusted more meaningfully from the 2022 peak, aided in part by builder incentives and the construction of smaller, more affordable homes.

Percent of household mortgages 30+ days delinquent